Read CEO Richard Zdunkewicz's PV Magazine article on the distributed energy value stack and what it takes to realize that value.

What is modeled is not necessarily what you get:

https://t.co/BbpMC5Xu0u

#DistributedEnergy#EnergyStorage#BatteryStorage#CommercialEnergy #CleanEnergy

#GridModernization spending is projected to exceed $1 trillion by 2040.

Increased investments by utilities increases costs to ratepayers and enhances the value of #DistributedEnergy.

Sources: @energy, @ieefa_institute

Visit https://t.co/ZkjeBFqjl2 for faster energy insights & better outcomes.

BTM battery capacity is growing 30% to 50% annually.

Storage adoption is accelerating as a proven tool to drive revenue, reduce costs, and manage risk.

Stay ahead with https://t.co/9WiDs9ZYm4

#CleanEnergy#BatteryStorage#DERs#GridModernization#EnergyStorage

Texas is paying for backup power that won't help the grid.

Texas recently funded a new program to keep hospitals, water systems, and other critical facilities running when the power goes out. It's a reasonable use of public money, but buried in the program rules is a restriction that undercuts the investment's broader value. The backup systems being funded aren't allowed to support the grid during normal operations. They can only function as emergency equipment. That's worth questioning.

The Texas Backup Power Package Program bars state-funded distributed generation and storage systems from participating in energy sales, ancillary services, emergency response programs, and demand response. The reasoning isn't hard to follow. Public funds are going toward site reliability, and officials want to make sure the equipment is available when a real emergency hits. That's a defensible position. The problem is that it treats "available for emergencies" and "useful only during emergencies" as the same thing, and they're not.

Texas is managing rising electricity demand, strained dispatchable resources, and growing transmission constraints all at once. Distributed generation and storage assets located across hospitals, campuses, and industrial sites are precisely the kind of flexible, local resources that could provide meaningful relief. Modern systems can be configured to maintain their emergency reserves while still contributing to grid stability during normal hours. The technology isn't experimental, the controls, protocols, and safeguards already exist.

Under the current rules, none of that is possible for program participants. The state ends up with publicly funded equipment that sits idle most of the year, generating no return for the owner and no benefit to the grid outside of actual outages.

Nobody is arguing that a hospital's backup generator should be tied up in a grid program when the lights go out across the city. Resilience has to come first, and that requirement can be written directly into the rules through mandatory reserve levels, islanding requirements, and operational safeguards. Within those guardrails, though, there's no good reason to prohibit owners from participating in grid support programs when their systems can safely do so. They'd earn a return on the investment, the grid would gain additional flexibility, and the public funds would stretch further.

Reliability and grid participation aren't in conflict. Texas just needs a policy framework that recognizes that.

#TexasGrid

#ERCOT

#TexasPower

#EnergyNews

Transmission & distribution costs now represent as much as 50% to 70% of C&I customer electricity bills. Focusing on comprehensive energy management strategy, including transmission & delivery costs, unlocks savings opportunities.

Unlock those savings now: https://t.co/ZkjeBFqjl2

#EnergySavings #CommercialRealEstate #EnergyStrategy

The Hidden Cost of Large Loads on the Electric System:

Electricity demand in the United States has entered a new reality. Over the past several decades, electric demand growth was relatively modest, gradual, and broadly distributed across customer classes Electricity demand in the United States has entered a new reality. Over the past several decades, electric demand growth was relatively modest, gradual, and broadly distributed across customer classes and regions. Utilities, grid operators, regulators, and large customers could plan around a system that changed incrementally. That pattern has shifted as a growing share of new demand comes from large, concentrated loads, particularly data centers.

At the national level, projected demand growth may still appear manageable. But the broad view does not tell the full story. The more important issue is where the new demand is appearing and how quickly local infrastructure can plan and take action. A new data center does not place equal pressure on the entire U.S. power system. It affects the specific utility territory, transmission zone, substation, or regional market where it connects – if it connects. When several large facilities cluster in the same area, they can create significant strain on local capacity, interconnection processes, grid planning, and wholesale market conditions.

That pressure can affect customers who have no direct connection to data centers. A manufacturer, hospital, university, distribution center, or large commercial facility may not be responsible for the new load, but if it operates in a constrained area, it may still be exposed to the consequences. Those consequences can appear in the form of higher energy costs, longer timelines for new service or expansion, tighter reserve margins, increased demand charge pressure, or greater price volatility during peak periods.

This is the practical meaning behind what some might describe as a “data center tax.” It is not a formal tax, and it won’t appear as a line item on a bill.

Rather, it is the potential cost of being located in a market where large new loads are growing faster than the grid can adapt. Transmission, substations, generation resources, and interconnection upgrades often require years of planning, permitting, regulatory approval, financing, and construction. When those timelines fall out of alignment with the presence of large loads on the system, the imbalance can ripple across the local grid.

For commercial and industrial customers, this changes how energy risk should be evaluated. The traditional question has been how much energy a facility consumes. While that still matters it is no longer enough. Large energy users also need to understand given their location how constrained their local grid may be, how their utility is planning for new load growth, what regulatory decisions may affect future costs, and whether they have options to improve flexibility before conditions become more expensive or restrictive.

In this environment, energy strategy becomes more local, more forward-looking, and more dependent on market-specific intelligence. Customers that understand these dynamics sooner rather than later will be better positioned to manage both cost and reliability risk. They can evaluate alternatives, consider distributed energy resources, assess operational flexibility, plan future expansion with better information, and avoid being surprised by changes that may already be developing in their local market.

DECH helps commercial and industrial customers evaluate this exposure by assessing local market conditions, utility planning, grid constraints, and energy cost risk. The goal is to give customers a clearer view of how regional changes may affect their facilities and what practical strategies may improve flexibility, reduce exposure, and support better long-term energy decisions.

The growth of data centers is not only a technology story. It is also an energy cost story, a grid planning story, and a local market risk story. For large energy users, the important question is not simply whether large load growth will impact the local grid and electric market. It is whether their business is prepared for how that growth may affect their cost and operational requirements.

Learn more at https://t.co/ZkjeBFqjl2

#EnergyMarkets #PowerDemand #AIInfrastructure

Wholesale price spikes have exceeded $1,000/MWh during peak demand events. Price volatility creates both risk and opportunity for dispatchable energy assets.

Learn how to capture more value and navigate market volatility at https://t.co/9WiDs9ZYm4

#Energy#DER#PowerMarkets

The economics of battery storage have changed considerably over the past decade, but what may be changing even more significantly is the way organizations are beginning to think about the role storage can play within their operations. As battery costs have continued to decline, storage is no longer viewed solely as a specialized technology reserved for a narrow set of customers with unusually high demand charges or resilience requirements. At installed commercial pricing levels that today commonly range between $300 and $600 per kilowatt-hour, batteries have become part of a much broader economic discussion around energy flexibility, operational efficiency, and long-term risk management.

Despite this shift, storage is still frequently evaluated using frameworks that were developed when systems were far more expensive and when the economic justification for deployment often depended on a single value stream. In many commercial and industrial settings, batteries continue to be analyzed primarily through the lens of peak shaving, where the objective is simply to reduce demand charges during periods of highest consumption. While that can certainly provide meaningful savings, it often understates the broader economic role storage is now capable of serving.

The value of battery storage increasingly comes from its ability to interact dynamically with the larger energy system rather than functioning as an isolated asset. A battery can reduce peak demand, but it can also provide flexibility in how and when electricity is consumed, help organizations respond to changing tariff structures, support onsite generation strategies, and improve operational continuity during periods of grid instability. As utilities continue moving toward pricing structures that place greater emphasis on timing, demand, and system conditions, the ability to manage energy consumption with greater precision becomes financially more important.

This broader approach increasingly focuses on the value stack, where the economics are driven by the combined effect of multiple operational and financial value streams working together. In the case of battery storage, those value streams may include demand charge reduction, energy arbitrage, resilience benefits, operational flexibility, coordination with onsite generation, and the ability to respond to evolving utility pricing structures. As storage costs decline, the ability to stack and optimize these benefits is becoming central to how projects are evaluated.

That evolution is beginning to expand the addressable market for storage. Organizations that may not have viewed batteries as economically viable several years ago are now finding that the economics improve substantially when multiple operational and financial benefits are evaluated together rather than individually. In practice, the financial performance of storage is often shaped by the interaction between load profiles, utility tariffs, operational schedules, distributed generation assets, and an organization’s tolerance for energy price volatility or outage risk. Looking at any one of these factors in isolation can produce an incomplete assessment of value.

For that reason, storage analysis is becoming less about evaluating a standalone technology purchase and more about understanding how flexibility can be integrated into the broader operation of a facility or portfolio. The organizations that appear to be deriving the greatest value from storage are often those that approach it as part of a coordinated energy strategy rather than as a single-purpose investment.

Distributed Energy Clearinghouse supports this type of analysis by modeling and optimizing multiple value streams simultaneously, helping organizations evaluate how storage interacts with the broader energy system and where operational flexibility can translate into measurable financial returns.

Get a demo: https://t.co/qTXFwvjegU

#EnergyStorage

#EnergyEconomics

#GridModernization

#OperationalEfficiency

#DECH

#Demandcharges can represent 30 to 70% of monthly consumer & industrial bills. Reducing #peakdemand can unlock significant and sustainable cost savings.

Find out more at https://t.co/9WiDs9ZYm4

#CleanEnergy

Battery storage technology has improved. Are your investment assumptions keeping up?

Battery technology has improved steadily over time, but the implications of those improvements are not always reflected in how projects are evaluated. Lithium-ion systems now operate at round-trip efficiency levels that frequently exceed 85 percent and can approach or surpass 90 percent under certain conditions. At the same time, cycle life has expanded significantly, often reaching several thousand cycles before meaningful degradation occurs.

Individually, these improvements may appear incremental, but together they reshape the financial profile of storage investments. Higher efficiency reduces energy losses during operation, while longer lifespans improve predictability and reduce the frequency of replacement. These factors directly influence long-term returns, particularly in applications where batteries are cycled regularly.

Despite this, many models still rely on assumptions that were reasonable several years ago but are increasingly outdated today. This can lead to conservative evaluations that undervalue storage, or system designs that are larger and more costly than necessary.

What we have observed is not a lack of interest in storage, but rather a lag in updating the inputs used to assess it. As the technology continues to improve, the margin for error in modeling becomes smaller, and the impact of those assumptions becomes more pronounced. In a landscape where pricing is more dynamic and demand-driven costs are more significant, accurate inputs are even more critical to making sound investment decisions.

Keeping models aligned with current performance is essential, especially as margins tighten and projects become more sensitive to even the smallest contributors of value. DECH enables energy management and investment teams to use our platform, which contains current data to evaluate scenarios with greater precision, reducing the risk of underestimating viable opportunities or overinvesting in unnecessary capacity.

#EnergyStorage #Batteries #CleanEnergy #EnergyMarkets #Renewables

ESCALATING PRICES (C&I)

Electricity prices for C&I customers increased ~20–40% since 2020.

Higher prices increase the value of demand management, on-site generation, and smarter procurement.

Source: @EIAgov

For faster energy insights, smarter investments, and better outcomes, visit:

https://t.co/mx5BjykLHL

#Energy #EnergyPrices #CleanEnergy #EnergyTech

The value of solar is limited. The value of solar and storage is being rewarded now.

The value of solar is no longer defined by electricity production alone. In markets like Massachusetts, it is increasingly defined by how and when that energy is used, and this is where battery storage materially changes the equation.

Massachusetts’ Clean Peak Standard is a strong example of how policy is reshaping distributed energy economics. The program rewards systems that deliver energy during specific seasonal peak windows, periods when the grid is under the most strain and energy is most valuable. The key value drivers are not just generation, but timing, consistency, and the ability to respond to those defined peak intervals. These windows vary by season and are not always intuitive, which makes the revenue opportunity difficult to estimate without detailed modeling.

Standalone solar can participate, but only to the extent that its natural production profile aligns with those peak periods. Often, it does not. Battery storage allows excess solar generation to be captured and discharged precisely during Clean Peak hours, converting what would have been lower value energy into premium compensated output. At the same time, storage can reduce facility demand charges by managing load during coincident peaks, creating a dual benefit that solar alone cannot achieve.

The result is not just incremental improvement, but a fundamentally different value profile. Solar produces energy, while storage enables control, and together they unlock access to programmatic revenues and tariff savings that neither can fully capture on their own.

The challenge is that programs like Clean Peak are complex. The rules, seasonal variations, and performance requirements introduce layers of nuance that are often oversimplified in project proposals. In many cases, the underlying value drivers are not modeled with enough precision, leading to overstated or understated outcomes.

This is where DECH provides a distinct advantage. DECH models the full complexity of these markets, including wholesale power prices, tariff structures, incentive mechanics, and hourly electricity demand, to deliver an objective, grounded view of a project’s true value potential, so organizations can make decisions based on what the distributed energy asset is can realistically earn, without errors like double-dipping or overly aggressive battery cycling.

#DER

#SolarPlusStorage

#EnergyTransition

#MAenergy

Peak demand growth in key regions forecasted at 2x historical averages.

Rising demand creates strong opportunities for load optimization and behind-the-meter solutions.

https://t.co/9WiDs9ZYm4

#Energy#Grid#DER#CleanEnergy

You’re paying for a $1 Trillion grid upgrade. What value are you getting?

Over the past decade, one of the most consequential shifts in retail energy has had little to do with how power is generated, and everything to do with how it is delivered and at what cost. Utilities across the United States are preparing for more than $1 trillion in grid modernization investments through 2040, driven by aging infrastructure, reliability requirements, and the increasing complexity of a more distributed grid. While this investment is necessary, it is important to recognize where those costs ultimately land, which is on the customer.

Transmission and distribution, or T&D, has quietly become the dominant component of many commercial and industrial electricity bills. In several markets, it already represents the majority of total delivered costs, and it continues to grow at a rate that significantly outpaces the cost of generation. This fundamentally changes how energy strategy should be approached.

For years, organizations focused heavily on procurement, using price management-enabled structures, negotiating supply rates and optimizing for imbedded risks. That approach made sense when generation costs drove most of the economics. Today, it addresses a smaller portion of the total electricity bill. What matters increasingly is what drives electricity demand, how it fluctuates, and how it can be managed to create value.

We often see companies make smart procurement decisions, or invest in renewable generation, only to find that those gains are offset by unmanaged demand peaks and rising delivery charges. The opportunity now lies in managing usage and demand, not just sourcing energy more cheaply, and that shift is where meaningful cost control is taking a higher profile.

What this means in practice is that organizations need to move beyond energy procurement strategies that don’t consider operational realities and start actively managing how their operations and associated electricity usage can be more dynamically managed. That requires visibility into when costs are actually incurred and how operational processes drive them. DECH helps translate complex rate structures and load behavior into clear financial insights, so teams can identify where delivery costs are being created and take targeted action to reduce them.

#Energy #GridModernization #EnergyTransition #Manufacturing

#Electrification may increase U.S. load by 20 to 40% by 2040, including the load increase of 12 - 14% from #DataCenter usage.

As the grid evolves, data-driven strategy is the competitive edge.

Faster #energy insights. Smarter investments. Better outcomes:🔗 https://t.co/ZkjeBFqjl2

Sources: @ENERGY, #NREL

#Datacenters may reach ~8–10% of U.S. load by 2030 representing highly concentrated demand.

Interconnection is now a binding constraint; onsite power is strategic. 🔋 #BTM#Energy

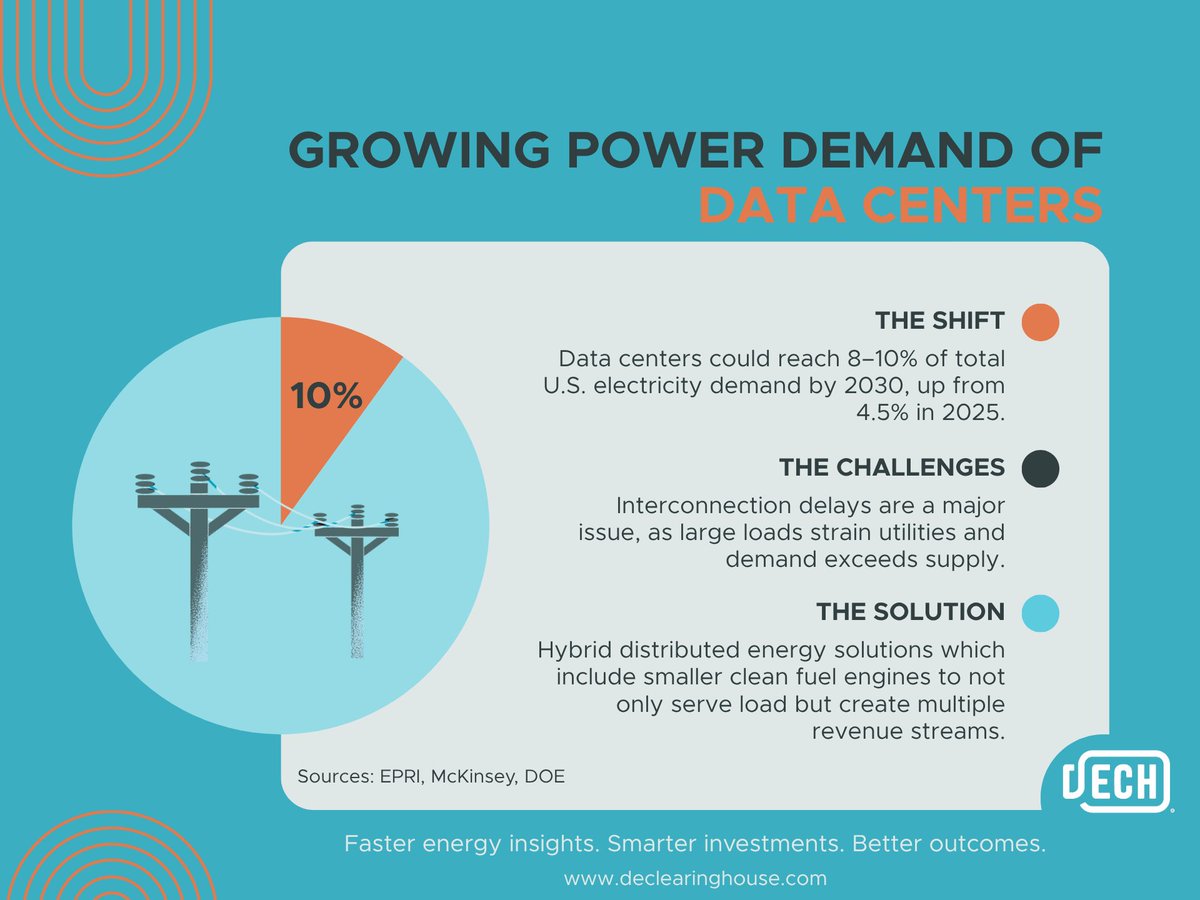

Growing Power Demand of #DataCenters

The Shift:

Data centers could reach 8–10% of total U.S. electricity demand by 2030, up from 4.5% in 2025.

The Challenges:

Interconnection delays are a major issue, as large loads strain utilities and demand exceeds supply.

The Solution:

Hybrid #DistributedEnergy solutions which include smaller clean fuel #engines to not only serve load but create multiple revenue streams.

#Energy #NetZero #Tech #PowerGrid

Sources: EPRI, McKinsey, DOE