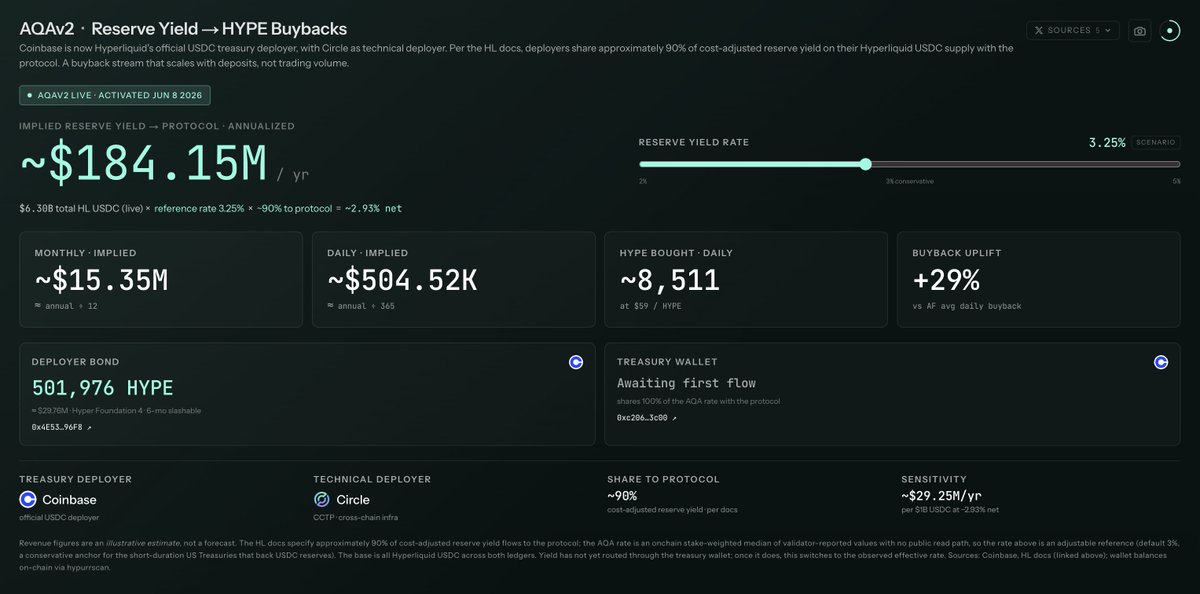

Now that AQAv2 is live we can see just how material these flows are going to be outside of the trading activity that occurs on HyperCore:

> USDC HyperEVM (CCTP): 5.37Bn

> USDC HyperCore (Bridge): 929M

> USDC Total: 6.3Bn

> Implied Yield Reserve @ 3.25% = $184.14M / yr

> Daily implied buyback pressure = $504K

> Buyback Uplift = 29%

The alternative products like HIP-3 and HIP-4 will continue to drive USDC towards Hyperliquid and AQAv2 will continue to benefit from the yield sharing from Circle/Coinbase.

HIP-3 will continue to scale becoming the venue for global price discovery for traditional markets and I think HIP-4 should see considerable traction as we enter the World Cup and Mid-Terms.

$HYPE

My personal view is I do not believe bitcoin:native can bottom until Strategy has increased its USD dividend coverage to at least 12 months (and give the market confidence that they won't sell any more bitcoin:native thereafter).

It seems to be the only way to do that IS by selling bitcoin:native.

@krugermacro Can only reduce the dividends by 25 bps + SOFR decline per month so STRC won't be sustainable until at least 2028.

Saylor has already shown to be unreliable by creating STRC in the first place and by retiring debt from 2029 with his only cash.

ethereum:0x232ce3bd40fcd6f80f3d55a522d03f25df784ee2 is by far the best looking chart in crypto holding above the previous range at $1.45 despite the massive sell off in all assets.

When bitcoin:native selling is done I expect it to be the leader in alts given structural demand for the token via buybacks and clear perps narrative

The zcash:native vulnerability issue shows that the Store of Value thesis is dead for now.

The bid for bitcoin:native has come predominantly from DATs and ETFs - $100B + over the last 2 years. It cannot be an SoV if its demand only comes from these sources.

Where does that demand come from in a market when the opportunity cost is equities with massive growth potential for the next decade due to AI.

The 'fiat debasement' argument isn't that strong when you have these US denominated assets performing significantly stronger.

I am more constructive on crypto assets with explicit value accrual, revenue share, and growth potential.

Same with zcash:native and privacy. The privacy narrative can stand on protocols that monetise privacy-enabled services, rather than on a monetary premium thesis.

With Zcash I also don't understand taking the vulnerability risk right now. Would at least wait until after the next upgrade that confirms there is no counterfeit Zcash in the orchard pool.

Anyways, rotation away from memetics / overvalued infra into cashflow generating protocols over the next 18 months.

Still early when the the CEO of @CMEGroup fails to see that perpetual futures are to be used in a different manner than dated futures and are able to provide a different type of hedge.

Hypocritical to be against this but provide 0DTE options to users

https://t.co/dBo0bSb1wz

Lows are in whenever Saylor announces he's sold a significant amount of bitcoin:native that will give him USD dividend coverage for at least 12 months.

I wouldn't be surprised if he sells $3 - 4B, which would give him cover for 2 years +.

Just rip the bandaid off.

last 10 years bull markets have been reliant on bitcoin going up first because it was such a large portion of the total crypto market cap and also in the beginning every altcoin was paired with btc on every exchange

now, we have stablecoins across all exchanges, and we also have altcoins that are attached to businesses that are not at all dependent on bitcoin

in trad markets nobody waits for gold to go up to buy amazon or google, in the same vein it makes much more sense for businesses with tokens attached to be evaluated on their own merit instead of waiting for $BTC to do well or not

believe that hyperliquid is a good example of a great business with durable revenues that has a token attached to it with no separation between another equity vehicle, & we will see many more successful businesses with similar token models post-Clarity Act & other important regulation

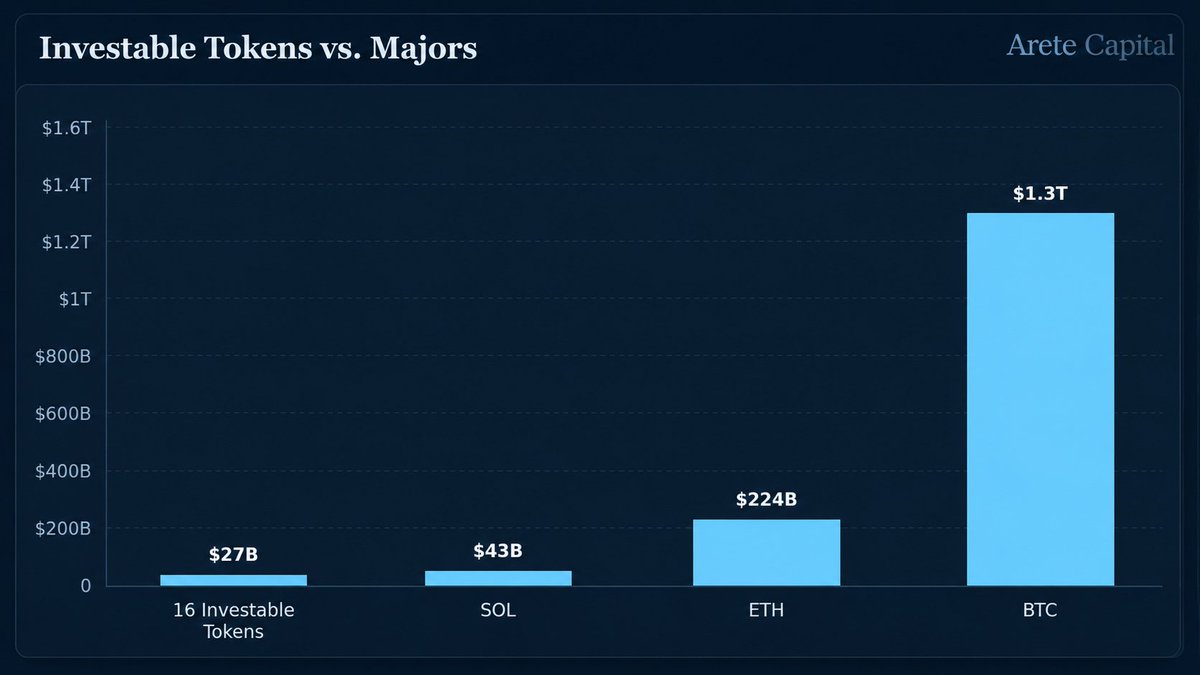

The rotation from $BTC, $ETH and $SOL and other crypto infra to strong tokens is only just starting. Take a look at the chart below.

In my estimation there are only 16 tokens that are generating revenue, are aligned with tokenholders, and have substantial growth opportunities over the next 18 months.

These have an agg market cap of $27B, and generate $1.2B in annual revenue.

As a % of Market Cap vs. the Majors this is:

65% of SOL

12% of ETH

2.1% of BTC

Those holding the above names and other overvalued infra need to move that cash somewhere. I do think some of it will exit crypto, but the majority of these holders are crypto natives who will keep their money on chain. The only logical place for these to go are sound projects with cash flows which are attributable to tokenholders.

Btw, hyperliquid:native generated 54% of the annualised revenue just by itself.

Hyperliquid.

ethereum:0x232ce3bd40fcd6f80f3d55a522d03f25df784ee2 and ethereum:0x0c1c1c109fe34733fca54b82d7b46b75cfb71f6e are my two bets for the mini alt season we're about to get as participants rotate from $BTC, $ETH and $SOL into crypto-enabled businesses.

Outside of selling $BTC, Saylor will start cutting ethereum:0x1aad217b8f78dba5e6693460e8470f8b1a3977f3 dividend rate to reduce cash outlays.

He can only cut it by a maximum of 25bps per month + a decline in SOFR.

Meaning by this time next year, STRC div rate is probably ~8.5%, reducing annual divs by $300m

This was straight-up NOT part of the rules.

It was not written down on the market, it did not make sense - and most of all, Polymarket didn't even believe it themselves.

Why? Because if it was true, the market would have closed on May 31st. The market didn't close.

The news of Saylor selling $BTC marks an inflection point in the mass crypto rotation from SoV/memetics/overvalued infra to cash flow generating businesses with actual growth prospects.

Point of no return. This divergence will accelerate from here