So, wen 🍌 ?

1) After the labour market weakens and the FED is forced to cut, and then eventually stops cutting.

Or

2) If everything holds steady and we start seeing ISM PMIs ticking up.

So keep an eye on jobs data and those PMIs, then you have a banana 🐵

Food for thought.

Trump, Hormuz and the End of the Free Ride

For half a century, Western strategists have known that the Strait of Hormuz is the acute point where energy, sea power and political will intersect. That knowledge is not in dispute. What is new in this war with Iran is that the United States, under Donald Trump, has chosen not to rush to “solve” the problem. In Hegelian terms, he is refusing an easy synthesis in order to force the underlying contradiction to the surface.

The old thesis was simple: the US guarantees open sea lanes in the Gulf, and everyone else structures their economies and politics around that free insurance. Europe and the UK embraced ambitious green policies, ran down hard‑power capabilities and lectured Washington on multilateral virtue, secure in the assumption that American carriers would always appear off Hormuz. The political class behaved as if the American security guarantee were a law of nature, not a contingent choice. Their conduct today is closer to Chamberlain than Churchill: temporising, issuing statements, hoping the storm will pass without a fundamental reordering of their responsibilities.

Trump’s antithesis is to withhold the automatic guarantee at the moment of maximum stress. Militarily, the US can break Iran’s residual ability to contest the Strait; that is not the binding constraint. The point is to delay that act. By allowing a closure or semi‑closure to bite, Trump ensures that the immediate pain is concentrated in exactly the jurisdictions that have most conspicuously free‑ridden on US power: the EU and the UK. Their industries, consumers and energy‑transition assumptions are exposed.

In that context, his reported blunt message to European and British leaders, you need the oil out of the Strait more than we do; why don’t you go and take it? Is not a throwaway line. It is the verbalisation of the antithesis. It openly reverses the traditional presumption that America will carry the burden while its allies emote from the sidelines.

In this dialectic, the prize is not simply the reopening of a chokepoint. The prize is a reordered system in which the United States effectively arbitrages and controls the global flow of oil. A world in which US‑aligned production in the Americas plus a discretionary capability to secure,or not secure, Hormuz places Washington at the centre of the hydrocarbon chessboard. For that strategic end, a rapid restoration of the old status quo would be counterproductive.

A quick, surgical “fix” of Hormuz would short‑circuit the dialectic. If Trump rapidly crushed Iran’s remaining coastal capabilities, swept the mines and escorted tankers back through the Strait, Europe and the UK would heave a sigh of relief and return to business as usual: underfunded militaries, maximalist green posturing and performative disdain for US power, all underwritten by that same power. The contradiction between their dependence and their posture would remain latent.

By declining to supply the synthesis on demand, and by explicitly telling London and Brussels to “go and take it” themselves, Trump forces a reckoning. European and British leaders must confront the fact that their energy systems, their industrial bases and their geopolitical sermons all rest on an American hard‑power foundation they neither finance nor politically respect. The longer the contradiction is allowed to unfold, the stronger the eventual synthesis can be: a new order in which access to secure flows, Hormuz, Venezuela and beyond, is explicitly conditional on real contributions, not assumed as a right.

In that sense, the delay in “taking” the Strait, and the challenge issued to US allies to do it themselves, is not indecision. It is the negative moment Hegel insisted was necessary for history to move. Only by withholding the old guarantee, and by saying so out loud to those who depended on it, can Trump hope to end the free ride.

I guess Israel made him say this back then too, right? 🙈

If anyone thinks Bibi made Trump go to war, that person clearly doesn’t know very much about Trump.

But watch what he says in this old interview.

I had dinner once with a top physicist and a top computer scientist and asked what they thought the probability was that we were in a simulation.

They answered simultaneously at 0% and 100% respectively. It was like a double-slit experiment, but with humans.

🚨🇮🇱 NEW:

Elbit Systems is developing an airborne portable laser system for fighter jets and helicopters to enhance Israeli air superiority.

The system uses directed energy to intercept UAV swarms and missiles above cloud cover, minimizing weather impact while integrating into Israel’s multi-layered defense network.

It offers rapid deployment, precision targeting with minimal collateral damage, and potential future offensive capabilities—marking a major shift in countering complex threats.

Stay connected, follow @MOSSADil.

The Israeli Air Force bombed a meeting of Iran’s Assembly of Experts while they were voting to choose the new Supreme Leader.

All 88 members have reportedly been ELIMINATED.

How did Israel have all that intelligence?

The regime's former president Ahmadinejad: “Iran's Secret Service had established a unit to target Mossad agents within Iran. However, the head of this unit turned out to be a Mossad operative himself, along with 20 other agents.” 🤣

Chances on Polymarket’s betting market that Ayatollah Ali Khamenei will be out as Supreme Leader of Iran by January 31 have skyrocketed in the last 24 hours, as anti-government protests across the country have exploded, with chances currently sitting at 20% and rising.

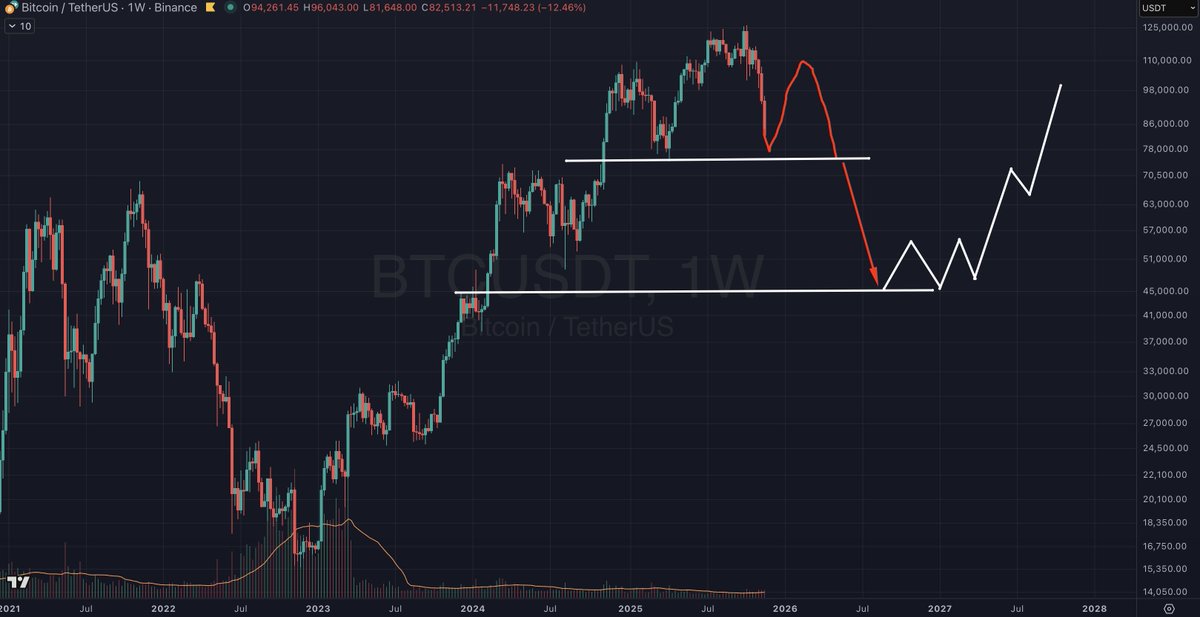

This is one of the most important things you need to understand about this cycle.

Everyone is looking for clues in the wrong place.

You cannot just look at Bitcoin pice action and make an overall decision about the cycle.

There are far greater foundational moves at play that dictate what happens.

And one of the clearest ones is the way the $RUT is currently moving.

The $RUT is the index for small cap stocks. Just like how we have OTHERS for alts.

And the $RUT is a key risk on metric as this index really only moves in the most risk on positions in the market as it is the highest risk stock index.

At this moment right now, it is nowhere near a cycle ending position... it is quite literally on the edge of breaking into price discovery.

And we can see where Bitcoin was the last time this was about to happen with the $RUT.

Then take a look at where $RUT was when Bitcoin was in the position everyone thinks we are in now.

In 2022, $RUT was starting its break down after large moves to the upside and distribution. And so was Bitcoin.

Now, it is only just starting its breakout phase.

And as hard as that is for many to believe, so is Bitcoin.

The most confusing thing for everyone this cycle is that Bitcoin has been moving higher not because of liquidity, but because of adoption.

This is why there have been no true sustained moves and no real price discovery. And also why alts have not been able to hold any kind of run either. There has not been the liquidity for it.

But everyone is making out these moves so far as the cycle completing, when the actual business/liquidity cycle is only just getting underway...

Which is why $RUT is about to breakout.

$RUT has followed an almost exact pattern from its previous run up to breaking out between 2020 - 2021.

It is not a coincidence that this is happening as we enter easier liquidity conditions.

And Bitcoin is not all of a sudden going to enter a bear market just because it has dipped.

You have to understand what is happening within the bigger picture here, and not just focus on the Bitcoin chart.

Bitcoin, alts, small cap stocks and anything else that is high on the risk curve only ever truly have their parabolic runs when the liquidity conditions enable them.

And as we can see with $RUT, they are starting to be enabled.

So, wen 🍌 ?

1) After the labour market weakens and the FED is forced to cut, and then eventually stops cutting.

Or

2) If everything holds steady and we start seeing ISM PMIs ticking up.

So keep an eye on jobs data and those PMIs, then you have a banana 🐵

Secondly, historically, risk assets suffer during rate cuts. Why? Because cutting rates means the economy is in trouble and needs support. Since markets forward-price lower earnings etc, we go down... Only when cuts STOP and the FED deems enough support has been given, then up.