Frank Head of Cyprx Research Lab | Exclusive insights on Blockchain, Geopolitics, Web3 & DeFi | Join us in exploring the future of finance & technology!

If you’re serious about crypto, trading, or DeFi, Cyprx is one of the most comprehensive research communities you can join.

Here we go down rabbit holes most people don’t even know exist backed by one of the largest curated libraries in the space.

💎 Non-mainstream research

💎 Real-time macro & institutional breakdowns

💎 Institutional-grade technicals

💎 4–6 private Zoom calls weekly

💎 Hundreds of educational docs

💎 A huge esoteric & awakening archive

No hopium.

No recycled Twitter noise.

Just real insight for people ready to level up financially, mentally & spiritually. 👇🏼

Institutional wallet infrastructure is becoming far more than “crypto custody.”

Modern MPC wallet architecture is evolving into a full operating layer for digital finance

The next generation stack combines:

- MPC-based distributed signing

- multi-chain wallet infrastructure

- policy-driven approvals

- HSM and secure enclave integrations

- compliance and risk monitoring

- treasury orchestration

- cloud-native scalability

The important shift:

Security alone is no longer enough.

Institutions now need systems that combine:

- governance

- compliance

- operational resilience

- usability

- programmable controls

Across stablecoins, tokenized assets, treasury operations, and onchain finance.

As digital asset adoption grows, the wallet increasingly becomes:

Not just a storage layer but the control layer for institutional finance itself.

A very important signal from the Financial Conduct Authority and Bank of England

The tokenization conversation is shifting from experimentation into market infrastructure.

The new FCA/BoE framework discussions focus on:

- tokenized collateral

- digital asset issuance + exchange

- prudential treatment

- settlement infrastructure

- central bank money settlement

- near 24/7 RTGS and CHAPS operations

That matters because tokenization is not only about putting assets onchain.

It’s about redesigning:

- issuance

- settlement

- liquidity

- collateral mobility

- market operating hours

- financial market infrastructure itself

One key takeaway:

Regulators are no longer asking if tokenization matters.

They are now working on:

“How do wholesale markets operate safely once tokenized assets, programmable settlement, and digital money become part of core infrastructure?”

That is a major shift.

Tokenized deposits are moving beyond payments.

They are becoming collateral infrastructure for institutional finance 👇

New architectures combining Canton Network + Hyperledger Fabric show how programmable bank money can support:

- collateral mobility

- atomic financing

- margining

- settlement coordination

- cross-chain interoperability

The important shift:

Collateral is no longer static.

Tokenized deposits can now:

- move in near real-time

- remain programmable

- settle atomically

- integrate directly into lending and treasury workflows

The flow increasingly looks like:

deposit, token minting, collateral pledge, automated financing, real-time settlement.

And technologies like DAML smart contracts & interoperability layers are making this operationally viable inside regulated environments.

This matters because institutional tokenization is not only about assets.

It’s about rebuilding:

- liquidity management

- collateral efficiency

- settlement infrastructure

- counterparty coordination

Around programmable financial systems.

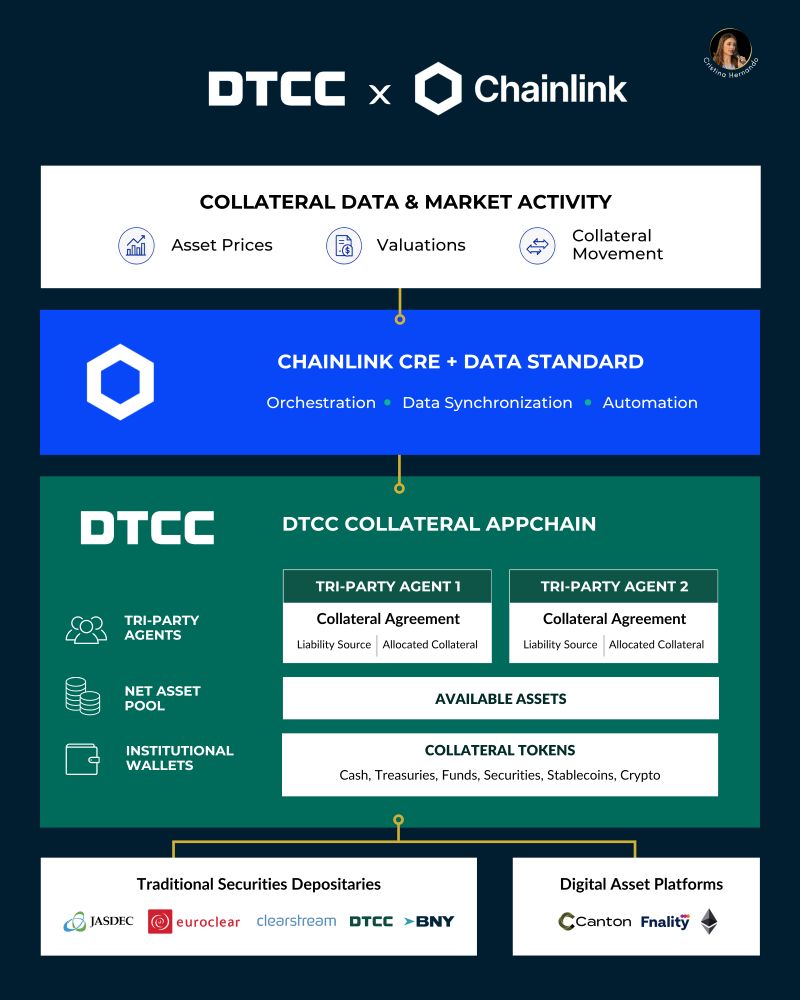

DTCC integrating Chainlink CRE into its Collateral AppChain is a much bigger signal than it first appears 👇

The focus is not “tokenized assets” alone.

It’s operationalizing collateral markets at institutional scale.

The platform is designed to support near real-time collateral workflows across:

- eligibility

- valuation

- margining

- collateral optimization

- settlement

- post-trade operations

That matters because collateral sits at the core of financial market plumbing.

And tokenization cannot scale institutionally without:

- trusted data standards

- interoperable workflows

- synchronized settlement coordination

The timeline around CRE is also telling:

2024: Swift explores cross-chain workflows with Citi, BNP Paribas, Euroclear

2025: UBS, Franklin Templeton, and JPMorgan Kinexys begin using CRE-related workflows

2026: DTCC integrates CRE into collateral infrastructure

The industry is gradually moving from tokenization experiments…

…toward coordinated market infrastructure.

Compliance is quietly becoming one of the biggest competitive moats in financial services

What used to be treated as a back-office cost center is evolving into a real-time intelligence layer across:

- onboarding

- payments

- fraud

- AML

- transaction monitoring

- customer risk

The problem:

Most institutions still run compliance through fragmented systems.

Result:

- duplicate alerts

- inconsistent risk scoring

- disconnected investigations

- siloed customer data

- analysts jumping between dashboards with no unified view

Financial crime does not happen in silos.

But compliance operations often still do.

The next phase is likely a shared intelligence layer connecting:

identity, transactions, behavior, investigations and risk.

And this becomes even more important with AI agents.

Because deploying AI on top of fragmented compliance infrastructure doesn’t solve the problem.

It simply automates fragmented decision-making.

Compliance is quietly becoming one of the biggest competitive moats in financial services.

What used to be treated as a back-office cost center is evolving into a real-time intelligence layer across:

- onboarding

- payments

- fraud

- AML

- transaction monitoring

- customer risk

The problem:

Most institutions still run compliance through fragmented systems.

Result:

- duplicate alerts

- inconsistent risk scoring

- disconnected investigations

- siloed customer data

- analysts jumping between dashboards with no unified view

Financial crime does not happen in silos.

But compliance operations often still do.

The next phase is likely a shared intelligence layer connecting:

identity, transactions, behavior, investigations and risk.

And this becomes even more important with AI agents.

Because deploying AI on top of fragmented compliance infrastructure doesn’t solve the problem.

It simply automates fragmented decision-making.

Most people describe tokenization as:

“Take an asset. Issue a token. Put it onchain.”

In reality, tokenization looks much closer to building a miniature financial system around the asset itself.

Before any smart contract exists, teams must define:

- what economic rights the token represents

- which regulations apply

- how custody works

- who can hold it

- how transfers settle

- how compliance is enforced

Then comes the infrastructure layer:

- issuance

- custody

- pricing

- liquidity

- interoperability

- settlement

- secondary markets

Without those layers, a tokenized asset is just an isolated database entry.

That’s why companies like:

Securitize, Tokeny, Ondo Finance, Centrifuge, Fireblocks, Chainlink, and tZERO are building entire layers of the emerging stack.

The important shift:

Once assets become programmable, finance itself starts behaving differently.

Settlement becomes faster.

Collateral becomes mobile.

Yield becomes automated.

Markets become interoperable.

Tokenization is not just “putting assets on blockchain.”

It’s the gradual rebuilding of financial infrastructure into programmable systems.

The tokenization discussion is evolving.

The real challenge is no longer only:

“How do we tokenize assets?”

It’s:

“How do tokenized assets actually settle?”

Every tokenized bond, fund, or Treasury product still needs a cash leg.

That means deciding between:

- stablecoins

- tokenized deposits

- central bank money

- or traditional fiat rails connected externally

And that decision shapes:

- regulation

- liquidity

- interoperability

- settlement finality

- counterparty risk

This is where firms like JPMorgan Kinexys become important.

Because tokenization is moving beyond issuance…

…and into the mechanics of market infrastructure itself.

The opportunity is not just digital assets.

It’s programmable settlement:

✓ atomic DvP

✓ near real-time finality

✓ synchronized cash + asset transfer

✓ reduced reconciliation layers

The future likely won’t run on:

one chain, one token, or one settlement model.

It will be an interoperable financial environment where assets, cash, and existing banking rails operate together.

A lot of people think Web3 funding disappeared.

It didn’t.

Capital simply moved from speculation to infrastructure

The companies raising $100M+ now are not “whitepaper projects.”

They’re building:

- payments infrastructure

- tokenized finance

- cross-chain interoperability

- institutional custody

- DeFi lending

- modular blockchain infrastructure

- prediction markets

- developer tooling

Examples:

Phantom

Morpho

Ondo Finance

Circle

Fireblocks

LayerZero Labs

Wormhole

Alchemy

Celestia

The interesting shift:

Investors increasingly care less about narratives and more about:

- real users

- liquidity

- revenue

- distribution

- infrastructure control

Web3 funding didn’t slow down.

It matured.

European Central Bank President Christine Lagarde just framed the stablecoin debate in a much bigger way.

The issue is no longer only innovation.

It’s monetary sovereignty.

Today, the stablecoin market exceeds $300B and remains overwhelmingly USD-denominated, dominated by Tether and Circle.

Lagarde’s warning:

Europe risks “digital dollarisation” if dollar-backed stablecoins become the default settlement asset for digital finance and tokenized markets.

An important distinction she made:

Stablecoins serve two different functions:

Monetary: store/transfer of value

Technological: settlement asset on blockchain infrastructure

And Europe’s position is becoming clearer:

The ECB wants tokenized financial infrastructure but anchored in central bank money, not dependent on private dollar stablecoins.

Projects like Pontes and Appia reflect that direction:

programmable settlement, interoperability, and tokenized finance without surrendering monetary control.

The bigger question:

Will the future digital financial system run on:

- private stablecoins

- tokenized bank deposits

- wholesale CBDCs

- or a hybrid model combining all three?

The future of stablecoins will not be defined by issuance alone.

It will be defined by infrastructure

The next generation of digital payment architecture is converging:

- stablecoins

- banking rails

- compliance systems

- DeFi connectivity

- real-time settlement

- institutional governance

A compliant digital money stack now includes:

- onboarding + collateral verification

- token issuance and redemption

- multi-chain circulation

- AML/KYC + regulatory reporting

- banking + escrow integration

- merchant + P2P payments

- automated audit trails

The important shift:

Stablecoins are evolving from standalone crypto assets into regulated financial operating infrastructure.

The winners likely won’t just issue tokens.

They’ll control:

- settlement coordination

- compliance orchestration

- liquidity routing

- banking connectivity

- cross-chain interoperability

The stablecoin conversation is still too USD-centric.

Today, Tether and USD Coin dominate because the dollar dominates global liquidity.

But if stablecoins become part of:

- daily payments

- treasury operations

- institutional settlement

- cross-border commerce

Then the market structure becomes much bigger.

The real question may not be:

“Which stablecoin wins?”

But:

How do different forms of digital money connect?

CBDCs.

- Licensed stablecoins.

- Tokenized bank deposits.

- Multi-currency settlement layers.

Because once multiple digital money systems exist, the market needs:

- routing

- FX conversion

- compliance coordination

- trusted settlement paths

- interoperability across networks and jurisdictions

The most valuable layer may not be the token itself.

It may be the infrastructure coordinating movement between currencies, issuers, banks, and payment networks.

The future of digital money may look less like one dominant coin and more like a global orchestration layer for many forms of programmable money.

A very important signal from the Bank of England and Bank for International Settlements

The new DLT Innovation Challenge report focuses on a critical question for financial markets:

Can wholesale central bank money settle securely on programmable external ledgers?

The answer is becoming less theoretical and far more infrastructural.

Key themes:

- settlement finality across DLT environments

- interoperability between DLT + RTGS systems

- governance and compliance controls

- scalability for institutional transaction volumes

One takeaway stands out:

There is no “perfect” DLT architecture.

Every design involves trade-offs between:

speed, decentralization, governance, resilience, interoperability, and trust.

The bigger shift:

Tokenized finance is forcing traditional financial market infrastructure and programmable ledgers to converge.

The future likely won’t be:

“traditional finance vs blockchain.”

It will be interoperable market infrastructure combining both.

Most people think blockchain will replace traditional payment rails.

It won’t.

The real shift is orchestration

ISO 20022 messaging, RTGS systems like Fedwire and TARGET2, and existing bank infrastructure are not disappearing.

What changes is the settlement layer:

- atomic PvP/DvP settlement

- 24/7 availability

- real-time regulatory visibility

- deterministic finality instead of reconciliation delays

The future of payments is not “crypto vs banks.”

It’s interoperable financial infrastructure.

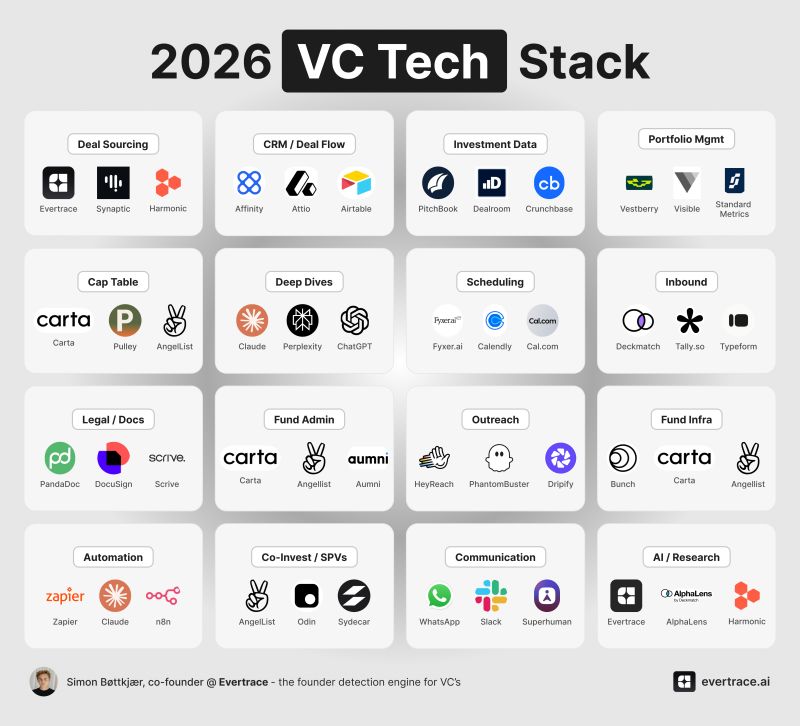

The modern VC firm is starting to look less like a partnership…

…and more like an operating system 👇

The 2026 VC stack now spans:

- sourcing

- research

- CRM

- portfolio analytics

- legal workflows

- fund infrastructure

- automation

- AI copilots

Tools like:

Affinity, PitchBook, Carta, Claude, ChatGPT, Perplexity, Zapier, and n8n are becoming core infrastructure.

The interesting shift:

VC advantage is moving beyond access to capital.

It’s increasingly about:

- information velocity

- workflow automation

- relationship intelligence

- proprietary data networks

- AI-assisted decisioning

The next top-tier VC firms may operate less like traditional investors…

…and more like AI-native financial platforms.

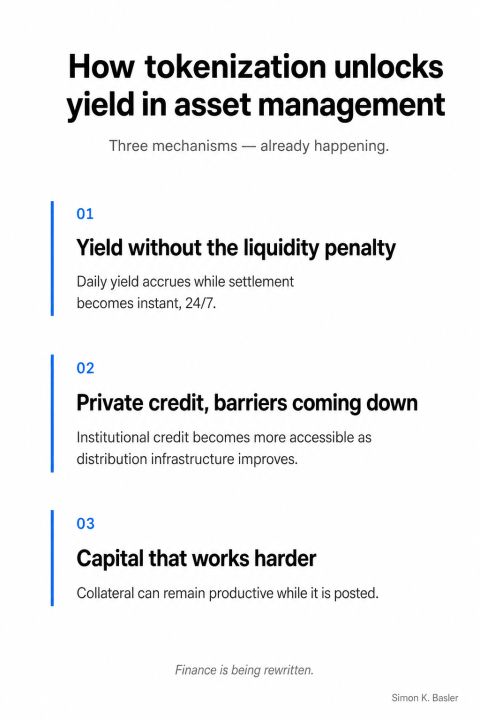

Tokenization is not just putting assets onchain.

It’s changing how yield, liquidity, and collateral work inside financial markets.

Three shifts stand out:

Yield without sacrificing liquidity

Tokenized money market funds now combine:

- daily yield accrual

- near real-time settlement

- 24/7 transferability

Examples:

BlackRock BUIDL, Franklin Templeton BENJI, JPMorgan Kinexys.

Private credit access is expanding

Tokenization lowers distribution barriers around institutional credit products.

The innovation is not “lower risk.”

It’s broader access + programmable infrastructure.

Collateral can now remain productive

Institutions increasingly use tokenized MMFs as collateral while still earning yield.

Same exposure.

Higher capital efficiency.

The important point:

These are not just crypto products.

They are new financial infrastructure layers for:

- liquidity

- collateral mobility

- treasury management

- capital efficiency

The yield story may attract attention first.

But the real battle is likely over:

settlement rails, custody infrastructure, and distribution controle.

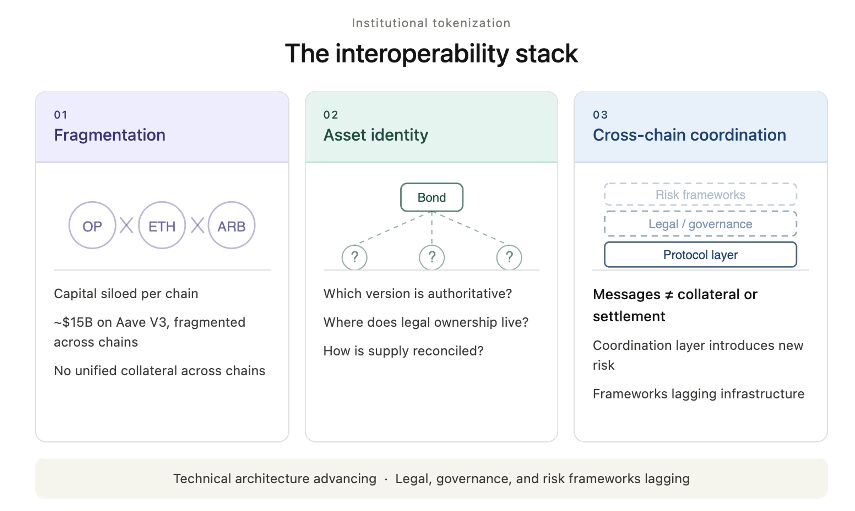

Tokenization will not happen on one chain.

It will happen across many chains.

And that makes interoperability one of the most important infrastructure problems in digital finance

The challenge is not just moving messages cross-chain.

It’s coordinating:

- collateral

- ownership

- settlement finality

- legal identity

- risk

Today, a position on one chain is often isolated from another.

Even on Aave:

ETH supplied on Optimism does not automatically provide borrowing power on Arbitrum.

That fragmentation limits liquidity efficiency at institutional scale.

Then comes the harder problem:

How do institutions know which cross-chain asset representation is the authoritative one?

Protocols like Chainlink CCIP, LayerZero, Wormhole, and Axelar are trying to solve parts of this.

But interoperability is not only a technical problem.

It is a coordination, identity, governance, and trust problem.

And events like the Kelp DAO exploit showed exactly how fragile that trust layer can become when cross-chain assumptions fail.

Tokenization is entering a new phase

The story is no longer just:

“What assets can move onchain?”

It’s:

How do tokenized funds, collateral, stablecoin settlement, and regulated infrastructure connect into real financial workflows?

Recent signals:

BlackRock: filing tokenized fund structures using Securitize infrastructure

DTCC: expanding collateral infrastructure with Chainlink Labs.

Circle: raising capital for Arc

Franklin Templeton: expanding tokenized investment partnerships

The common thread:

Tokenization is moving from isolated digital assets into financial operating infrastructure.

- Funds.

-Collateral.

- Settlement.

- Custody.

- Transfer agency.

- Investor eligibility.

- Treasury workflows.

That’s where institutional adoption becomes durable:

not when assets are merely tokenized…

but when they integrate into the systems markets already depend on.

Cross-border payments are changing because blockchain changes the architecture behind settlement.

Instead of routing messages bank to bank to bank:

- transactions are validated by distributed nodes

- recorded on a shared ledger

- and settled on a synchronized infrastructure layer

The result:

- fewer intermediaries

- real-time visibility

- immutable audit trails

- programmable execution via smart contracts

Institutional players often use permissioned blockchains for controlled access, compliance, and high-value settlement.

Fintechs and SMEs increasingly use permissionless networks for:

- faster global transfers

- lower costs

- broader financial access

- transparent payment tracking

The important shift:

Blockchain is not just a new payment rail.

It’s a new coordination model for how financial institutions, businesses, and payment systems share data, validate transactions, and settle value globally.