Potential BoJ intervention (selling USD/buying JPY) to defend the 160 level could trigger a sharp yen rally.

This risks unwinding yen carry trades — cheap JPY borrowed to fund US/global equity positions — leading to forced selling and short-term volatility, as seen in the 2024 episodes and April 2026 moves.

Japanese exporters face headwinds from stronger yen; broader equities could see risk-off pressure and corrections, especially momentum stocks.

More near-term turbulence than structural bearish signal — depends on intervention scale and macro backdrop. Watch yen action closely.

BREAKING: 🚨🇮🇱🇮🇷 Archaeologists in the Holy Land just uncovered a 3,000-year-old Israelite tablet…

It reads: “Iran is 12 days away from developing a nuclear weapon.”

Some may feel I’m dwelling on this, but I am concerned for the health of the UK economy.

The yield on the 10-year gilt has climbed 12 basis points today (see the CNBC chart below), decoupling from both oil prices and yields in other advanced economies—both of which are currently lower.

Meanwhile, the 30-year yield has just hit a 28-year high.

#economy #markets #gilts #uk

MICHAEL BURRY HAD DROPPED A CHILLING WARNING:

“THE MOMENT YOUR INTEREST PAYMENTS EXCEED TAX REVENUE, YOUR COUNTRY OFFICIALLY BECOMES A PONZI SCHEME.” 👀

WHEN DEBT SERVICES ITSELF…

WHEN INTEREST OUTPACES INCOME…

THE SYSTEM STARTS EATING ITSELF.

THIS ISN’T THEORY.

THIS IS MATH.

AND THE CLOCK IS TICKING.

A UK home cost £19,273 in 1980.

The same home today? £301,151.

The house didn't get better. Your money got worse.

A generation priced out. Quietly accepted as normal.

Rory Sutherland made a quietly devastating observation about one of the biggest societal shifts of the last 50 years.

He said the move to the double-income household started as an option but quickly became an obligation. The big winners? Governments (twice as many people to tax) and property owners (now two salaries were needed to buy a house). The big loser? The family itself, which lost roughly 35 hours of discretionary leisure time per week — with no real increase in living standards, because the extra money was largely soaked up by higher house prices and taxes.

It’s a classic example of how something that begins as liberation can quietly turn into a new form of constraint.

Longitudinal studies on happiness and time use (including data from the American Time Use Survey and OECD reports) show that the sharp rise in dual-earner households correlated with stagnant or declining leisure time for families, while subjective well-being metrics for parents have not risen in line with the additional income — supporting the idea that much of the gain was captured by housing costs and taxation rather than improved quality of life.

It’s a reminder to look carefully at changes that society presents as inevitable progress.

What do you think — has the double-income model delivered more freedom or more pressure for most families?

THE RECKONING

Wall Street’s oldest warning system just triggered.

The Shiller PE ratio crossed 40.16 this week.

In 154 years of recorded market history, this threshold has been breached only three times. The first was December 1999. The second was November 2021. The third is now.

What followed the first: a 49% collapse.

What followed the second: a 25% drawdown within ten months.

What follows the third: you are living it.

Consider what 40 means. The market now trades at 2.3 times its 154 year average valuation. Stocks have been cheaper than today 98.9% of all recorded history. The only comparable moments preceded the two most devastating corrections of the modern era.

The mathematics are unforgiving. Vanguard’s century long analysis confirms a 0.43 correlation between current CAPE and decade forward returns. At 40, the implied annual real return through 2035 falls to 1.6%. Not negative. Not catastrophic. Simply… exhausted.

But here is what the headlines miss: CAPE does not predict crashes. It predicts gravity. The difference between a 49% collapse in 2000 and a 25% correction in 2022 was not valuation. It was the catalyst.

The catalyst today remains unknown. Trade policy. Credit contraction. Earnings disappointment. Geopolitical rupture. Any spark finds abundant fuel.

What this means for you: Recalibrate expectations. A decade of 10% returns is mathematically improbable from current levels. Diversification is not caution. It is arithmetic.

The market is not broken. It is priced for perfection in an imperfect world.

History does not repeat. But it rhymes in numbers that do not lie.

The clock at 40 has started.

JAPAN JUST BROKE THE GLOBAL FINANCIAL SYSTEM AND YOU HAVE 30 DAYS

November 18th, 2025. Japan’s 20-year bond yield hit 2.75%. Highest in recorded history. This single number just ended the 30-year era that made your retirement possible.

The math is simple and fatal.

Japan has 263% debt to GDP. $10.2 trillion total. They survived because rates were zero. At 2.75%, debt service explodes from $162 billion to $280 billion over ten years. That’s 38% of total government revenue consumed by interest alone.

No nation in history has sustained this without default or hyperinflation.

But here’s what kills your portfolio first.

Japan holds $3.2 trillion in foreign assets. $1.13 trillion in US Treasuries alone. They bought everything foreign because Japanese bonds paid nothing. Now Japanese bonds pay 2.75%.

After hedging costs, holding US Treasuries loses money for Japanese investors. Repatriation is not optional. It’s mathematical necessity. $500 billion exits global markets in 18 months.

The yen carry trade holds $1.2 trillion in borrowed yen funding global assets. Stocks. Crypto. Emerging markets. Everything. As Japanese rates rise and the yen strengthens, every position goes underwater. Forced liquidation has already begun.

Three certainties nobody can deny.

The rate gap between US and Japanese bonds collapsed from 3.5% to 2.4% in six months. When it hits 2%, Japanese money floods home. US borrowing costs spike 30 to 50 basis points regardless of Fed policy.

December 18th the Bank of Japan meets. 50% probability they hike again. If they do, the yen surges. Every carry trade loses another 6% instantly. Margin calls cascade globally.

Japan cannot print money to escape. Inflation already exceeds target. More printing collapses the yen and imports inflation. They’re trapped between currency crisis and debt crisis.

The anchor holding global rates down for 30 years just broke. Every portfolio built since 1995 assumed Japanese yields stayed near zero forever. That assumption died today.

Position for chaos or become collateral damage. There is no middle ground.

Full Deep Dive Article - https://t.co/J14xVslTlR

Subscribe for daily premium data driven newsletter.

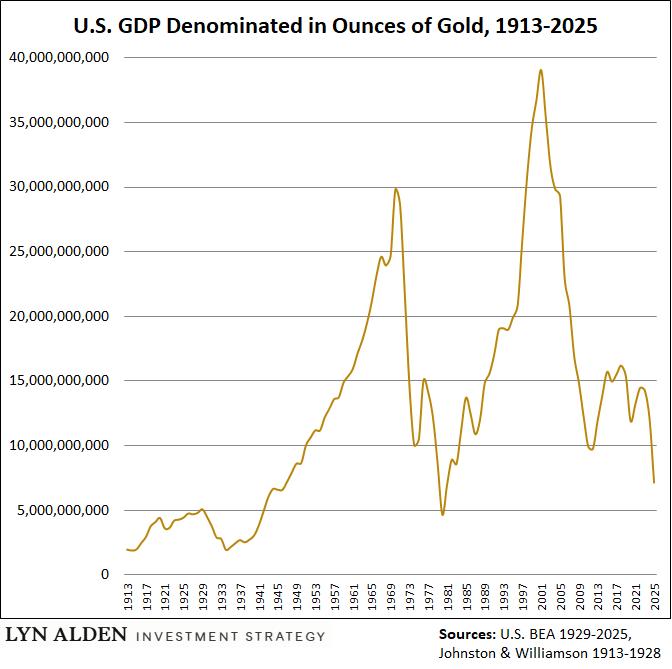

What if stock market gains were measured in gold instead of dollars?

As John Authers notes, “Denominate U.S. stocks in gold rather than dollars, and they’ve been in decline since the dot-com bubble burst 25 years ago. Stocks elsewhere have done even worse.”

#stocks#gold #markets #investors #investing

The UK's bond market is collapsing:

Today, the yield on a 30Y Bond in the UK rose to 5.64%, its highest level since 1998.

Yields in the UK are now 15 TIMES higher than they were at the 2020 low, just 5 years ago.

What is happening? Let us explain.

(a thread)