When traders say “Price is engineered!”, what they really mean is that price is deterministic.

But what exactly does that mean?

Well, in this study, I attempt to explain and potentially prove exactly that:

Does a hidden order lie within market dynamics? More importantly, how can this order be exploited, if it were to exist?

What can such a framework provide for risk aversion and forecasting early-warning signals for flash crashes, black swan events, and unusual phenomena?

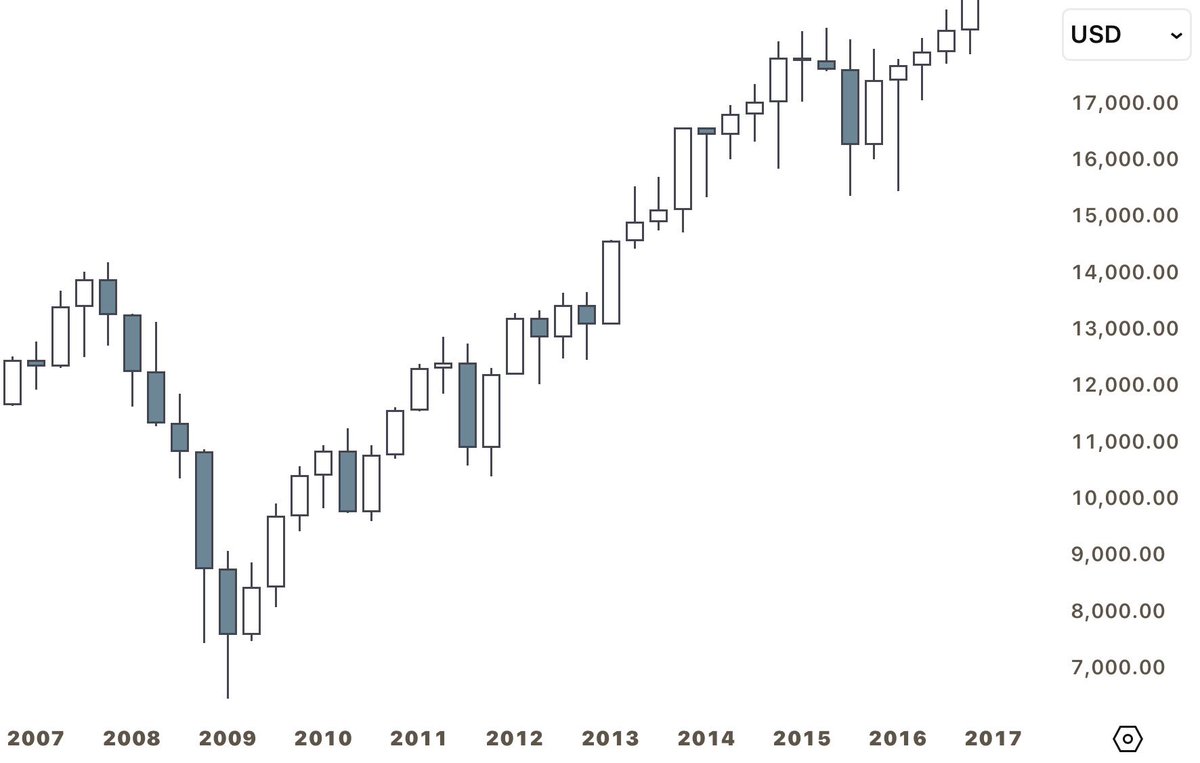

Lastly, as the final conclusion to our proof of concept, I show that a range in a market can be split into sections, in which the attractors of those periods can mechanically quantify the “state” of the market, where:

- Limit cycle attractors state price is “oscillating” in a periodic manner (I.E. Consolidations)

- Torus attractors are quasi-periodic and tell us when prices are oscillating in a quasi periodic manner (I.E. Converging triangles)

- Fractal attractors are dissipative in nature and tell us when prices are undergoing s tipping point (the system is about to change) (I.E. Manipulation)

- Strange attractors are chaotic in nature and tell us when price is expanding towards a newly perceived market value

One can quantify the transition between one state and another by analyzing the rate and impact of perturbations on the system, which is what leads to tipping points and is what classifies a liquidity injection

When traders say “Price is engineered!”, what they really mean is that price is deterministic.

But what exactly does that mean?

Well, in this study, I attempt to explain and potentially prove exactly that:

Does a hidden order lie within market dynamics? More importantly, how can this order be exploited, if it were to exist?

What can such a framework provide for risk aversion and forecasting early-warning signals for flash crashes, black swan events, and unusual phenomena?

Next up, I’m actively engaging in the same complex systems research in three markets simultaneously:

- Cryptocurrency (Open ledger, On-Chain Orderbook Analysis)

- Tick Data (Historical, Local, L3 Orderbook Data across 15+ exchanges, Quote + NBBO Feeds)

- Options Data (@unusual_whales options chain, 7-Day historical orderbook through API)

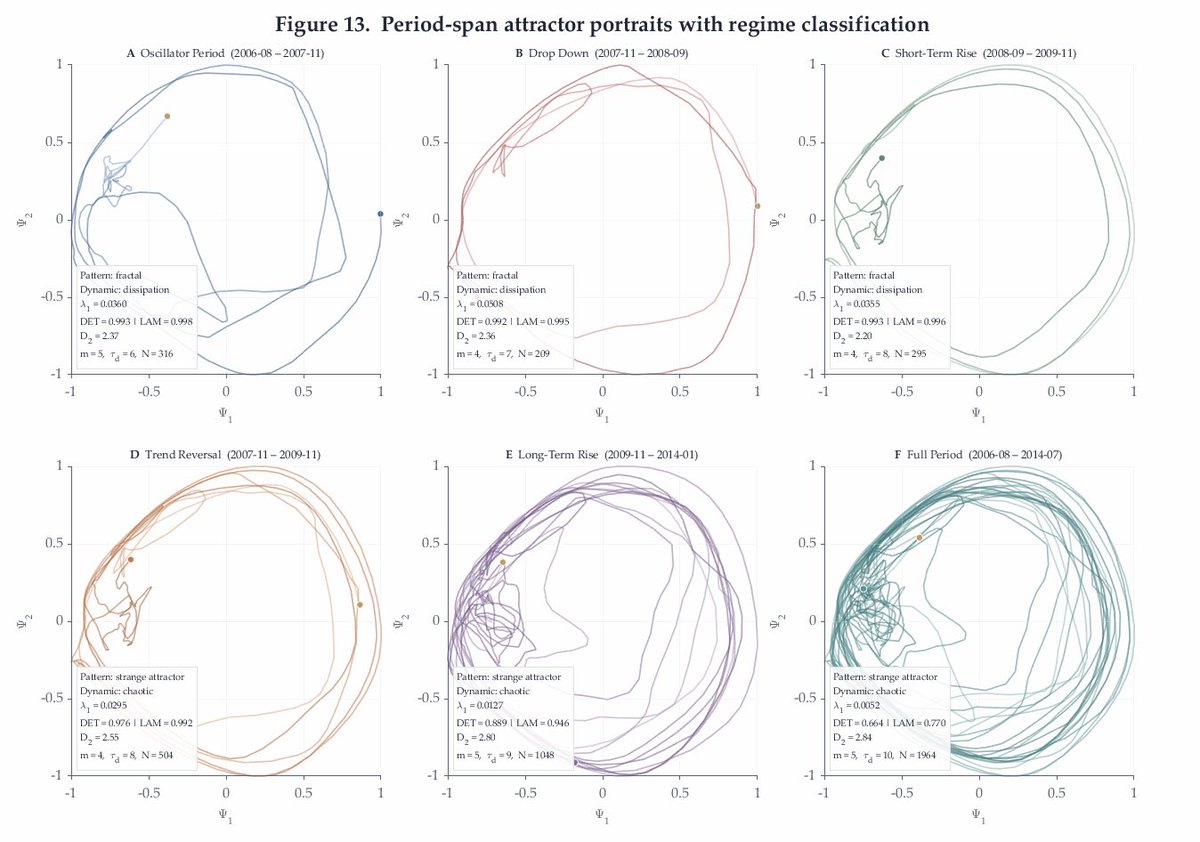

I predict that participation rates and perceived value across all markets lie on an attractor embedded within an n-dimensional Euclidean space, in which information dynamics across a society emerges as globally chaotic but locally deterministic, and thus, orderly at finite scales

Given a preconditioned environment in which fair-market value has shifted (a growing spring constant) while volatility has simultaneously been under-damped (a decaying damping coefficient) through liquidity provision, it can be predicted that a set of surgically placed orders (exploratory trading) can act as perturbations, leading to a dislocation and a forced cascade (I.E. Tipping point), forcing market makers to over-dampen volatility and secure a newly perceived fair-market value

Thus, I predict that leading up to a trajectory, a dissipative and fractal attractor is the fingerprint of this forced transition

Next up, I’m actively engaging in the same complex systems research in three markets simultaneously:

- Cryptocurrency (Open ledger, On-Chain Orderbook Analysis)

- Tick Data (Historical, Local, L3 Orderbook Data across 15+ exchanges, Quote + NBBO Feeds)

- Options Data (@unusual_whales options chain, 7-Day historical orderbook through API)

I predict that participation rates and perceived value across all markets lie on an attractor embedded within an n-dimensional Euclidean space, in which information dynamics across a society emerges as globally chaotic but locally deterministic, and thus, orderly at finite scales

Given a preconditioned environment in which fair-market value has shifted (a growing spring constant) while volatility has simultaneously been under-damped (a decaying damping coefficient) through liquidity provision, it can be predicted that a set of surgically placed orders (exploratory trading) can act as perturbations, leading to a dislocation and a forced cascade (I.E. Tipping point), forcing market makers to over-dampen volatility and secure a newly perceived fair-market value

Thus, I predict that leading up to a trajectory, a dissipative and fractal attractor is the fingerprint of this forced transition

When traders say “Price is engineered!”, what they really mean is that price is deterministic.

But what exactly does that mean?

Well, in this study, I attempt to explain and potentially prove exactly that:

Does a hidden order lie within market dynamics? More importantly, how can this order be exploited, if it were to exist?

What can such a framework provide for risk aversion and forecasting early-warning signals for flash crashes, black swan events, and unusual phenomena?

Proposed Risk-Aversion Research through Symbolic Dynamics:

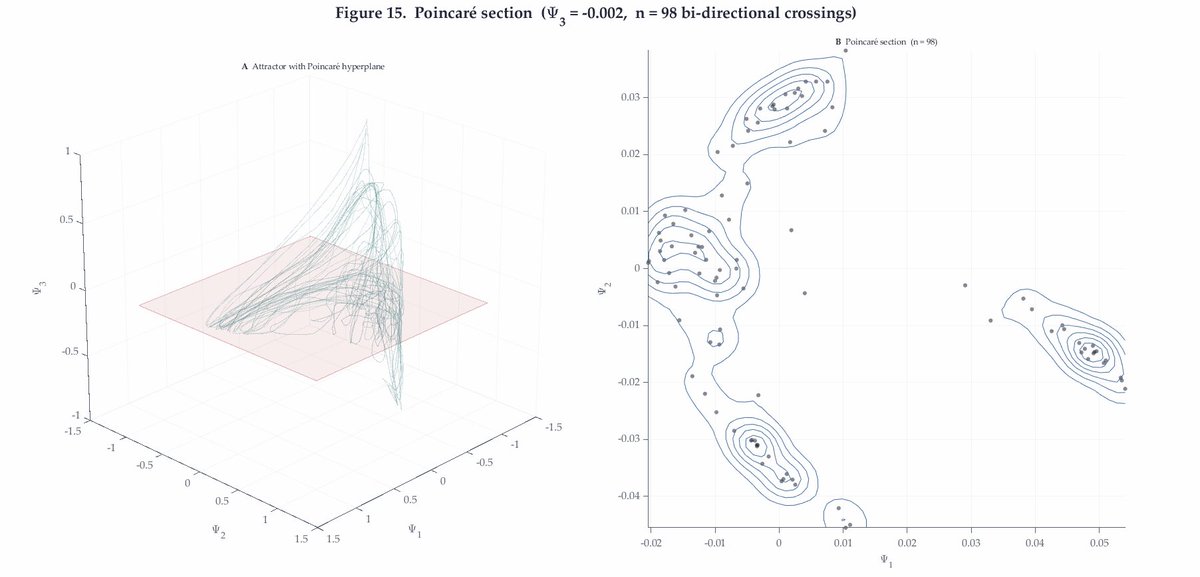

1. Use the Poincaré section clusters (Figure 14) as seeds for a Markov partition of the attractor into symbolically labeled basins

2. Map the trajectory through the partition to produce a discrete symbolic time series encoding qualitative regime transitions

3. Compute the information flow between the symbolic series and future returns at multiple horizon

4. Use the local Lyapunov exponent as a position-sizing multiplier, giving tighter stops and smaller positions in high-divergence regions (crisis) and larger positions in low-divergence regions (trend)

5. Construct an agent-based model and verify that the observed attractor geometry and regime transitions emerge from heterogeneous agent interaction

When traders say “Price is engineered!”, what they really mean is that price is deterministic.

But what exactly does that mean?

Well, in this study, I attempt to explain and potentially prove exactly that:

Does a hidden order lie within market dynamics? More importantly, how can this order be exploited, if it were to exist?

What can such a framework provide for risk aversion and forecasting early-warning signals for flash crashes, black swan events, and unusual phenomena?

Lastly, as the final conclusion to our proof of concept, I show that a range in a market can be split into sections, in which the attractors of those periods can mechanically quantify the “state” of the market, where:

- Limit cycle attractors state price is “oscillating” in a periodic manner (I.E. Consolidations)

- Torus attractors are quasi-periodic and tell us when prices are oscillating in a quasi periodic manner (I.E. Converging triangles)

- Fractal attractors are dissipative in nature and tell us when prices are undergoing s tipping point (the system is about to change) (I.E. Manipulation)

- Strange attractors are chaotic in nature and tell us when price is expanding towards a newly perceived market value

One can quantify the transition between one state and another by analyzing the rate and impact of perturbations on the system, which is what leads to tipping points and is what classifies a liquidity injection

Two final tests are the analysis of the Poincaré section and the Determinism Test; Both tests pass, with Poincaré showing a closed system snd many intersecting points, and the Determinism test proving that our denoised and nonlinear series has preserved its deterministic properties