@DsrPrivate Thanks Andy, appreciate you. It is this humility and systematic self-reflection that makes DS a compelling voice (and source of alpha) on this site.

Democracy is no longer a system of shared responsibility—it has become a sophisticated vote-buying machine, sustained by unchecked deficit spending. The costs are deferred through inflation, currency debasement, and the slow erosion of social cohesion.

The political, social, and economic fractures increasingly fall along generational lines: the old secure entitlements; the young inherit debt, asset inflation, and stagnating opportunity. This dynamic is unsustainable.

Possible endgames include fiscal discipline imposed by bond vigilantes, forced austerity in the wake of large-scale conflict, or a collapse into authoritarian control as institutions fail to adapt

Why is anybody surprised?

“Make America great again” policies are geared towards relocation of production inside USA. Of course there is going to be a demand for labour if local production increases. The risk is not a meltdown of the labour market, it is a melt up in long-term borrowing rates and inflation depending on the exact path of monetary and fiscal policy implementation.

If the equity market was to weaken, causes would be phase shift in the discount rate b/c where long term rates land. And margin compression which should follow increased bargaining power by labour and a higher cost of capital.

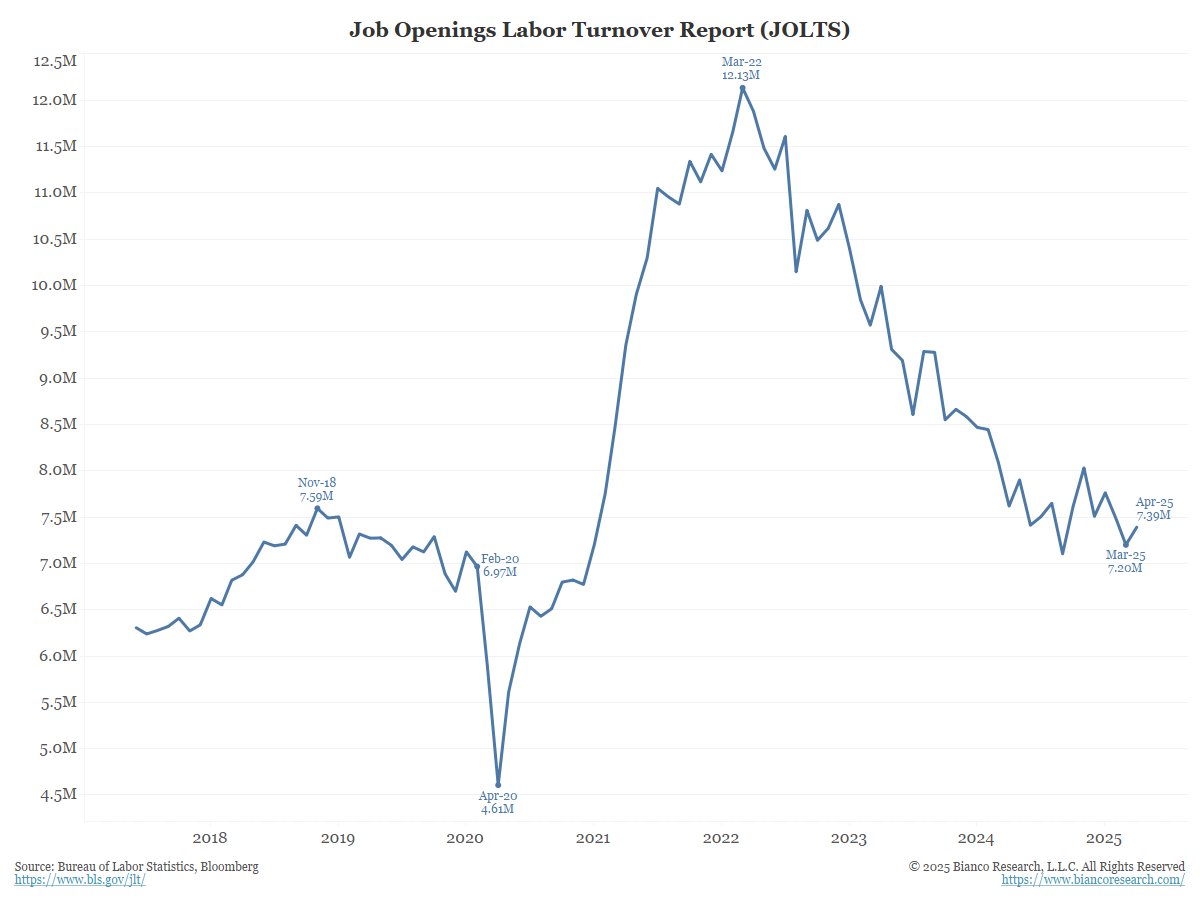

How did everyone get it so wrong?

This morning, the April Job Opening Labor Turnover (JOLTS) report was released.

The headline number:

*US APRIL JOB OPENINGS 7.391M; EST. 7.100M

---

The number of open jobs in the country INCREASED in April!

The same month that the collapsing "soft" (survey) data was supposed to be a leading indicator of a recession (Polymarket gave a 65% probability of recession), rising unemployment was also on the horizon. Combine that with the Liberation Day reaction in the stock market (-20%), and "bad stuff" was all but guaranteed.

Instead, companies were too busy filling out help-wanted advertising to get around to firing anyone in April. To repeat for emphasis, the stock market fell 20% in April, and companies responded by INCREASING the number of open jobs they were looking to fill.

Data looks fine at the moment, but seeds are sewn for the second wave.

Our domestic AUD retail operation has in the past 60 days seen packaging supplier hike prices by 25%, chocolate supplier prices by 50% and accounting firm raised fees after prevaricating for two years; they say “we’ve waited as long as we can to pass on our costs, but we have never been as unprofitable as we are now“

What is happening under the hood? During the first inflation wave, economic agents who had pricing power exercised it, and indexed their prices to inflation (maybe gouged a little).

Second wave is about price-taker agents scrambling to get a slice of the spending power being released back into the economy via rate cuts.

Cost push inflation is a bitch.

Economy is 100% soft but costs are hard. And slowdown is not going to ease the costs pressures.

@BergMilton SPX experienced upside gaps 23 April, 1 May & 12 May — given you interpreted upside gaps as a bearish signal before the recent correction, can you please help me understand why you don’t weight these gaps as a bearish signal now?

Risk markets are marching in lock-step to the upside while the safety duo marches in lock-step the other way. That’s bullish today but concentration risk is high; one macro jolt can flip both clusters in unison. Keep an eye on BTC and yields as early warning lights.

It’s a two-bucket world 🧵

- Risk assets (equities, oil, copper, crypto, dollar) are tightly positively correlated.

- Safe-havens (long bonds, gold) are tightly negatively correlated.

That’s a textbook “risk-on vs safety” split, just exaggerated to extremes.

Actionables to track over the next week

#1 Bond/Gold correlation to each other

If it breaks positive, safety trade fragmenting

Could precede wider cross-asset volatility

#2 BTC vs ES correlation

First mover on liquidity turns

Decoupling would flag liquidity tightening

#3 DXY vs ES

Rare positive link—fragile

A single dovish data print can snap it