I’ve talked about this before but it seems like everyone forgets what a cash cow $ASTS becomes once the network is live. Look at $NFLX for the blueprint.

Netflix has around 325 million subscribers paying roughly $10 to $23 a month, and that recurring subscription model built a $310 billion company doing nearly $47 billion in revenue.

Now look at what AST is building. Nearly 60 mobile operator partners covering over 3 billion subscribers.

AST does not spend a dollar acquiring a single one of them. The carrier brings the customer, AST provides the coverage from space, and they split high margin recurring revenue.

No content to produce, no stores, no marketing. Just a subscription toll on connectivity beamed to phones already in billions of pockets.

If even a small slice of that 3 billion converts to a few dollars a month, you are looking at Netflix scale recurring revenue on infrastructure that is already paid for once the satellites are up.

And the incremental cost to serve one more subscriber from orbit is almost nothing.

Netflix proved how powerful global recurring subscriptions can be. AST is building the same model with 10x the addressable base and no content bill.

The market is watching a future cash cow get built in real time.

$ASTS - For those of us who don’t speak Cat:

To understand why this is a big deal, think of Signal-to-Noise Ratio, or SNR, like trying to hear a friend talking at a loud party. The signal is your friend's voice, and the noise is all the background chatter and music.

An SNR of 16 means your friend is speaking clearly over the noise. It is a good connection. An SNR of 21 means your friend just grabbed a megaphone.

The jump from 16 to 21 might look small, but it is actually huge. Signal strength is measured on a curve, meaning every jump of 3 basically doubles the power. So, going up by 5 means the signal is nearly three times stronger than it was before.

Here is why hitting that 21 mark on a remote island is a game changer for the company.

First, it proves their technology actually works with standard smartphones. Phones have weak antennas made to connect to cell towers a few miles away, not satellites hundreds of miles up in space moving at 17,000 miles per hour. Getting a strong signal without needing a clunky, special satellite phone is incredibly hard to do.

Second, it means real internet speeds. A weaker signal is fine for sending a basic text message, but to stream video, make clear calls, or browse the web, you need a high SNR. A score of 21 provides the clarity needed for actual broadband data.

Third, it saves battery life. When a phone struggles to connect to a weak network, it drains its battery fast by trying to shout back. A strong connection means the phone can work normally without dying quickly.

Finally, it allows the company to serve more people. A messy signal means the satellite has to keep resending lost data. A clean signal gets it right the first time, freeing up the satellite to handle more customers at once.

In short, getting this result on an unmodified phone in a remote area proves to the telecom industry and investors that AST SpaceMobile's technology works exceptionally well in real-world conditions.

$ASTS 🚨 800 MHz is not just “more spectrum.”

It’s premium low band: wide coverage, building penetration, mature device ecosystem, hundreds of millions of compatible phones.

Speculative upside….. If AST secures meaningful D2D access here, the market could eventually price in $5B–$20B+ of added strategic value roughly $14–$55 more per share.

Today it’s an FCC filing.

Tomorrow: A U.S. D2D moat. 🛰️🌐🇺🇸

$ASTS - AST SpaceMobile has now secured integration into the US FirstNet public safety network (in coordination with AT&T) and effectively won Japan’s J-LEO initiative via its joint venture with Rakuten Mobile.

When the world’s two most demanding telecommunications and public safety regulators independently audit a technology and reach the exact same conclusion, it sets a global precedent.

These aren't just commercial deals, they are sovereign mandates for national security and disaster resilience.

The underlying reason AST SpaceMobile triumphed in both arenas reveals exactly why it makes overwhelming economic sense for the rest of the world to adopt the same solution.

The core differentiator, and the reason AST SpaceMobile defeated alternatives like SpaceX's Starlink in Japan's strict procurement process, is data sovereignty.

Most LEO mega-constellations rely on inter-satellite laser links to route traffic across the globe. While highly efficient for standard global broadband, this introduces a massive national security liability: a citizen's data (or a first responder's transmission) can cross international borders before being downlinked to a ground station.

AST SpaceMobile utilizes a "bent pipe" architecture. The massive BlueBird satellites act as space-based cell towers, catching the signal from an unmodified smartphone and bouncing it straight down to a local gateway within that specific country's borders. All data routing, core network control, and encryption keys remain strictly on domestic soil. For governments prioritizing disaster resilience and national security, this is the only acceptable architecture.

In the wake of geopolitical tensions, countries from the EU to the Middle East are attempting to build their own sovereign LEO constellations. However, orbital mechanics dictate that LEO satellites circle the globe at roughly 17,000 mph; they cannot simply hover over a single nation.

If a country builds a sovereign constellation to ensure continuous overhead coverage, those multi-million dollar satellites will spend over 90% of their orbit flying over other nations, providing zero value to the state that paid for them. It is a wildly capital-inefficient strategy.

AST SpaceMobile solves the "Sovereign LEO Dilemma" by offering a shared global infrastructure with strict local partitioning.

Nations do not need to spend billions designing, launching, and replacing their own orbital hardware. They leverage a network funded and maintained by private capital.

The network utilizes the standard sub-6 GHz spectrum already owned by domestic mobile network operators (MNOs). It doesn't require carving out new global spectrum allocations or navigating complex regulatory workarounds.

First responders and citizens don't need expensive proprietary satellite phones or specialized ground terminals. The network connects directly to the standard 5G smartphones they already have in their pockets.

By adopting the FirstNet/J-LEO model, governments guarantee nationwide, domestically routed emergency communications at a fraction of the cost of a bespoke space program.

The blueprint has been validated by the United States and Japan.

Here is a list of the major sovereign (and heavily state-backed) Low Earth Orbit (LEO) satellite initiatives globally. They are driven by a mix of national security, digital autonomy, and disaster resilience.

Japan: J-LEO

A roughly $1 billion state-backed constellation focused on disaster resilience and consumer direct-to-device (D2D) connectivity. It mandates that all network control and data routing remain entirely within Japan to prevent communication blackouts during natural disasters.

Taiwan: Beyond 5G (B5G)

Spearheaded by the Taiwan Space Agency, this program is developing independent LEO communication payloads to ensure Taiwan’s command systems and internet survive if its highly vulnerable subsea cables are severed by geopolitical conflicts or earthquakes.

India: ISRO & Jio Platforms

Driven by strict data localization laws, India's space agency (ISRO) and national telecom champions like Jio are developing sovereign LEO networks. The goal is to connect rural India without allowing sensitive domestic data to touch foreign-owned infrastructure.

South Korea: Project 425 & Hanwha Systems

A dual-track approach. Project 425 is a sovereign military constellation for independent reconnaissance of North Korea. Concurrently, defense contractor Hanwha Systems is building a government-supported commercial LEO network to power 6G and urban air mobility.

European Union: IRIS²

The €10.5 billion Infrastructure for Resilience, Interconnectivity and Security by Satellite. Spurred by the war in Ukraine, this multi-orbit network of nearly 300 satellites will provide highly encrypted communications for EU militaries and governments, ensuring independence from American commercial operators.

United Kingdom: The Sovereign Stake (OneWeb)

Instead of building a network from scratch, the UK government invested £400 million to rescue OneWeb (now Eutelsat OneWeb) from bankruptcy. This secured a "golden share," guaranteeing the UK prioritized access and veto rights over a global LEO network for defense and remote connectivity.

Saudi Arabia: Vision 2030 LEO

As part of its economic diversification strategy, Saudi Arabia is actively planning a sovereign LEO network to ensure absolute national autonomy over its digital infrastructure. The current challenge is structuring international partnerships to make a localized network financially viable.

Oman: Omansat & Space Policy 2023–2033

Oman is embedding space infrastructure directly into its national security strategy. By developing domestic satellites (like Omansat-1) and strict regulatory frameworks for orbital slots, Oman is prioritizing sovereign data control and regional trust over rapid, massive scale.

United Arab Emirates (UAE): MBRSC LEO Programs

The UAE is heavily investing in localized satellite assembly, integration, and testing (AIT). Programs out of the Mohammed Bin Rashid Space Centre are rapidly building sovereign Earth observation and communication fleets (such as the upcoming Sirb radar constellation) to reduce reliance on foreign hardware.

Canada: Telesat Lightspeed

While Telesat is a commercial operator, the Lightspeed LEO constellation is heavily backed by over $2 billion in Canadian federal and provincial loans and subsidies. The government considers it a strategic sovereign asset, required to guarantee secure connectivity for Canada’s vast, unserved Arctic territories and its national defense forces.

AST SpaceMobile could win them all.

I hadn’t thought about this. Like a G-7 country buying some F-35s as part of a broader fleet. $ASTS

Remember Golden Dome? Stock price lower than when this was announced. Bet the shorts forgot. Good luck to them.

Indian Department of Telecommunications says that “the rules require all Indian user traffic to be routed through domestic gateways, not international gateways or inter-satellite links.”

This is why $ASTS transparent architecture continues to win globally. It secured the JLEO award, united top European MNOs (ex DT) under Satellite Connect Europe, and won a Brazilian S-band allocation. Meanwhile, Starlink is forcing a square peg into a round hole, pushing a regenerative, mesh model that clashes with a new global landscape where national sovereignty dictates telecom policy

Si crees que ya se te escapó "la mejor oportunidad del momento"... espera

Mientras todos huyen, la empresa está construyendo en silencio lo que podría ser la subida más fuerte de su historia

La acción cayó.

La empresa no.

$ASTS acaba de caer ~ 50% desde máximos

Hilo 🧵👇

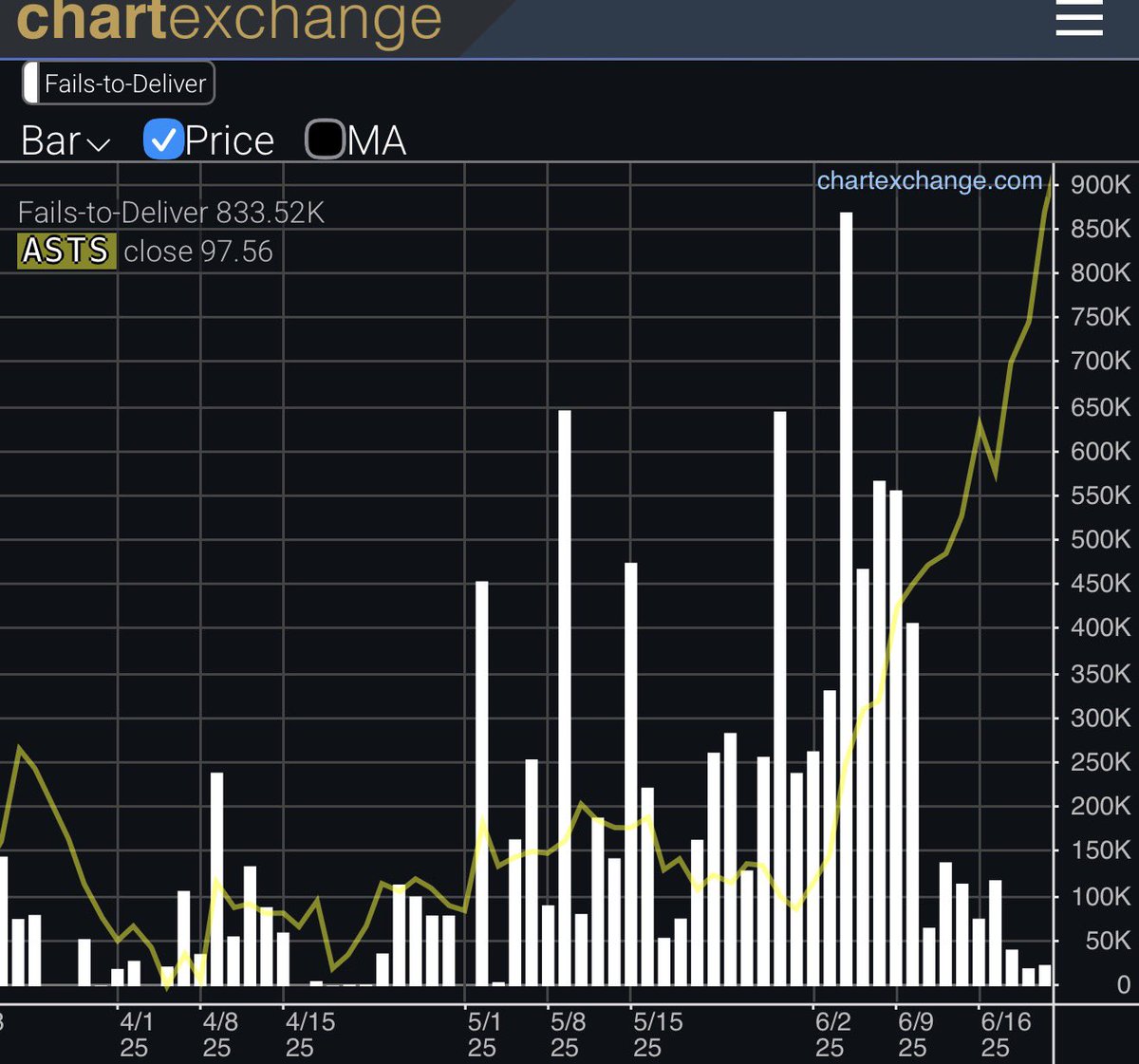

Before the last big runup in shareprice, in April 2025, there was low availability of shares to short.

As price consequently went up dramatically (yellow line) there were a lots of fail to deliver (white bars). Shorts that couldn’t give back their shares when asked.

1/2

🚨 ASTS: La señal técnica MÁS fuerte de short squeeze que hemos visto en mucho tiempo

Lo que está pasando con las Shares Available to Short es una de las señales más alcistas a corto plazo en el mundo de los shorts.

¿Qué significa “Shares Available”?

Son las acciones reales que hay disponibles en los pools de préstamo (Interactive Brokers, Ortex, Fintel, iborrowdesk, etc.) para abrir nuevos shorts.

No es el short interest total, es el “stock del almacén”.

Lo que acaba de pasar:

En 24 horas pasó de 1.4 MILLONES a solo ~65K shares disponibles.

Esto no es normal. Es extremadamente alcista.

¿Por qué cayó tan fuerte el inventario?

Hay 4 razones principales (suelen venir combinadas):

a) Nuevos shorts entrando masivamente (muchos bajistas creyeron que el +21% del viernes era excesivo)

b) Lenders retirando sus acciones (fondos grandes vendiendo o pasando a cash)

c) Salida de margen de retail (los “apes” moviendo acciones de margen a cash para impedir que las presten)

d) Cierre de shorts existentes (recompra)

Cadena de causalidad que puede activarse:

Inventario cae → Borrow fee se dispara → Shorts antiguos pierden rentabilidad → Algunos cierran (recompran) → Precio sube → Stop-loss de otros shorts saltan → Más recompras → SHORT SQUEEZE

Y si encima coincide con gamma squeeze por calls (ASTS tiene mucho call open interest en $90-110), la mecha es vertical.

Pasar de 1.4M a 65K en 24h significa que alguien (institucional o retail masivo) ha consumido casi todo el inventario disponible. Esto genera una tensión real en el préstamo de acciones.

¿Coincidencia o se está cocinando algo grande?

El mercado lo dirá en las próximas horas, sesiones.

MARKET REALITY AST Will Have 100% Japan Market Share - Nobody Gets It Yet

AST SpaceMobile is going from Japan's scrappy fourth-place carrier partner to what will be 100% market share across the entire country - and the market still hasn't figured it out. This is a sign of how things unfold globally.

$ASTS I dk who needs to hear this but according to my math short interest is now roughly 48.3% of the float.

388m shares outstanding

Abel owns ~78m

Other insiders/5%+ holders own ~90m

This leaves 220m, subtract 20% of that from sub 5% strategics/long term investors and you get to 180m. I think this is a better estimate of the actual float. They’re short 87m shares. 87/180 =0.483

And this is no bullsh*t company. This is a prime U.S defense contractor that is building out the future of global D2D telecommunications and national defense priorities in several countries.

If this was a pre IPO company I think it would be raising at 100b right now. I have some credibility on this bc I head private markets for an investment bank.

Whoever is short has gone off the edge and this is going to squeeze. It’s not if anymore, they doubled down and doubled down, so now it’s when. I think very soon given availability to borrow shares has now dried up.

What happened in 2021 with GameStop was a much smaller situation. This short is 7 times the size of that at $7.5b notional now.

Ticking time 💣. /End

$ASTS Great point @ancapspace !

This way the satellites are ptotected by governments and any attack on the constellation will be threaten as attack on the current country!

$ASTS good morning.

- we officially won JLEO

- next in the docket we have unfurling news, shipping news, and high likelihood of new launch provider news

- we could get news of a partnership with Canada today, we’re waiting on official TMobile partnership news

- we might partner with VSAT soon

- still waiting on gov/military updates. Seems like BB 8-10 may have been doing some testing

- we’re hiring 500 new employees, a major expansion

- over a billion of cash on hand

- clearly past the bottom and ready to make major new ATH with a ton of short interest to power through

We’re going past 90 for sure…100? Higher?