par•lay. (ˈpɑr leɪ, -li) v.t. 1. to bet or gamble (an original amount and its winnings) on a subsequent contest. 2. to use (assets) to achieve a relatively great gain: to parlay a modest inheritance into a fortune. n. 3. a bet of an original sum and the subsequent winnings.

Silver dropped almost 50% from June 1968 to November 1971, and then rallied ~420% into February 1974.

Silver then dropped ~43% into 1976 and then rallied ~1150% by January 1980.

Silver dropped 60% from March to October 2008 and then rallied ~490%.

Gold dropped almost 30% in late-1973 and then rallied almost 100%...and then dropped ~25% and then rallied another 45% all by January 1975.

Gold dropped 50% in 1975 and 1976 and then rallied ~770% by Jan 1980.

Gold dropped ~26% in 2006 and then rallied 90%.

Gold dropped ~35% in 2008 and then rallied 180%.

This sell-off since January 2026 is now the third largest silver has ever had within the context of a bull market, and for gold it's the the fourth largest...almost on par with the 1973 correction and nearly on par with the Great Financial Crisis. In terms of time from top to bottom, this is more akin to the 1973 correction (about 20 weeks) or 2006 (about 20 weeks).

All of these drops led to enormous V-bottom rallies, some so rapid that if they repeated today it would mean $8000+ gold by October.

$FOR.V $FTBYF - FORTUNE BAY CORP.

FOR stands out as my top pick from a field of 40+ candidates in my most recent research pass. Here's why:

Core Asset – Goldstrike (USA)

1.2 Moz gold resource at a solid 1.3 g/t grade, situated in a Tier 1 jurisdiction

Exceptional resource confidence: 97% of ounces are in the Indicated category

Advanced development stage with MRE, PEA, and EIS complete, First Nations consent secured, and PFS on the horizon

Management & Capital Structure

Strong CEO and Chairman with meaningful skin in the game — insider buying only, zero selling

Very tight share structure for a junior

Market cap priced like an explorer despite developer-stage fundamentals — implies at least 3x upside on a peer comparison basis, making it a credible M&A target

Near-Term Catalysts

Ongoing assays expected to grow the 1.2 Moz resource at higher grades

Bonus Assets

Mexico: 1.74 Moz gold + 6.7 Moz silver with high-grade intercepts

Porphyry: 600m of 0.28% Cu and 0.68 g/t gold from surface

Uranium: JV or royalty exposure adding further optionality

Bottom line

A rare combination of resource quality, jurisdictional safety, management alignment, and valuation disconnect. Solid pick.

$FOR.V - FORTUNE BAY CORP.

I took a position in FOR. 69.9M shares. No debt. Tight structure. Maximum leverage to gold. MRE done. PEA done. PFS soon.

The worth: Market cap: C$54M. NPV at spot gold (US$4,535): C$1.8B. That's 3 cents on the dollar.

The asset: 1.2 Moz gold in Saskatchewan — #3 jurisdiction globally. 97% Indicated. Approved EIS since 2008. Written First Nations consent through DFS. PEA done. PFS executing now, completion YE2026/Q1 2027.

The man: Wade Dawe owns ~15% and has already sold two companies for C$400M+. He bought C$445K of stock personally in 2025 at C$0.32. Now C$0.77. He's not done.

The catalysts: 700+ assays in the lab from targets outside the current resource. Manhattan Uranium drilling 25 targets on Fortune Bay's land right now. PFS completion in 6–9 months opens M&A conversations.

The precedent: Fresnillo paid C$780M for Probe Gold in January 2026 — same stage, same jurisdiction, 39% premium. At 0.20× NAV, FOR's takeout value is C$7–11/share.

You can all the angles on FOR below, the detailed research however is in the research document on https://t.co/vVk3nTwRkg.

The Discount Angle

C$54M market cap. C$1.8B NPV at spot gold. That's 3 cents on the dollar. Even if you haircut everything by 50% for development risk, you're still paying 6 cents. Name another Canadian gold developer priced this cheap.

The Gold Leverage Angle

Every US$100 move in gold = C$61M change in NPV. Gold is at US$4,535. The PEA was modelled at US$2,600. The bull case is now spot. The stock hasn't moved. FOR is a leveraged gold call option with a 13.9-year mine life underneath it.

The M&A Angle

Fresnillo bought Probe Gold in January 2026 for C$780M — 0.2–0.3× NAV, 39% premium. Same stage, same jurisdiction quality. At 0.20× NAV, FOR's takeout value is C$7–11/share. Current price: C$0.77. The chairman has already done this twice.

The De-Risking Angle

97% Indicated resource. Approved Environmental Impact Statement since 2008. Written First Nations consent through Definitive Feasibility Study. Saskatchewan — #3 mining jurisdiction globally. Every 2026 technical workstream returning clean data. This is not a speculative explorer. It's a developer where the hard work is already done.

The Operator Pedigree Angle

Wade Dawe built and sold Brigus Gold for ~C$350M at a 45% premium. Then built and sold Keeper Resources for C$51.6M all-cash. He's doing it again at Fortune Bay — same playbook, same jurisdiction category, bigger gold price backdrop. He bought C$445K of stock personally at C$0.32. Now C$0.77. Still cheap.

The Unpriced Upside Angle

The PEA modelled a doré flowsheet. New met results show >50% gold to gravity concentrate at 0.08% feed mass, >90% flotation recovery.

If the PFS switches to concentrate, AISC drops materially vs the PEA base case. The market has priced zero of this.

Add Golden Pond (all 7 holes hit, 578 assays pending), the Box down-dip extension at 3.70 g/t over 21m outside the MRE, and an underground scenario not in any economic model. The PEA is the floor, not the ceiling.

The Resource Angle

989,600 oz Indicated at 1.28 g/t Au. 214,200 oz Inferred at 0.90 g/t. Total 1.2 Moz — and 97% of the mine plan is already Indicated.

That's not a conceptual resource. It's 838 drill holes over 80,000m, reconciled to within 1% of 64,000 oz of actual historical production from the same ore body. And it's about to get much bigger. Some step-outs:

+ 3.70 g/t over 21.0m (incl. 9.89 g/t over 7.0m)

+ 6.95 g/t / 3.72 g/t / 4.55 g/t stacked + 8.72 g/t over 2.0m

+ 2.54 g/t over 17.0m (incl. 6.61 g/t over 5.0m)

+ 1.20 g/t over 23.2m (incl. 4.68 g/t over 3.2m, 12.20 g/t over 1.0m)

+ 2.06 g/t over 6.88m

+ 8.95 g/t over 1.0m

+ 16.53 g/t over 13.6m.

578 assays still in the lab. Frontier: 135 assays pending. Athona West: not yet drilled. The 2 km gap between Box and Athona almost entirely undrilled. Updated MRE hits in 2027. None of the expansion ounces are in the current PEA economics.

The Hidden Optionality Angle

Nobody is talking about Mexico.

Fortune Bay holds 100% of the 4,176 ha Rio Negro concession in Chiapas — valid until 2051, no royalties, no back-in rights. Prior operators (Linear Gold, then Kinross) drilled 89,000m in 342 holes focused entirely on near-surface epithermal gold.

Historical resource: 1.74 Moz Au + 6.7 Moz Ag (M&I + Inferred). High-grade historical intercepts: 100m @ 12 g/t Au & 64 g/t Ag at Campamento; 22m @ 10 g/t Au at Laguna Chica.

Nobody drilled the porphyry underneath.

One hole — IXM08-51 — intersected 601.4m @ 0.28% Cu / 0.68 g/t Au / 2.71 g/t Ag from surface. That's the upper halo of a district-scale copper-gold-silver-molybdenum porphyry system. The geological setting parallels Grasberg and Bingham Canyon at the district scale. No focused copper exploration has ever been conducted. The buried porphyry has never been drill-tested.

This asset is valued at approximately zero in every model. It's not needed for the Goldfields thesis to work. It's not in any analyst's numbers.

It's just sitting there.

The Jurisdiction Angle

Saskatchewan is #3 mining jurisdiction globally (Fraser Institute 2025). Royalty and taxation framework unchanged since 2006. Regulators who actively want mining to happen — Verran's own words: "It's so nice to talk to regulators who listen and want to broaden their mineral economy."

No indigenous land claim uncertainty, no federal impact assessment (below 5,000 tpd threshold), no permitting lottery. Compare that to Nevada title disputes, Quebec court injunctions, or anything in West Africa. The jurisdiction risk premium the market is applying to FOR is essentially zero — because it should be.

The Infrastructure Angle

This is not a greenfield project in the middle of nowhere. Road to the Box deposit. Active hydro powerline. Airport at Uranium City 13 km away. Existing camp and facilities. Multiple operating uranium mines within 350 km with comparable logistics. The 2008 feasibility study already designed the mine — Fortune Bay is updating it, not starting from scratch. C$301M capex looks different when the site prep is already done.

The Tight Share Structure Angle

69.9M shares outstanding. FD ~82.2M. In a junior mining peer group where 300–400M share counts are routine, Fortune Bay is surgical. Every dollar of value creation hits fewer shares. In a re-rating scenario — PFS completion, M&A approach, gold breakout — the per-share leverage is maximum. Dawe knows exactly what he's doing keeping the count tight.

The Uranium Kicker Angle

Most investors in FOR have no idea there's a uranium portfolio attached. Manhattan Uranium (TSXV: MANU) is drilling up to 25 targets at Murmac & Strike right now — June 2026, fully funded, largest program to date. Best hole to date: M24-017 returned 8.4m @ 0.30% U₃O₈ including 1.20m @ 1.79% U₃O₈, with individual assays up to 13.80% U₃O₈ — textbook Athabasca unconformity geometry. If Manhattan hits a discovery, FOR holds the underlying land and collects either a JV interest or NSR royalties. A uranium discovery on optioned land costs Fortune Bay shareholders nothing. It's a free lottery ticket on the hottest uranium basin in the world.

The Cheapest MCap/NPV Angle

Canadian gold developers routinely trade at 5–10% of NPV. Fortune Bay is at 3%. The peer set — Amex Exploration, NexGold, Getchell — all trade at multiples of FOR's MCap/NPV ratio. The discount has not narrowed as gold has run from US$2,600 to US$4,535. It has widened. Every week that passes without a re-rating is another week of compounding undervaluation against a rising gold price backdrop. At some point the gap closes. It always does.

The Bankable Resource Angle

The most de-risked PEA-stage resource in the Canadian peer group. 97% of the mine plan is Indicated — not Inferred, not historical, not conceptual.

989,600 oz Indicated across 24.0 Mt at 1.28 g/t, drilled in 838 holes over 80,000m, reconciled to within 1% of 64,000 oz of actual underground production from the Box Mine (1939–1942). SRK Consulting signed it. Ausenco is building the PFS on top of it. This resource is bankable today. The PFS makes it financeable.

The Permitting Fast Lane Angle

A provincially approved Environmental Impact Statement has existed for a 5,000 tpd open-pit operation at this exact site since 2008. The PEA's 4,950 tpd throughput is designed to stay below the federal impact assessment trigger — provincial permitting only. A First Nations Exploration Agreement signed November 2022 grants documented written consent through to and including Definitive Feasibility Study. That is not "community engagement ongoing." That is pre-existing written consent covering the entire study sequence. Pam Bennett has personally navigated the Saskatchewan permitting system on 14 mining projects. The permitting pathway is not a risk. It's a competitive advantage.

The Catalyst Runway Angle

The PFS isn't the only catalyst. It's the last one in a sequence that's already running.

Between now and PFS completion (YE2026 / Q1 2027), every quarter delivers:

Imminent:

Manhattan Uranium drilling up to 25 targets at Murmac & Strike — mobilisation confirmed June 4, 2026. Results H2 2026.

Neu Horizon Uranium ASX listing ~June 29, 2026 — A$15M IPO, funded partner for The Woods uranium option.

578 Golden Pond assays still in the lab. All 7 holes already confirmed gold. Historical hole in same area: 16.53 g/t over 13.6m. When these land, the resource footprint expands visibly.

135 Frontier assays pending — first data from an untested target.

Summer 2026:

Athona geotechnical drilling (4 holes, ~400m) — PFS-level data for the second pit, which is 25% of the mine plan.

Athona West drilling — tests the 2 km undrilled gap between Box and Athona. High impact if it hits.

Concentrate trade-off study output — does the PFS switch from doré to concentrate? If yes, AISC drops materially vs the PEA baseline.

Phase 2 waste rock kinetic testing results — confirms the acid generation profile for permitting.

H2 2026:

Poma Rosa amparo ruling — binary outcome, upside if successful.

Manhattan uranium drill results — discovery scenario adds a narrative the market hasn't priced.

YE2026 / Q1 2027:

PFS completion (Ausenco-led). This is the document that makes the asset financeable, enables institutional capital, and opens M&A conversations with majors. Dawe doesn't need a buyer before the PFS. He needs the PFS to start the conversation.

2027:

Updated MRE incorporating all 2026 drilling — Box extensions, Golden Pond, Frontier, Athona West. First time the market sees what the resource actually looks like post-expansion drilling.

Saskatchewan regulatory permitting advancement building on the 2008 EIS.

Strategic partner / JV / M&A conversations get serious. Probe/Fresnillo closed January 2026 — majors are actively buying Canadian developers at 0.2–0.3× NAV.

The stock is at C$0.77. The next six months deliver more data than most juniors produce in three years. None of it is priced in.

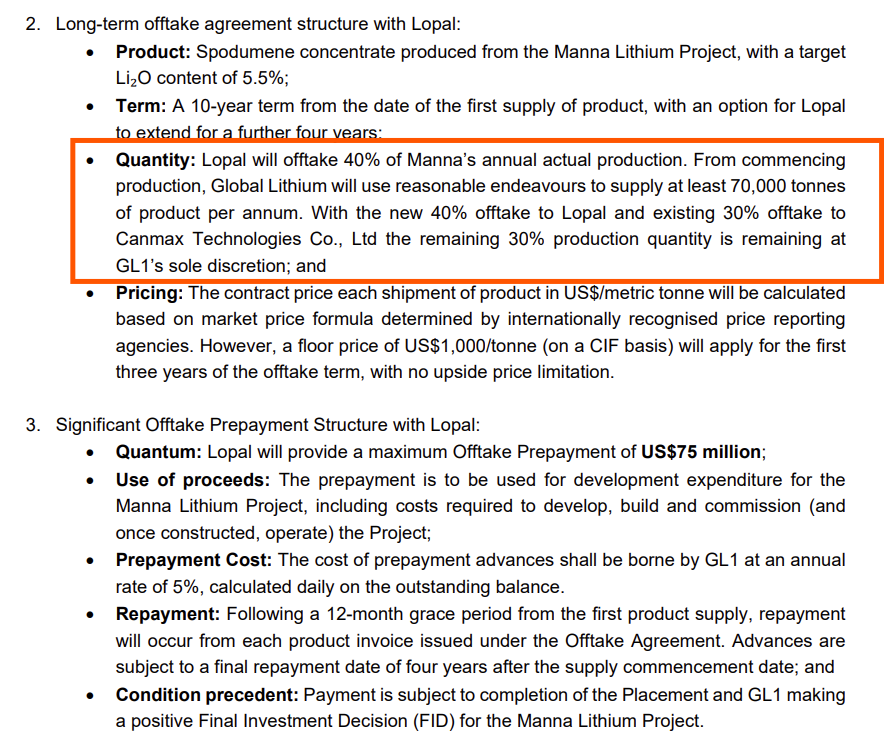

Give us 40% of your total yearly output of spod and we will pay for it now... You haven't started construction of your mine yet but that's ok.

Why doesn't Jiangsu Lopal Tech just source 70ktpa of SC5.5 from Manono North or from one of the many "mega" deposits recently found? Surely Zijin can spare a measly 70ktpa. Hmmm🤔

Floor price of US$1000 seems to be a common theme now.

Market tight. Bullish Aussie spod.

Only God is capable of knowing *exactly* what will happen 2,000 years in the future. The Bible is absolutely incredible. This is more proof.

What many Christians miss in Genesis 22 👇

🔥🚨BREAKING: A Mexican gold miner who was trapped 300 meters underground for two weeks has just been found alive. The rescue footage shows him standing in waist-deep water, telling rescuers he never lost faith during the ordeal.

$BNZ $BNZ.ax new discovery corridor confirmed with Hurricane trend emerging as Zone 126-style high-grade system over a 1,000m NE-plunging fold corridor. Two rigs now drilling.

⛏ 11m @ 6.4g/t within 102m @ 1.1g/t

⛏ 2m @ 19.1g/t

⛏ New "Lens 0" links Zone 126 & Zone 102

$BZ $BZ.v

Desecrating Easter was the first step toward nuclear war. Christians need to understand where Trump is taking us.

0:00 Monologue

43:23 Paula White’s Strange Easter Sunday Service

51:17 Who Really Is Paula White?

57:24 How Did Paula Become Trump’s Spiritual Advisor?

1:00:03 The Exposed Megachurch Documents

1:09:52 Why Is Corruption So Prevalent in American Protestant Churches?

1:13:10 The Scam That’s Taken Over the Nonprofit Industry

1:27:14 The Mormon Church’s Investments in Weapons Manufacturing

1:28:52 How Much Money Does Franklin Graham’s Nonprofit Have?

1:33:11 How Do Megachurch Pastors Justify Owning Private Jets?

1:39:30 Graham's Bizarre Alaskan Hideout

1:52:42 The Love of Money Is the Root of All Evil

1:54:27 What Is Dispensationalism?

2:07:15 The Attempts to Usher in the Antichrist

2:13:00 Finding Contentment and Fulfillment in Christ

2:16:36 The Spiritual War Happening in the White House

Canada just criminalized reading the Bible.

Now quoting Scripture on marriage, sin, or God’s design for sexuality can be prosecuted as “wilful promotion of hatred.”

This is how the West falls.

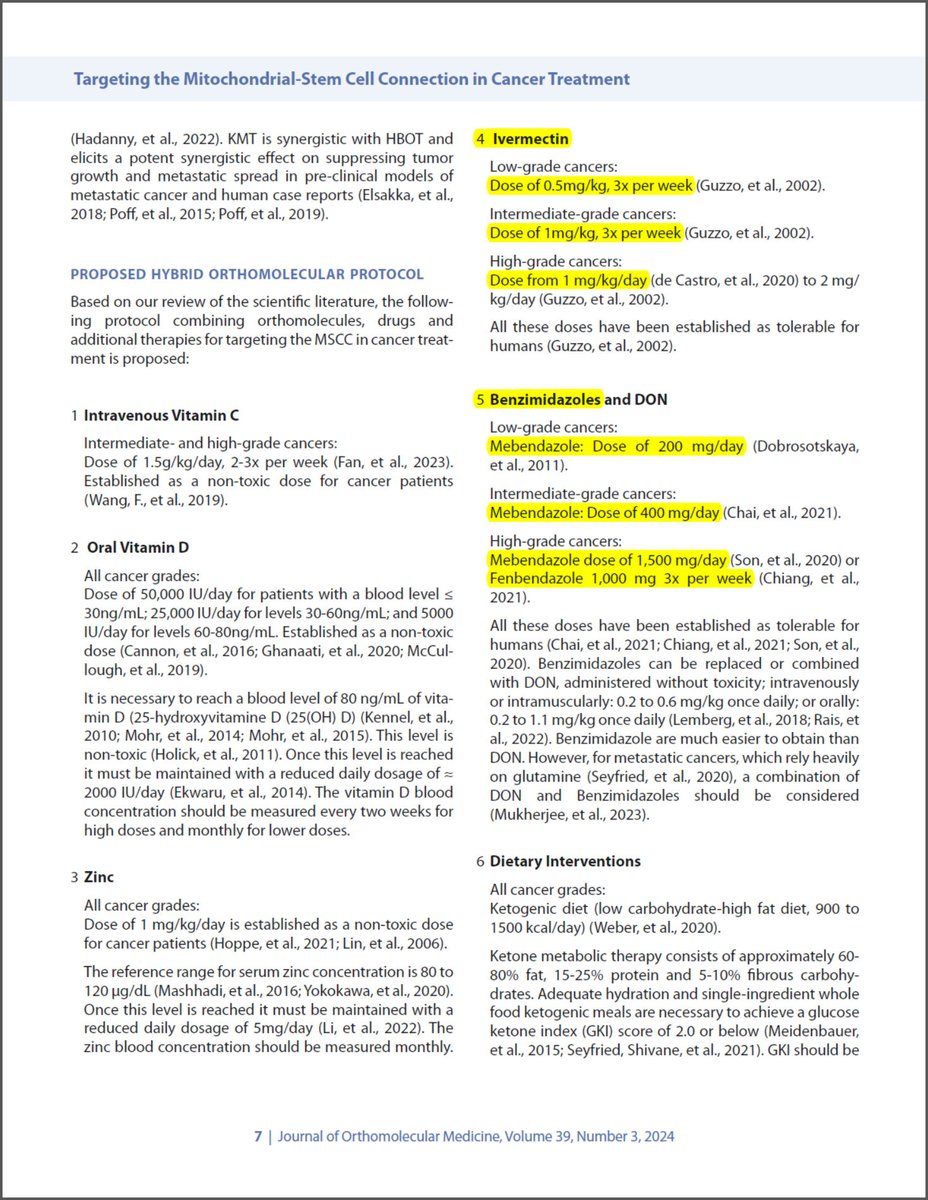

BREAKING NEWS: First-in-the-World IVERMECTIN, Mebendazole and Fenbendazole Protocol for CANCER has been peer-reviewed and published!

I am seeing our paper everywhere recently, the NEWS is spreading! 😃

BIG PHARMA attacked our Fenbendazole paper on three Stage 4 Cancer patients who are now Cancer Free, but it will be resubmitted and published soon!

I have been attacked recently by Canadian authorities for my revolutionary Cancer research and work, but...

a NEW FLORIDA CANCER CLINIC is coming soon!🙏

Thank you all for your ongoing support!! 😃

God Bless you all and God bless those who are fighting Cancer...