Stale inventory has a monthly price tag most brands never calculate.

3PL storage fees. Capital that can't move. SKUs that lose relevance every week they sit.

Cashmas in July turns that dead weight into cash before Q4 starts. 30 days. Private. Handled.

https://t.co/V8rI2CA5lg

91% of brands that ran a Q3 cash event held or grew their Q4 margin, with revenue up 48%.

Cashmas in July does it in 30 days, using only your list and paid audience, without touching your public site.

See how it works: https://t.co/WxXT7gaiY4

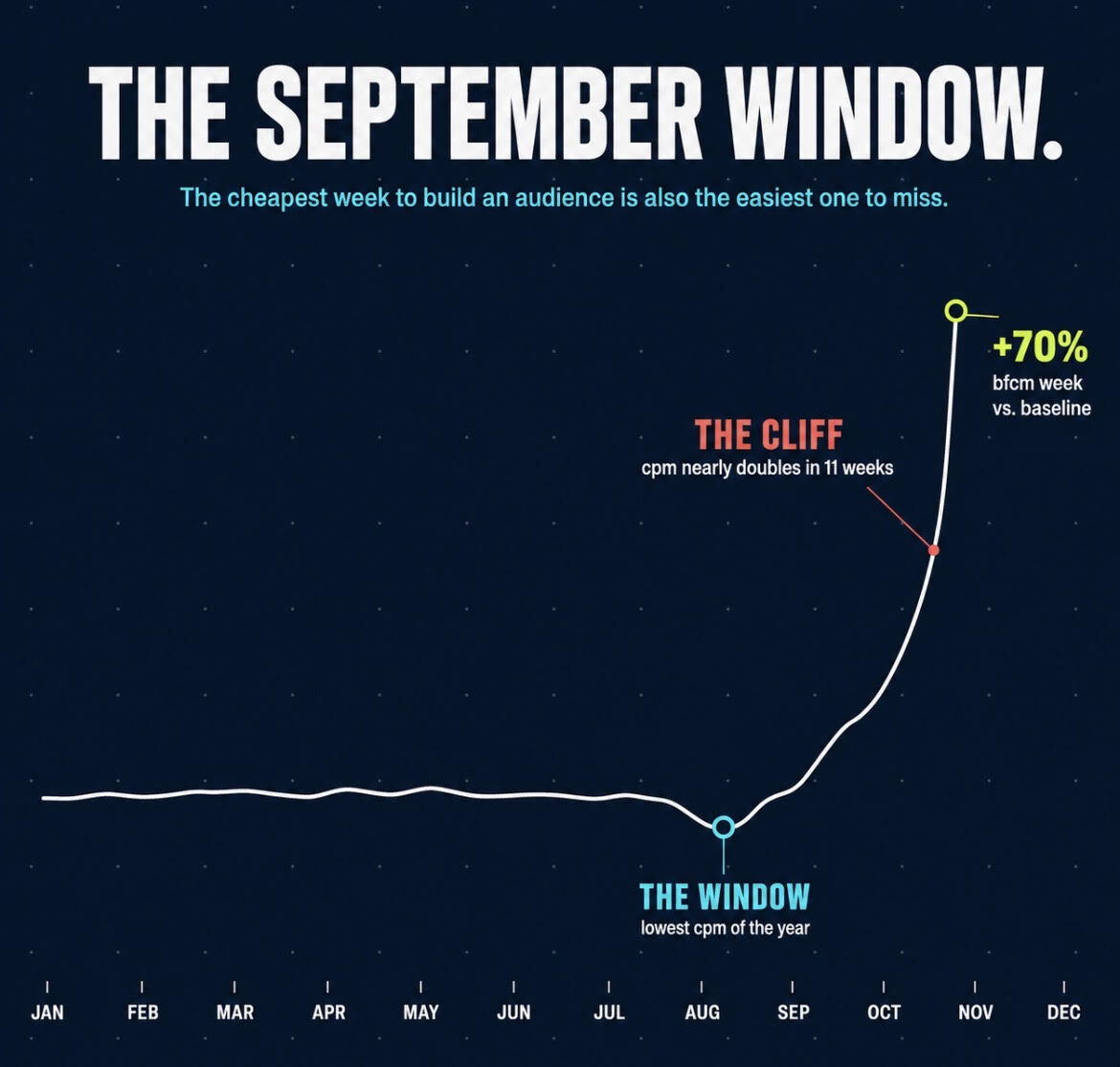

Pulled from our MCP this morning. Data from 170+ brands over the past 2 years:

Q4 CPM vs. Jan–Sep baseline: +27.7% (2024), +17.0% (2025)

BFCM week CPM vs. baseline: +70.7% (2024), +52.1% (2025)

The annual low consistently lands in the second week of September, both years.

What does this mean for your Q4 stategy?

If you're a 7-figure brand stuck at a growth plateau, we can tell you what's wrong without looking at your ad account.

The answer is almost never creative. Almost never ad structure. Almost never a new platform.

It's offer-market fit. And Q3 is the window to fix it before Q4 spend ramps.

@JoySharma_11 breaks down the full framework. →

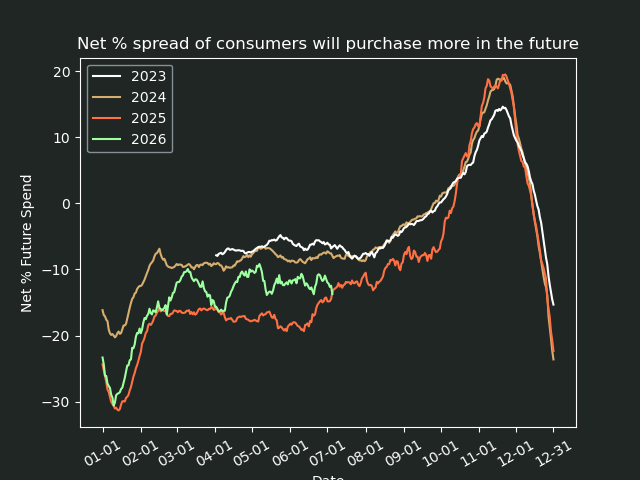

For the first time this year, Future Purchase Sentiment in our DTCCI data dropped below last year by more than 0.1% in the 28-day rolling average. Without Prime Day in July, I expect a pullback from consumers. I will calculate our DTCCI for July in the next couple of days.

Thanks to @TaylorHoliday@KnoCommerce@CommnThreadCo@JeremiahPrummer

More in the @dtcindex

As of July 1, Meta is charging location fees on European ad delivery. UK: 2%. France, Italy, Spain: 3%.

They show up as a separate line item on your invoice. On top of your campaign budget.

If your campaigns touch Europe at all, your effective CPA just changed.

Full breakdown: https://t.co/6RybmprtdH

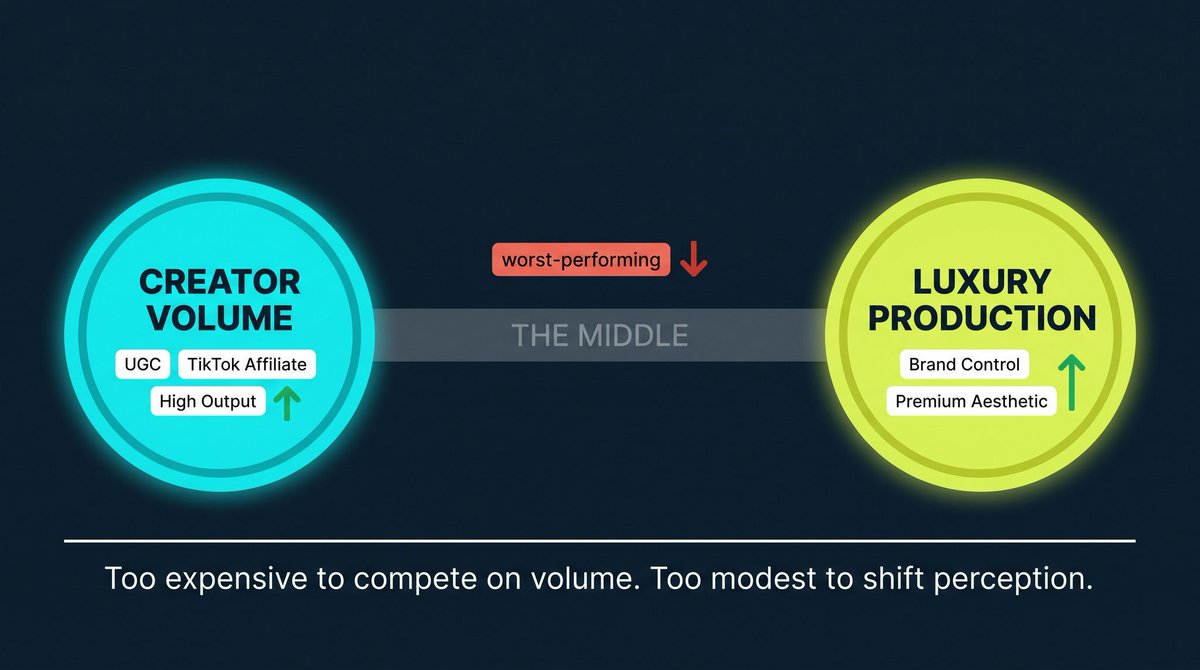

A founder came to a Q&A recently with a real problem: they had invested $40,000 in a video production and their phone-filmed UGC was converting at two to three times the rate.

What they were experiencing is what we see across the portfolio. The creative barbell.

On one end: full creator outsourcing. High volume, TikTok affiliate, UGC. Brand identity is whatever the creator makes it. On the other: luxury brands with deep production competency, where every touchpoint reinforces a premium perception built over years of sustained investment.

The middle is the worst-performing place to be.

The production cost is too high to compete on volume. Too modest to actually shift brand perception. A $40,000 production does neither.

Real luxury brand awareness requires millions in sustained marketing effort. For a 7-figure DTC brand, unaided brand awareness is vanishingly small. Most of the people who could buy from you have never heard of you, which means your brand identity is far more malleable than it feels from the inside.

The brands that accept this while they still have runway will build a profitable creative engine and use those margins to invest in the brand they want to become. The ones protecting an aesthetic their customers haven't been convinced of yet will spend their runway on production with no one to receive it.

If in 18 months you want to be more precise about creative quality, you'll have room to make that shift. But you have to build the acquisition engine first.

Three measurement truths that don't care about your opinion:

1. Media efficacy changes constantly. Any system that treats it as fixed is wrong.

2. You are always building an approximation. There is no perfect measurement. Only less wrong measurement.

3. Progressive truth is the goal. Every test reduces the error rate. Truth accumulates over time.

Full framework: → https://t.co/VObDY7omJq

"Organic" and "direct" aren't channels.

They're where your attribution model stopped looking.

One brand celebrated a spike in direct traffic for 4 days. We traced it to a creator post with no UTM.

Paid traffic with the receipt lost.

Every customer has a reason they're there. Find it.

Brands come to us convinced they've hit Meta saturation.

We look at the creative portfolio and find: one angle, one visual style, one creator, for 6 weeks straight.

The algorithm didn't run out of audience. It ran out of inputs.

The answer isn't new platforms. It's new angles.

From DTCCI data, Present Sentiment is up above the last 3 years at this time but Future Sentiment is closing in on the low of last year.

This may point to a challenging July after this holiday weekend.

Thanks @JeremiahPrummer@KnoCommerce@TaylorHoliday@CommnThreadCo

Every morning, three questions:

What is the data showing us vs. expectation?

So what does that mean for the monthly target?

Now what action do we take today?

3% forecast accuracy across $3B in GMV doesn't happen at end of month. It happens every morning.

→ https://t.co/XZHwZmfxjU

We run our forecasts on 4 proprietary models wired together.

They produce a daily P&L with 3% accuracy across $3B+ in GMV.

Here's how they connect:

→ Spending Power Model forecasts new customer revenue from any spend level

→ Retention Model builds returning revenue cohort by cohort

→ Event Effect Model distributes daily precision without breaking monthly targets

→ Creative Demand Model ensures the ad account has fuel to execute

Each output feeds the next. That's why the forecast actually works.

Most brands test new paid channels in the wrong order. Build creative, launch, hope it works.

The variable that actually matters is whether your customer lives on that platform. Get that right first and the creative follows.

We broke down how to do it: https://t.co/hK4nQA6bV5