The "Network Effect" is one of the most powerful forces in #Crypto, explaining exponential growth. Simply put: the more users or participants a network has, the more valuable it becomes for every user. We witnessed this phenomenon propel $BNB to prominence, and now, $CHEX is primed to ride this wave within the exploding Real World Asset (RWA) tokenization sector. Understanding this is key to spotting the generational wealth opportunity in $CHEX, that @krakenfx is bringing to the masses.

Source: https://t.co/FoS1wZjm8z

Delighted to announce that $CHEX will be listing on @krakenfx! The @ChintaiNexus network token has been added to the roadmap today, which represents a major milestone both for the importance of RWA, as well our first T1 exchange listing.

We have move exchange listings coming, stay tuned.

I’m betting my money on #Indonesia. I’ve spent the last year studying the language and preparing to move there.

Why? 👇

Because emerging markets have been ignored for far too long, and that’s about to change.

My generation won’t build wealth by competing over saturated Western assets. We’ll build it where growth is still exponential. I’ve already started — with real estate in Indonesia. Let me show you the difference 👇

Imagine a 1000 m² beachfront plot in Key West, Florida.

~$20M price tag, high taxes, high maintenance, high cost of living.

Now ask yourself: is that land going 10x from here? Or are you just hoping someone richer pays more for the same thing?

Now compare that to 🏝 Lombok, Indonesia. A 1000 m² beachfront plot goes for ~$50,000. On less developed islands, even ~$5/m². Same question: where is 10x more likely?

Bali (Canggu) already showed what happens when global demand meets cheap land — 20%+ Airbnb yields, massive appreciation, and the growth does not stop. Lombok is just getting started.

Rising living costs, globalisation and remote work are changing everything. People are leaving the West in masses. They choose Thailand, Vietnam, Indonesia... I’m one of them. HOWEVER, this tweet isn’t just about real estate.

Take #gold mining 🪙 in Alaska. You need licenses, expensive land, heavy machinery, and huge upfront capital, with no guarantee of profit.

Now look at Indonesia. In many regions, resources are still extracted manually by locals, inefficiently, with minimal technology. People carry materials for hours with no infrastructure or optimization.

Now imagine building roads, buying machinery, introducing logistics, AI systems. How much does cashflow increase? 2x? 10x? 100x?

This is the reality: a country of ~300M people, low labor costs, low taxes, low prices, massive natural resources, and huge inefficiencies everywhere.

So why isn’t everyone investing already? Because for individuals, it’s difficult. Bureaucracy, paid up capital requirements for company formation, language barriers, connections, corruption.

But that’s changing. #Tokenisation opens the door to borderless, all-size-capital access to these markets without needing to set up companies or move there.

This is where @ChintaiNetwork comes in. They recently closed a $28B deal in Indonesia (Maluku region), one of the largest tokenisation deals ever. https://t.co/6IiDHmcg5q

The goal is to tokenize and develop 710,000 km² across 1400 islands with 60-year development rights, spanning forestry, mining, agriculture, fisheries and many more.

This isn’t theory — it’s already happening, backed by experienced financial titans like former head of JP Morgan, former Vice President of finance of Airbus, and many more. The company behind this investment arm Maluku Forest I am talking about is

https://t.co/yQyCNBfFJz

And here’s the key: you don’t need connections, you don’t need to relocate, you can invest directly from your sofa. Registrations are already open, with an initial $200M allocation pledged to fill once the deal is opened.

If you’re looking at tokenisation as a sector, many projects are still down 96-99% from ATH due to uncertainty and crypto bear cycle, but some are actually delivering even during bear.

One example is $CHEX — the utility token of @ChintaiNexus, the same platform bringing deals like the $28B Maluku project. Licensed by Monetary Authority of MAS (#Singapore), with buybacks, staking, burning, and a secondary market for tokenised assets, tying value directly to company cashflow, it creates perfect risk/reward investment.

Current mcap of #CHEX is around $25M, down ~97% from ATH. And they’re also offering tokenised equity (~$84M valuation) for those who prefer a more traditional structure.

CEO @GunnisonCap with decades of experience in banking, finance, and project management, from companies like HSBC, Barclays, Credit Suisse, Goldman Sachs etc. and many other experienced team members are a guarantee for the success.

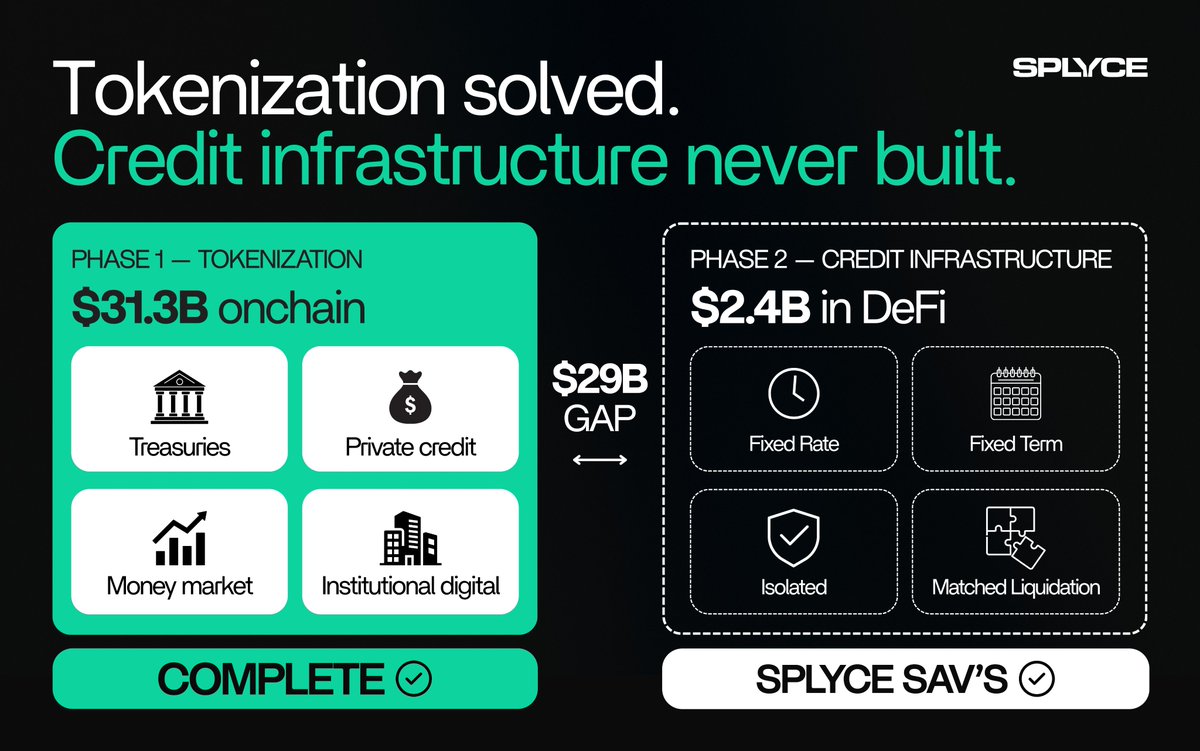

The tokenized asset market crossed $30 billion last month and has stayed there. Roughly the size of an elite university endowment.

As recently as mid-2024, it was below $3 billion. 10x in under two years.

What changed: the GENIUS Act, mature institutional onchain infrastructure, and a wave of financial institutions moving from pilots to production — all at roughly the same time.

$29B gap between what's tokenized onchain and what's active in DeFi.

Tokenization put the assets onchain. The credit infrastructure was never built.

Variable-rate pools assume collateral is fungible, prices are live and one liquidation logic fits every asset. None of that holds for institutional credit.

SAVs are the credit infrastructure.

Fixed rate. Fixed term. Isolated by borrower. Liquidation matched to the asset.

Built for the gap.

@ChintaiNexus has $4.6B in deal flow and has a Top 5 asset manager on their final leg of legal review. The CLARITY Act is the legal opinion their outside counsel has been waiting for.

Here's the recap of the AMA, hosted by @ChintaiNexus and featuring @GunnisonCap and @HumbleBarracuda.

Graphic explaining how @ChintaiNetwork and $CHEX will hugely benefit the passing of the #ClarityAct

BOTTOM LINE

> Legal clarity reduces regulatory risk

> Lowers compliance costs

> Opens institutional capital

> Expands issuer & bank participation

= ACCELERATES CHINTAI’S GROWTH

Here is the full picture/TLDR.

@ChintaiNetwork holds dual MAS licenses in Singapore, runs a permissioned L1 blockchain, operates white-label platforms for dozens of financial institutions, and has confirmed $4.6B in deal flow, with seven clients having already tokenized $668M on-chain.

@EYnews projects that tokenized assets will reach $28 trillion by 2030. The global capital markets universe is $270 trillion. RWA tokenization is still at $33 billion.

The gap between where we are and where this goes is where @ChintaiNetwork and their partners are operating.

CLARITY is the regulatory green light. The platforms that built compliant infrastructure before the rules arrived do not just participate in this market; they also lead it. They become the market.

The CLARITY Act is one of the most significant regulatory developments for real-world asset tokenization in history. I wanted to break down what it actually means for @ChintaiNetwork, the businesses building on its platform, and the $28 trillion market they are positioned to capture.

@ArchNtwrk and @ChintaiNetwork are collaborating to bring RWAs onto Bitcoin natively through @HoneyB_BTC, a platform that allows investors to access yield-bearing opportunities via regulated RWA tokenization denominated in Bitcoin. This is a meaningful step because it extends Chintai's compliance infrastructure into the Bitcoin ecosystem without bridging or wrapping assets.

CLARITY's mature blockchain certification pathway under Section 205 establishes a formal process for certifying a blockchain system as sufficiently mature to support digital commodity classification. That pathway is directly relevant to legitimizing the kind of multi-chain infrastructure Chintai and Arch are building together.

Check out https://t.co/wcuhwCHXiq, with @loancyborg at the helm.

the Clarity Act keeps coming up and most people don't know what it actually means

simple version:

right now nobody in crypto knows who's in charge the SEC and CFTC have been fighting over jurisdiction for years different tokens, different rules, different regulators nobody can get a straight answer

the Clarity Act draws a clean line digital assets get their own regulatory framework clear rules on who regulates what

why does this matter?

because institutions won't commit serious capital to markets with regulatory ambiguity compliance teams won't sign off boards won't approve it

clear rules = real capital

tokenisation, onchain lending, RWA infrastructure all of it accelerates the moment this passes

that's the window everyone at consensus was talking about

and it's closer than most people think