The deal and funding database built for biopharma. Curated deal comps, company profiles, pipelines, dedicated analyst support so you do better research faster

Biopharma therapeutics and platform financing activity in Q1 2026 reflected a strengthening IPO market alongside more selective follow-on and PIPE funding conditions.

Read our research

https://t.co/yi7uw2beDN

Biopharma therapeutics and platform financing activity in Q1 2026 reflected a strengthening IPO market alongside more selective follow-on and PIPE funding conditions.

Read our research

https://t.co/5KXdcCcaNG

We’re excited to share that Chris Dokomajilar, Founder & CEO of DealForma, will be speaking at the CELS Canada in the Valley Showcase 2026 on May 14.

Chris will lead a session titled “Biopharma Venture, Licensing, IPOs, and M&A Trends Through Q1 2026.”

https://t.co/5jrmK49EOg

WSJ cited DealForma data showing that China and Hong Kong companies accounted for 50% of large pharma in-licensing deals with at least $50 million upfront so far this year, underscoring rising global pharma interest in China-originated assets.

https://t.co/n8fHWwsFWZ

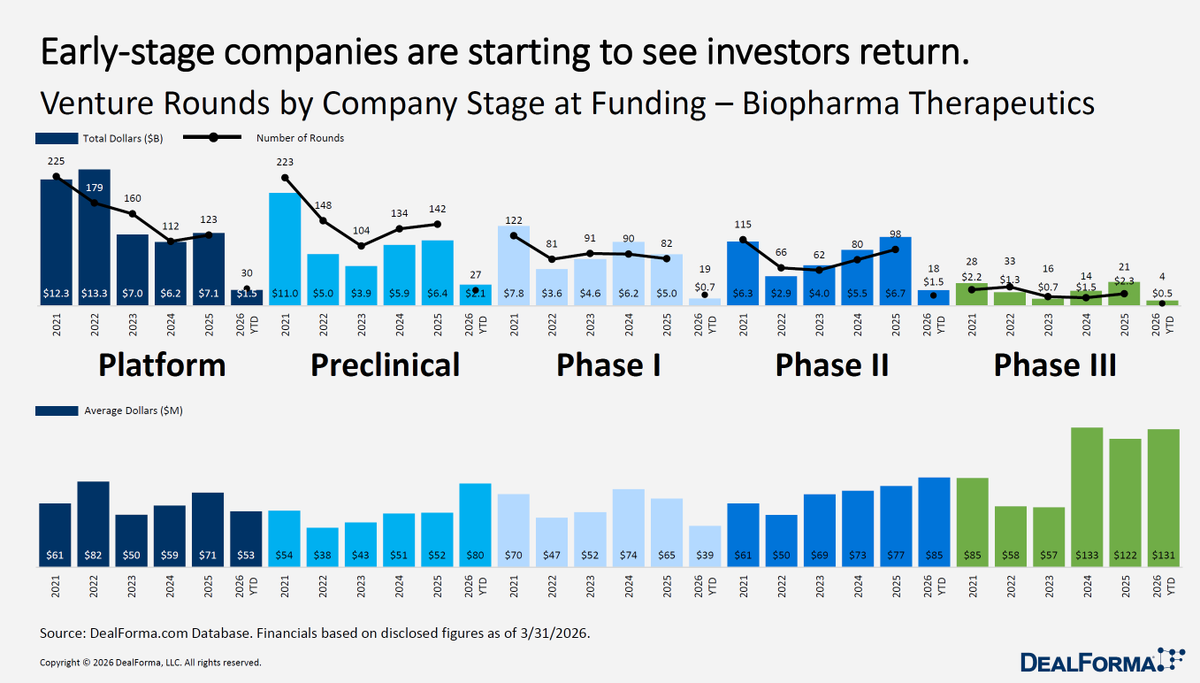

Early-stage biopharma funding rebounded in 2025, but Q1 2026 is mixed: softer at platform/preclinical, while Phase II–III remains resilient with dollars and check sizes holding near 2025 levels.

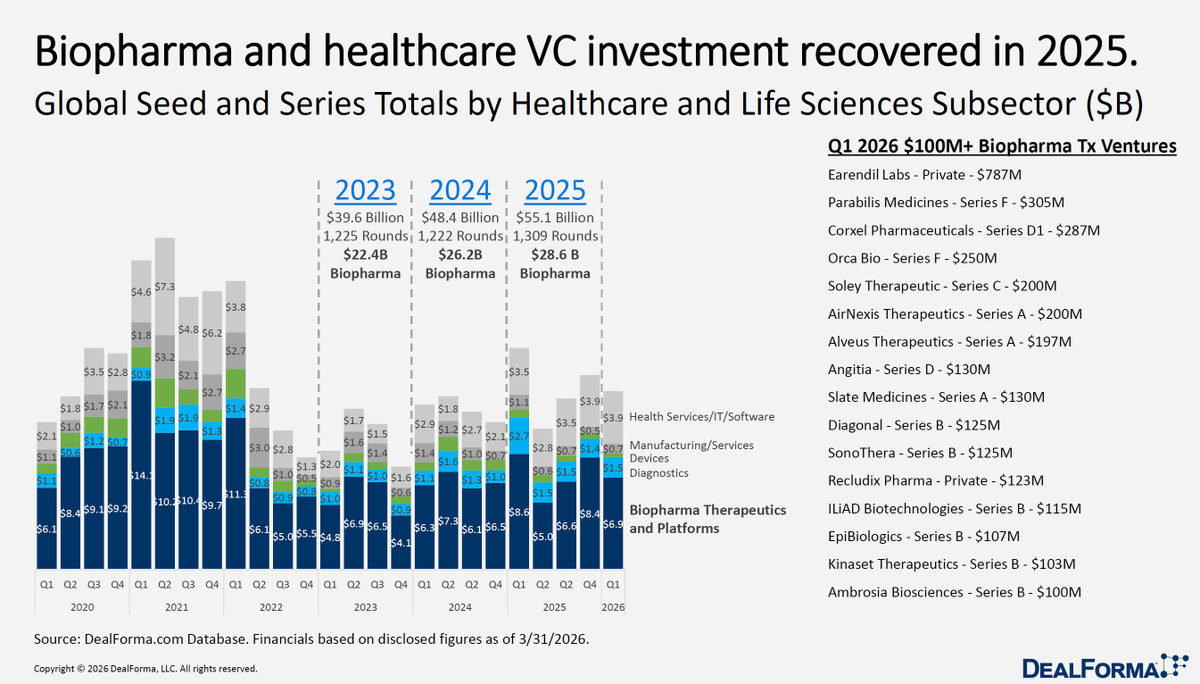

Biopharma and healthcare VC investment rebounded in 2025 to $55.1B (1,309 rounds), up from $48.4B in 2024, with biopharma specifically increasing to $28.6B. Momentum has carried into Q1 2026 with several large $100M+ rounds.

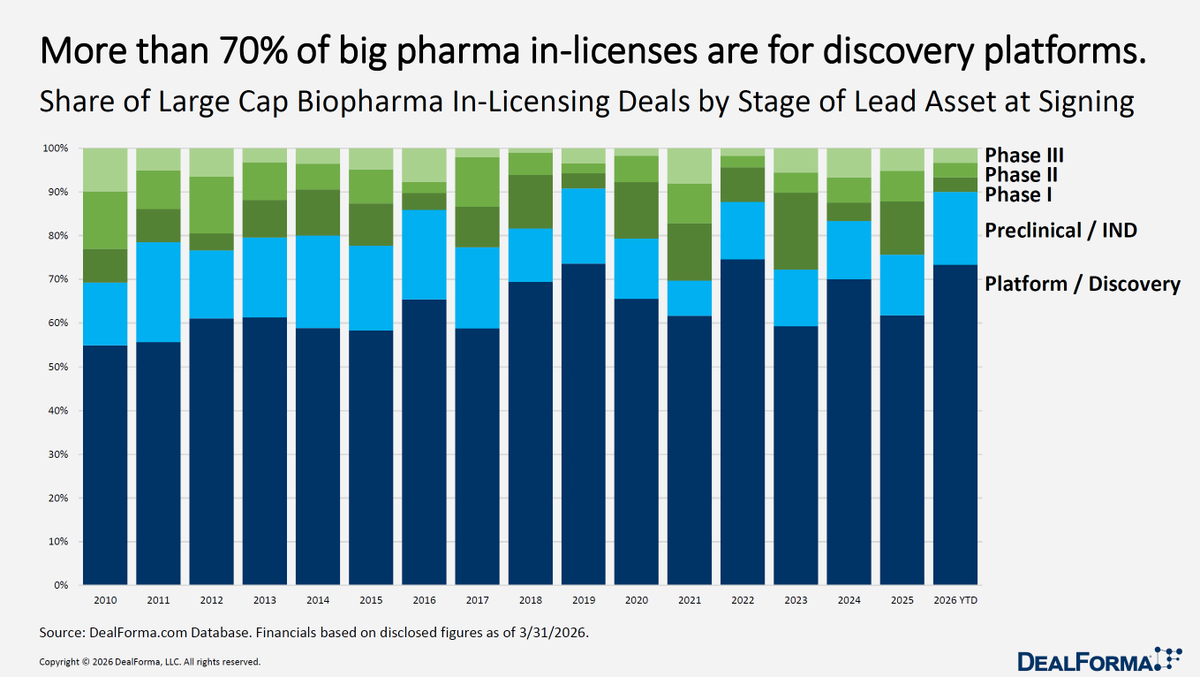

Big pharma in-licensing remains heavily skewed toward early-stage assets, with platform/discovery deals consistently making up ~60–70%+ of activity, rising to ~75% in 2026 YTD. Late-stage (Phase II–III) deals continue to represent only a small share.

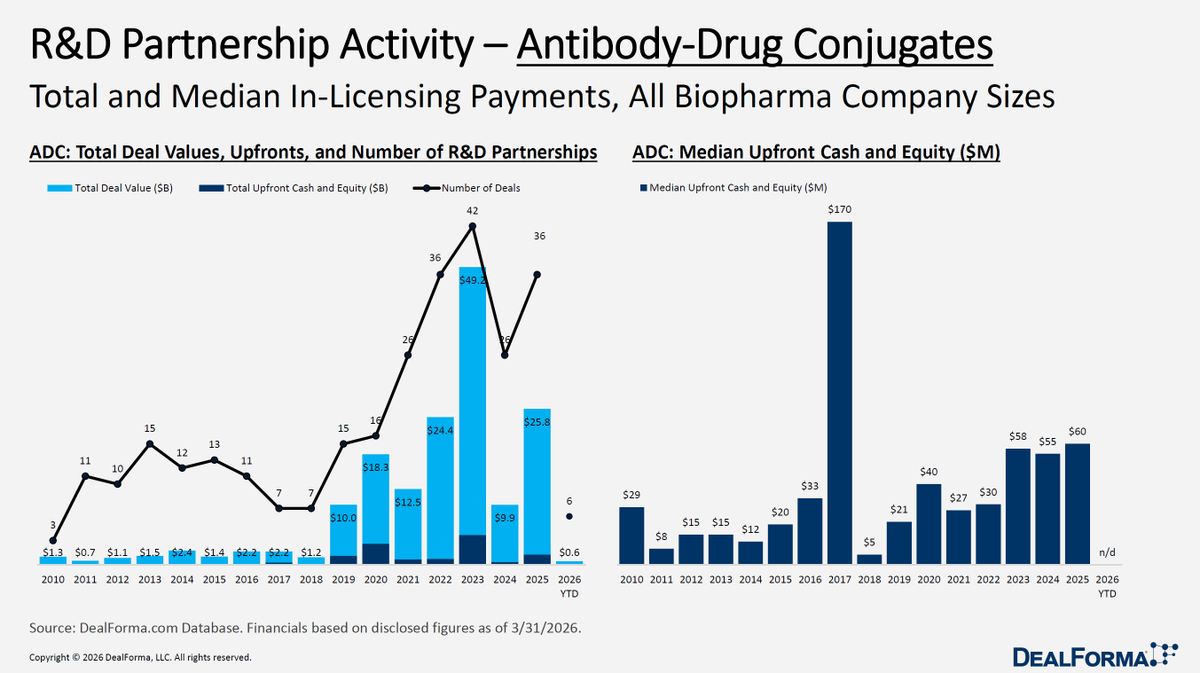

ADC deal activity remained strong in 2025, with total value reaching ~$25.8B across 36 deals and median upfronts rising to ~$60M, signaling continued demand for high-quality assets. In 2026 YTD, activity is more muted (~$0.6B; 6 deals)

Big pharma in-licensing spend is heavily concentrated in oncology and biologics, with cancer driving the majority of upfront payments each year and biologics/antibodies/ADCs dominating modality spend (peaking at ~$9.7B in 2025).

Biopharma & medtech entered 2026 with selective momentum, with J.P. Morgan’s reports — powered by DealForma — highlighting strong licensing, M&A, and early IPO recovery.

Download the full reports for deeper insights.

https://t.co/rZtvj5ILGh

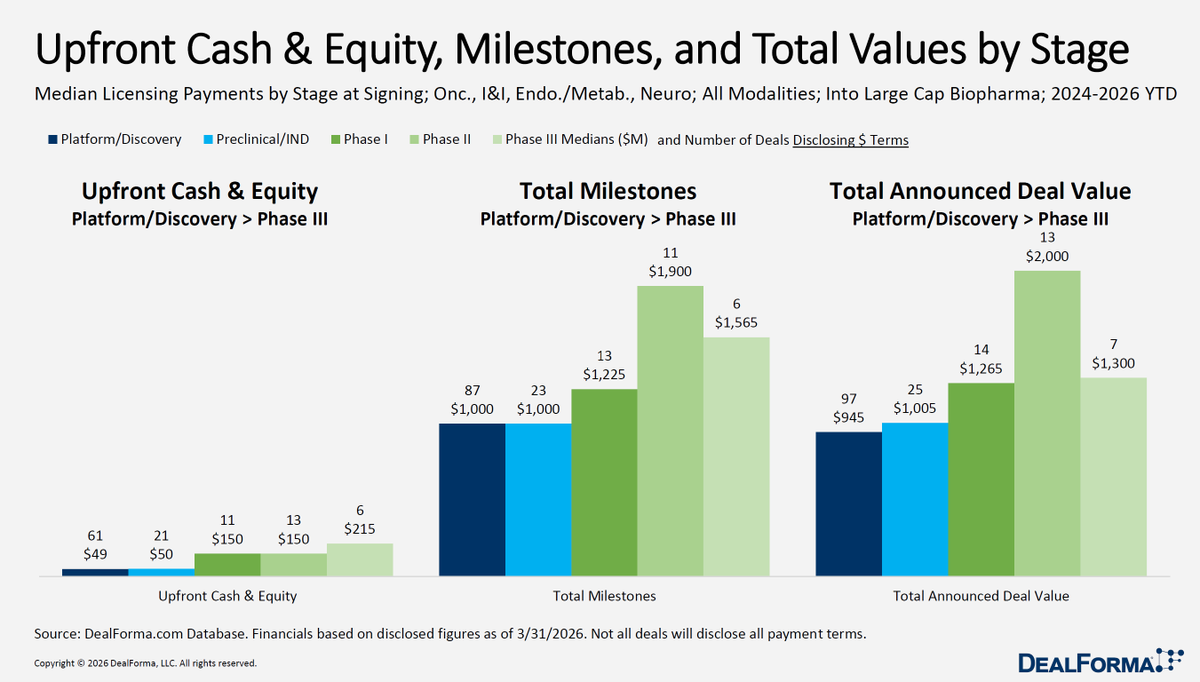

Upfront payments remain relatively compressed across stages (~$49M–$215M), but total deal value expands significantly in later stages, driven by milestones—peaking around ~$2.0B in Phase II and ~$1.3B in Phase III.

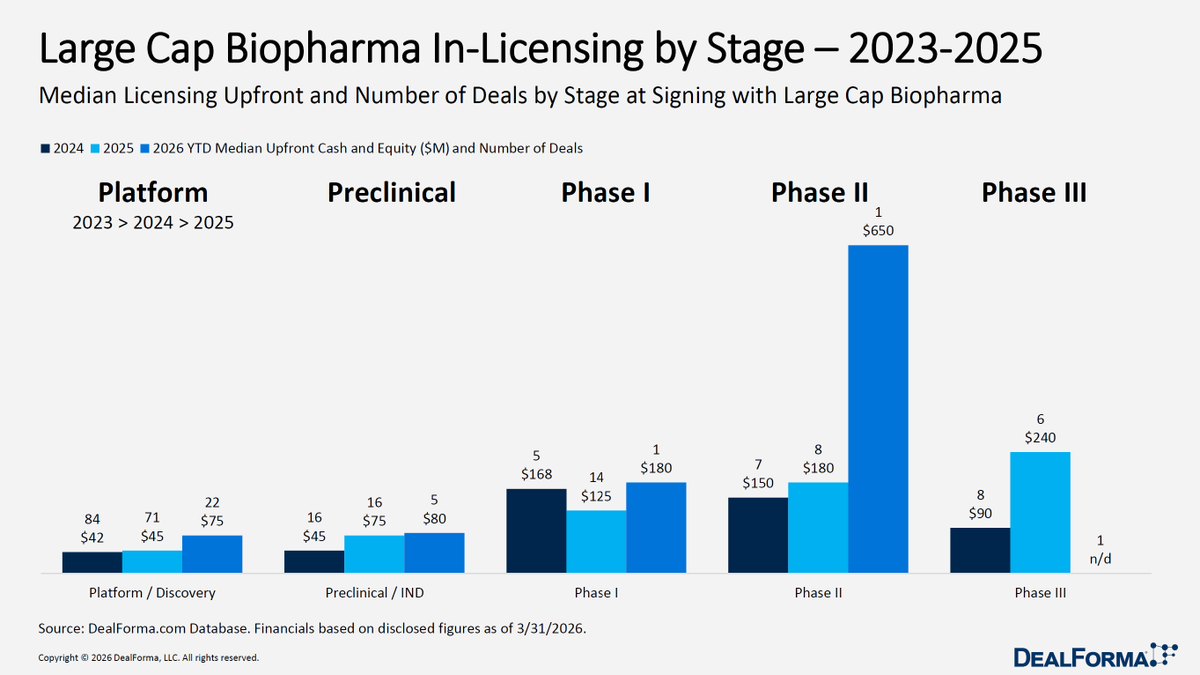

From 2023–2025, upfronts increased with stage, with later-stage deals commanding the highest premiums. In Q1 2026, this trend accelerated—Phase II median upfront hit ~$650M (single deal) and Phase I ~$180M—showing a shift toward fewer, high-value later-stage deals.

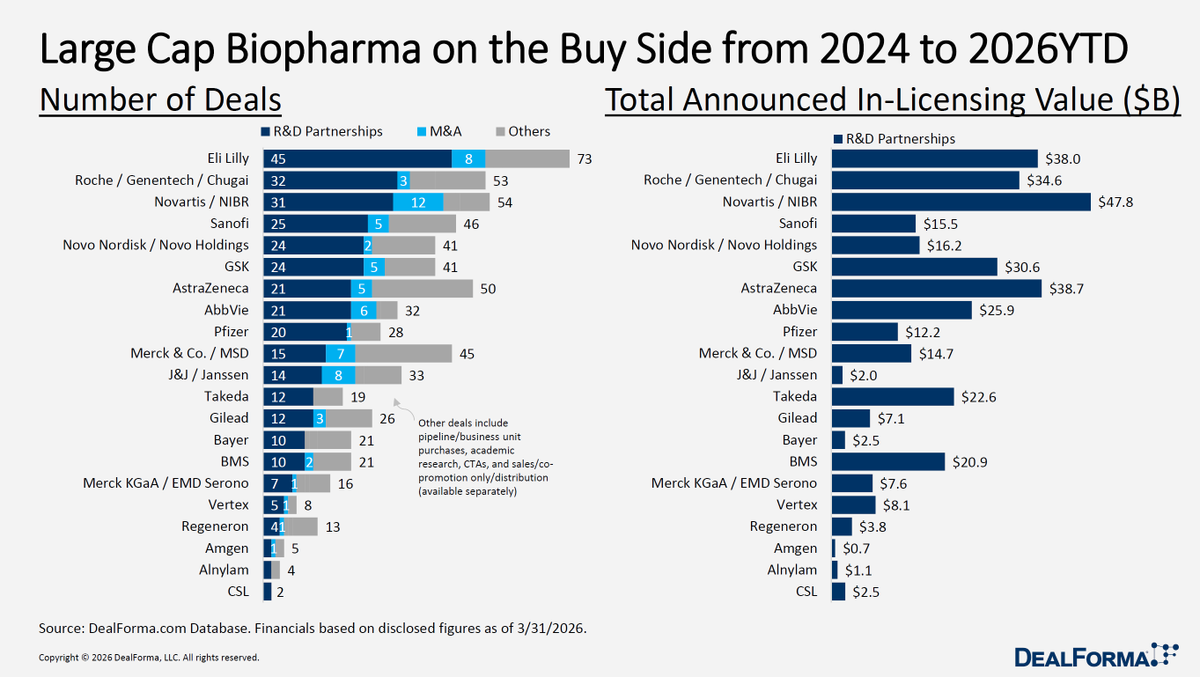

Large-cap biopharma dealmaking from 2024–2026 YTD is led by Eli Lilly, Roche, and Novartis in volume, with activity heavily skewed toward R&D partnerships over M&A. In terms of value, Novartis ($47.8B), AstraZeneca ($38.7B), and Eli Lilly ($38.0B) lead in in-licensing spend

Big pharma significantly increased sourcing from Chinese biopharma through 2025, with deal value rising to $68.7B across 19 large transactions, alongside growing upfront payments. In Q1 2026, China accounted for ~50% of big pharma deals and ~75% of upfront capital.

Licensing upfronts in 2025 were relatively balanced across regions (~$5.0B U.S., $5.1B EMEA, $7.3B APAC), with APAC leading overall. In Q1 2026, activity shifted sharply toward APAC, which generated $3.4B in upfronts, compared to $1.4B in the U.S. and just $0.4B in EMEA.

Neurology deal activity in 2025 was mixed, with weaker R&D partnerships offset by strong M&A growth, steady venture funding, and improved IPO activity, signaling confidence in later-stage and clinically validated assets.

Read our research

https://t.co/JkhAG1kZWO

China is leading large biopharma licensing deals in early 2026, with strong M&A activity and continued momentum showing sustained dealmaking and bigger payouts despite a slight dip in deal volume.

Read it here

https://t.co/waerjJjdAr

Biopharma licensing reached a record in 2025 with $259.6B total value and $17.1B upfront across 468 deals, and in Q1 2026 delivered $79.4B total value and $4.9B upfront vs. $61.6B and $5.2B in Q1 2025, with top upfronts led by CSPC/AstraZeneca ($1.2B) and RemeGen/AbbVie ($650M).