The State of RWAFi Q1 2026 Report is here.

Developed in collaboration with @DefiLlama, this report breaks down tokenised commodities, equities, real estate & alternative finance. Same macro trend, yet evolving differently under unique constraints.

https://t.co/arOeCRFwuz

Japan's regulatory clarity is becoming a competitive advantage in enterprise blockchain.

@StartaleGroup CEO @WatanabeSota sat down with us to discuss vertical integration, the JPYSC and USDSC stablecoin pair, and building compliant onchain infrastructure:

https://t.co/Qbg6h8ni9E

The @pharos_network built an ocean. @circle made sure it had somewhere to flow.

We spoke with @wishlonger, @michellek_web3, and Spencer Jaffe at EthCC about the compliance rails, institutional throughput, and settlement infra RealFi needs to scale:

https://t.co/gWYML45BuZ

Join the DLR analysts next Monday as they dive into topics straight from the State of RWAfi Q1 2026 report:

→ Is RWAfi one market or many?

→ The rapid growth of tokenised stocks

→ What's happening in private credit

→ Permissioned vs permissionless RWA

See you then!

Thank you to our first donor! $500 in USDC has been contributed.

We're excited to make @ethereum more secure for everyone. Shout out to @Giveth@ethereumfndn for making this possible!

We went deep on this across four asset classes, looking at what's being used, how it's being used, and what's still in the way.

Everything you need to know is in The State of RWAfi Q1 2026:

https://t.co/qWcB4tozNp

What's the current state of RWAfi? tokenised ≠ used.

Nearly $30 billion dollars. That's the amount of real-world assets tokenised onchain. Yet only $1.9 billion is being put to work.

So where's the disconnect? This is one of the topics we explored in our latest report with @DefiLlama:

🧵

Looking at utilisation alone misses something. For instance, tokenised gold should behave like gold; most holders want exposure, not yield. The low utilisation reflects the asset, not a failure of the market.

The State of RWAfi report points to three blockers keeping assets idle:

1) Tokens represent claims through legal wrappers and not direct ownership, which limits how freely they can move into DeFi.

2) Liquidity is fragmented across issuers, chains, and venues, making it harder for lending protocols to integrate them.

3) Regulation varies by jurisdiction, so what you can do with an asset onchain depends heavily on where you are.

The assets that have cracked it so far (private credit, gold) share one thing: their economic function maps naturally onto DeFi use cases like collateral and yield.

The ones still sitting idle mostly haven't found that fit yet.

The State of RWAFi Q1 2026 Report is here.

Developed in collaboration with @DefiLlama, this report breaks down tokenised commodities, equities, real estate & alternative finance. Same macro trend, yet evolving differently under unique constraints.

https://t.co/arOeCRFwuz

95% of EU crypto derivatives volume was offshore. Until now.

After @okx announced MiCA-regulated X-Perps at @ParisBlockWeek, we spoke to OKX Europe CEO @EraldOnChain about bringing perps volume back onshore and the future of regulated trading in the EU.

https://t.co/09PZxvZLEj

Featuring @OndoFinance@xStocksFi@binance@SentoraHQ@redstone_defi

Stay tuned for an upcoming X space where we'll unpack it all together.

Until then, let us know what asset class you are most bullish (and bearish) on in the comments.

https://t.co/arOeCRFwuz

The State of RWAFi Q1 2026 Report is here.

Developed in collaboration with @DefiLlama, this report breaks down tokenised commodities, equities, real estate & alternative finance. Same macro trend, yet evolving differently under unique constraints.

https://t.co/arOeCRFwuz

A few things the data made hard to ignore:

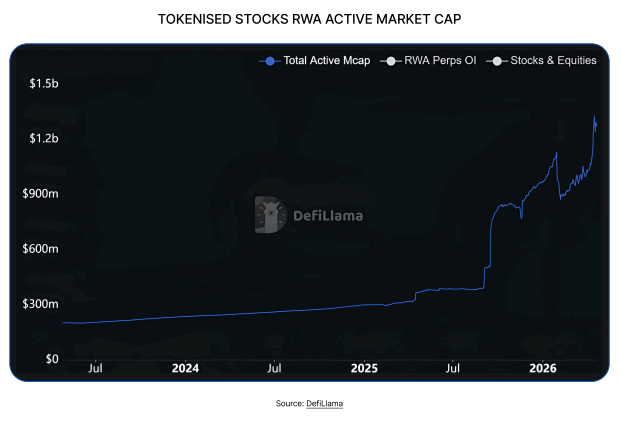

→Tokenised stocks scaled from $200M to $1.2B, but the market hasn't converged on which model wins. Synthetic, custody-backed, natively issued; each works differently onchain.

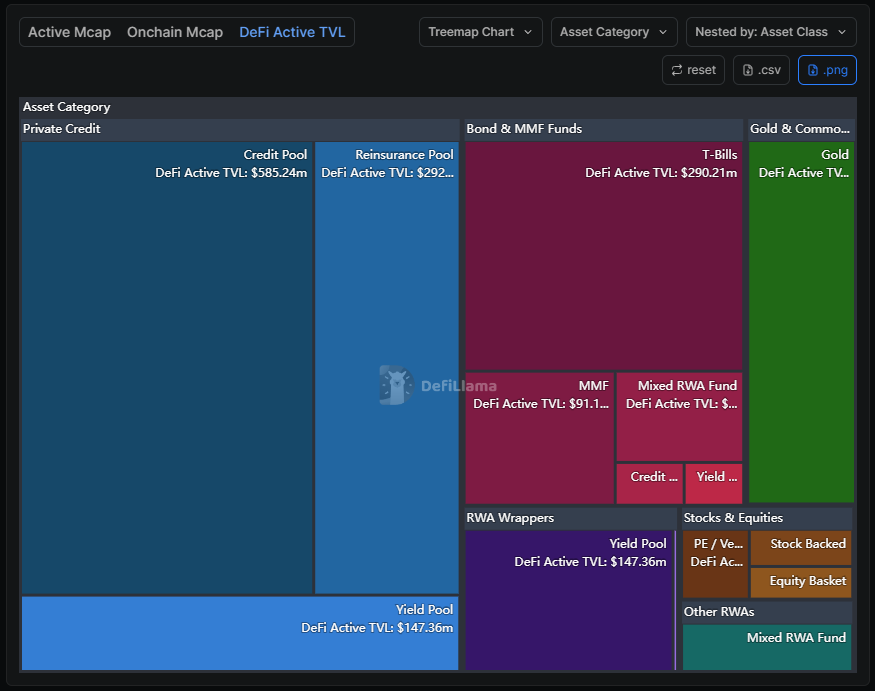

→ Private credit went from $49M to $4.57B in a year. The TradFi-to-DeFi pipeline is here, and it runs through credit.

→ The gold surge quickly propelled the world's oldest store of value into one of the most interesting DeFi assets. Collateral, perps, yield; it does it all now.

→ Real estate's slow growth is not a tech problem. Every jurisdiction has its own rules, its own registries, its own idea of what ownership means. That means bottlenecks.

Some of these assets are ready for DeFi. Some are not even close. The data makes it pretty clear which is which.