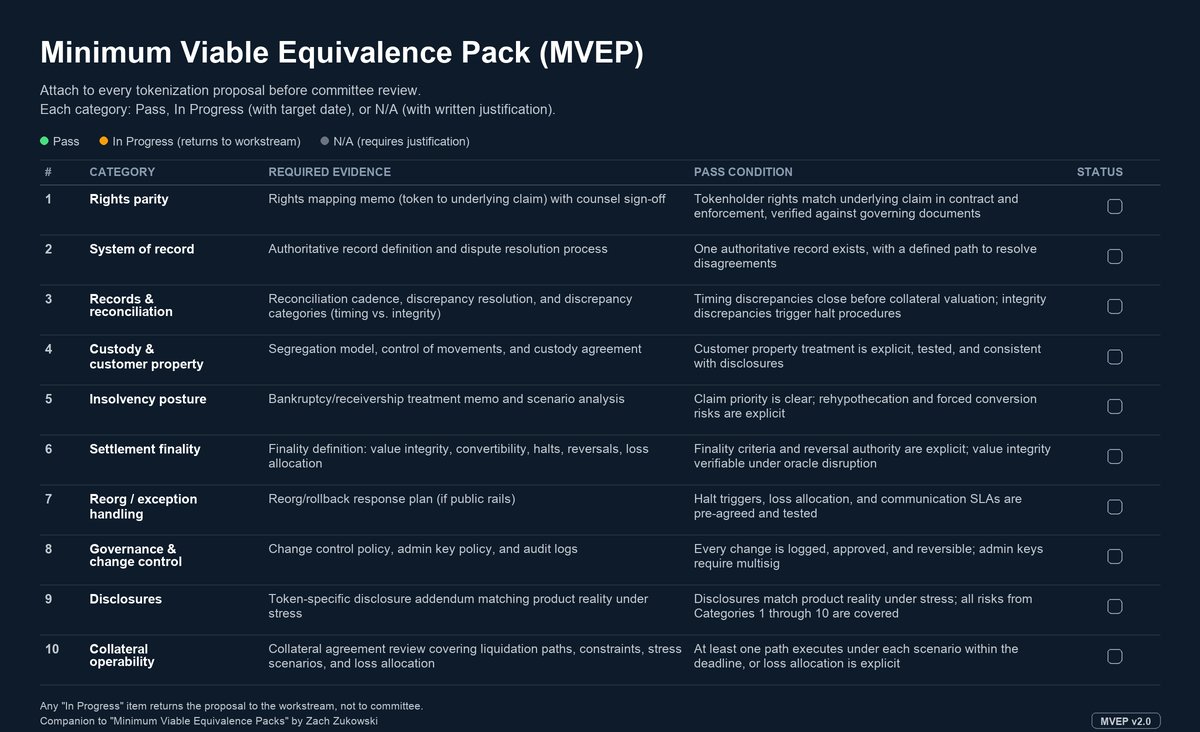

A margin call triggers at 2am Saturday. The tokenized Treasury posts as collateral instantly. Liquidating it to cash is a different problem. The redemption pool may be depleted. The secondary market may have no active makers at 2am. The fund administrator does not process redemptions until Monday. MVEP v2.0 is the diligence framework for this problem. Ten categories, each with required evidence and a pass condition. Reverse-engineered from SVB, stress-tested against seven scenarios. Updated paper on SSRN, updated article on Medium. #Tokenization

The explicit exclusion of stablecoin-handling activities is the most consequential boundary in the statement. It leaves the largest segment of the tokenized asset market outside the conduct framework developed here. Worth watching whether a parallel regime emerges for payment stablecoin interfaces, or whether this boundary hardens.

@EleanorTerrett@ABABankers Banks fighting to maintain their business when much better tech exists. Lending will migrate to neobanks like it did in 2008-2009.

Before 2008, rating agencies treated mortgage-backed instruments with different credit profiles as equivalent within the same tranche. Today, collateral frameworks treat tokenized Treasury products with different legal structures as equivalent within the same margin pool. Three products. Three different sets of rules. One custodian. No federal regulator supervises the boundary where they are combined. Submitted a comment to the OCC on the GENIUS Act rule explaining why that matters.

#USYC #BUIDL #BENJI #GENIUSAct #stablecoins #tokenization #OCC

A margin call triggers at 2am Saturday. The tokenized Treasury posts as collateral instantly. Liquidating it to cash is a different problem. The redemption pool may be depleted. The secondary market may have no active makers at 2am. The fund administrator does not process redemptions until Monday. MVEP v2.0 is the diligence framework for this problem. Ten categories, each with required evidence and a pass condition. Reverse-engineered from SVB, stress-tested against seven scenarios. Updated paper on SSRN, updated article on Medium. #Tokenization

13/13

Paper: https://t.co/ItEOeTtOCK package: https://t.co/FJwKlWpsmX

Prepared for the Fifth Conference on the International Roles of the U.S. Dollar.

Feedback especially welcome on where the gateway thesis should break.

#Stablecoins#USDC#USDT#DeFi#MonetaryPolicy #FederalReserve #CryptoRegulation #FinancialStability #GENIUSAct #CLARITYAct

1/13

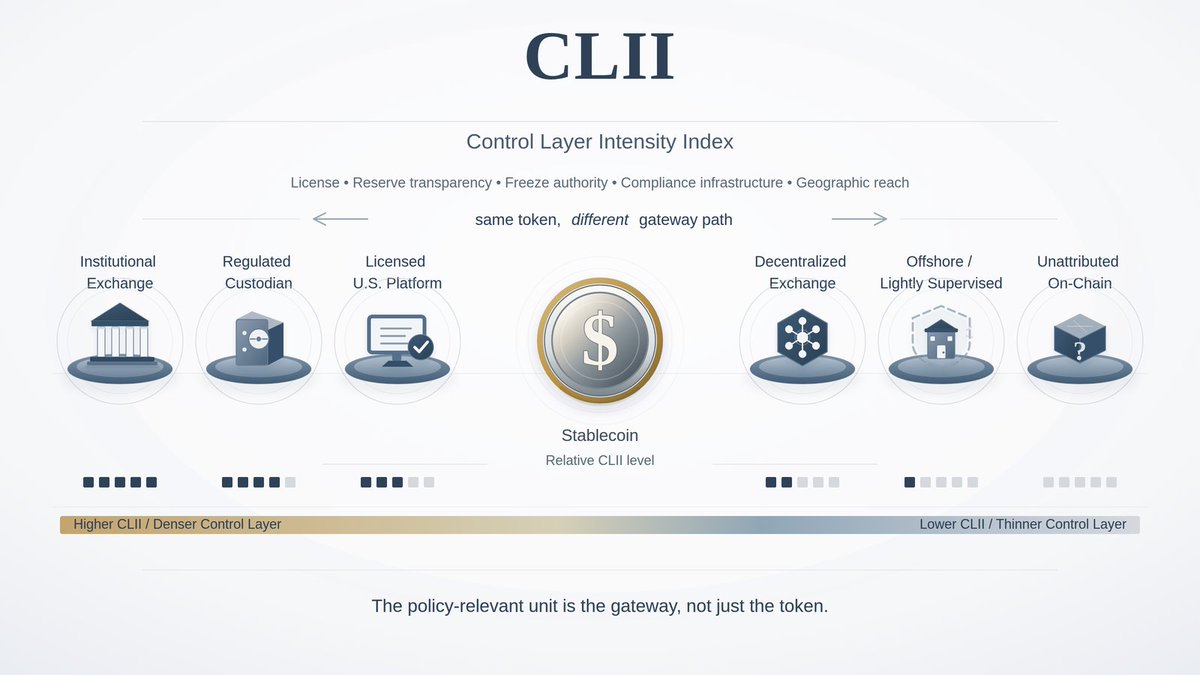

USDC through Coinbase and USDC through a Tron DEX are the same token. They are not the same financial product.

New paper: "Routing the Dollar." The policy-relevant unit isn't the stablecoin. It's the gateway that routes it.

https://t.co/0r5pVIhHtJ

12/13

None of that is visible in token-level data.

You would see USDC falling and USDT rising.

You wouldn't see Curve 3pool becoming an emergency valve, one market-maker becoming a key bridge, or Tier 1 share collapsing over a weekend.

Monitoring stablecoins at the token level is like monitoring the banking system by watching cash. You see the instrument moving. You don't see which bank handled it, whether that bank was supervised, or whether the whole system depended on one clearinghouse that nobody was watching.