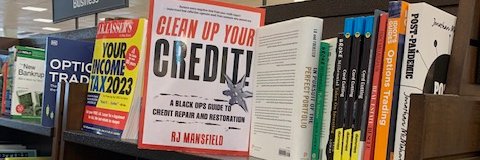

Author of "Clean Up Your Credit"-Consulted @ FICO™

@DebtAssassin15

Owned a collection agency-Prev VP at Guardian Bank-Ruined my credit to prove any negative on your credit report can be removed if you know how the system works!

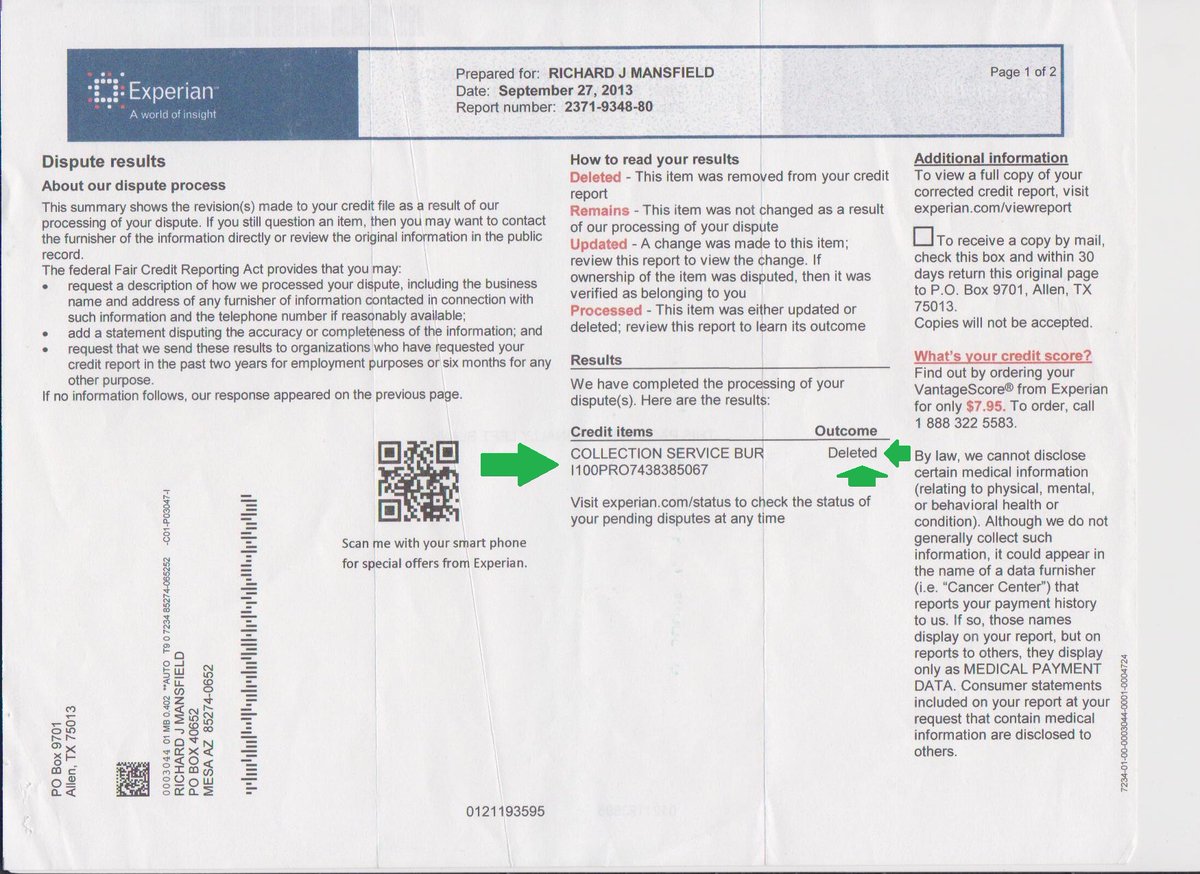

I get negative items removed from credit reports! I owned a collection agency. I know how the system works. I ruined my credit to prove what I knew in theory really works. I wrote a book about it & coach ppl thru the puzzle know as credit repair. email me https://t.co/lbXehYqcla

The credit reporting system is a mess! I've reviewed reports since 1972 & been part of a class action suit against TransUnion. If you know how the credit system works you can get every negative removed from your credit reports. Questions? Email me at https://t.co/b3MnGZ2qkq

@Buckeye19682 I don't want to sound like I'm avoiding the question but it depends on your situation. Do you have a good score (670 or over)) you're looking to increase or a low score (under 670) or very low score (under 600)?

I've reviewed credit reports since 1972 when reports came from teletype machines. Every credit report contains errors that can be used to remove every negative item. I previously owned a collection agency. I know how the system works. Questions? Ask away. https://t.co/6XHX5FgMeP

I don't want to sound like I'm avoiding the question but it depends on what your situation is. Do you have a good score (over 670) you're looking to increase or a low (under 670) or very low (under 600) score?

Schools should replace teaching subjects like Geometry & Literature; things most will never use. Make them electives!

Replace it with:

Understanding credit.

Like-How to-

Read a credit report

Start & improve your credit

Qualify for a mortgage.

What do you think should be taught?

Credit isn't a disease. If used properly it's a cure for the lack of access to sufficient capital for large purchases. Without credit the American Dream of owning a home would be out of reach for most. Few ppl can pay cash for a house or car.

Coerced Debt is Abuse! How it affects you & what you can do.

Coerced debt is non-consensual. It is identity theft when an abusive partner uses your personal info to incur debt without your knowledge and/or permission. Some forms of coerced debt occur when the abuser opens a credit card, cell phone account, any kind of loan, or even files fraudulent tax returns. Obtaining credit or using credit you already have without your consent is fraud!

Coerced debt also includes other forms of non-consensual credit transactions that do not look like identity theft. An abusive partner may utilize the threat of physical or emotional harm to the abused partner, their children, or pets, to intimidate you to obtain new credit or provide access to assets to financial products you already have like credit cards or bank accounts.

Severe Consequences of Coerced Debt

The impact of coerced debt on the abused partner is devastating. Perpetrators of abuse use coerced debt to gain financial control over the abused partner's economic choices. Many abused partners do not discover unknown coerced accounts until after they’ve been placed for collection, and their credit has already been damaged.

Additionally, the abused is often unable to obtain credit from traditional lenders and are driven to borrow from predatory sources like payday lenders. These high-cost loans aggravate an already desperate financial situation, trapping the abused partner in insurmountable debt.

Moreover, partners of domestic violence are apt to stay in abusive relationships if ending the relationship would result in poverty or homelessness. If children are involved, partners are even more prone to stay in an abusive relationship to shield their children from economic instability.

A Safety Plan as an Immediate Priority

Because coerced debt is often linked to physical domestic violence, the first step is to ensure your safety and that of loved ones.

Partners in abusive relationships should always develop a safety plan. Help is available from the National Domestic Violence hotline at 800-799-7233. If you call, make sure you are in a safe place to talk and preferably alone! DO NOT trust any third-party while making this call. Even the best-intentioned friends say things they shouldn’t to people they shouldn’t!

IMPORTANT! If you dont payoff credit cards monthly pay as much as you can as soon as its billed. DON'T wait for the due date. You're charged interest every day on unpaid balances. Make a payment as soon as your billed so you're not charged interest on the amount you're paying.

@ArcOgre007 There are tons of things that should be illegal for banks. Unfortunately, the bank lobby is strong & most politicians are weak & value money over constituents.

@ArcOgre007 There are tons of things that should be illegal for banks. Unfortunately, the bank lobby is strong & most politicians are weak & value money over constituents.

Take Action: Bank of America Customers Should Opt-out and Consider Changing Banks to Avoid New Forced Arbitration Clause

Bank of America recently announced a decision to insert a forced arbitration clause in the fine print of its Online Banking Service Agreement. BofA’s agreement gives customers just 60 days to opt-out after they receive notice, so for many customers this clock has already started ticking.

Forced arbitration blocks customers’ access to the court system and eliminates their right to a jury trial when they are harmed, instead forcing them into biased, closed-door proceedings where consumers rarely win. It also prevents people from joining together in class action lawsuits to fight back against systemic harms.

Act quickly. Contact BofA immediately to maintain your right to a judge and jury trial. Follow these simple steps:

1. Visit: https://t.co/hdZV76cDQT

2. Log in to your online BofA account

3. Click on the “Submit” button on the bottom of the page

Or call: 800-283-8875

Not all banks and credit unions use forced arbitration. In addition to opting out, or if it is too late, BofA customers can transfer to a bank or credit union that does not take strip rights away in the fine print.

Act now. You have just 60 days to opt out to maintain your rights. Tell Bank of America that you say NO to forced arbitration ripoff clauses.

If someone forces you to obtain credit THAT'S ABUSE. It's called COERCED DEBT You feel helpless if they're still around but when they're gone, if you want it removed from your credit report there is a way! Ask me. Go to https://t.co/wk7di2aEKQ

@bobby_blam Great question! The fear of CFPB involvement was no doubt helpful. But the laws governing the debt collection industry-FDCPA & credit reporting-FCRA are still the same. I've been doing this for 50+ yrs. Long before the CFPB existed.

I get negative items removed from credit reports! I owned a collection agency. I know how the system works. I ruined my credit to prove what I knew in theory really works. I wrote a book about it & coach ppl thru the puzzle know as credit repair. email me https://t.co/lbXehYqcla

This is what artificial intelligence says about me> RJ Mansfield, known as "The Debt Assassin," is often quoted in financial coaching materials: The book is his main publication where he details his "Black Ops" strategies for settling debts and repairing credit. You can find it on Amazon or through major book retailers. Clean Up Your Credit!: A Black Ops Guide to Credit Repair and Restoration Credit Restoration Coaching: His methods and quotes are frequently cited in credit repair forums and by individuals following his specific debt-settlement systems. Media and Interviews: As a former bank vice president and collection agency owner, his expertise is often quoted in financial advice articles focusing on aggressive credit recovery. Clean Up Your Credit! : A Black Ops Guide to Credit Repair and Restoration by RJ Mansfield * Call Number: eBOOK. * Publisher: Guilford, Connecticut : Lyons Press, [2022] * Target Age: Adults.📷Brooklyn Public Library📷 Clean Up Your Credit!: A Black Ops Guide to Credit Repair and Restoration says ... you could do this yourself but if you try to go it alone, the credit repair journey can be a nightmare. This book introduces a step-by-step credit repair system📷https://t.co/zAcaSWp5fM📷 A Black Ops Guide to Credit Repair and Restoration : Mansfield, ...About the Author RJ Mansfield is a credit repair coach who has helped hundreds of clients improve their credit scores. How does RJ Mansfield's approach differ from traditional credit repair? "Black Ops" strategies focus on aggressive legal technicalities rather than standard negotiation.RJ Mansfield, known as the "Debt Assassin," differentiates his approach. through what he calls Legal "Quirks" While traditional credit repair focuses on settling debts or removing inaccuracies, Mansfield teaches how to use specific "quirks" in consumer protection laws to remove negative items that are actually yours. Aggressive Litigation: His system includes step-by-step guides and actual legal documents used to file lawsuits against major credit bureaus in small claims court. Traditional services never provide these tools for individual litigation. "Insider" Experience: Unlike most credit coaches, Mansfield was a bank vice president in charge of collections and owned a collection agency. He uses his knowledge of how the industry operates "from the inside" to challenge credit reporting agencies. Radical Proof-of-Concept: To prove his methods, Mansfield famously intentionally defaulted on all his own debts—including a mortgage and car—dropping his score to 461 before restoring it to 742 in five months. Focus on Speed: Mansfield provides a significantly faster restoration timeline (months vs. years) by bypassing standard dispute channels in favor of more aggressive challenges. For those looking to apply these methods, he details them in Clean Up Your Credit!: A Black Ops Guide to Credit Repair and Restoration. Go to https://t.co/AIkNbiSwWO

![DebtAssassin15's tweet photo. This is what artificial intelligence says about me> RJ Mansfield, known as "The Debt Assassin," is often quoted in financial coaching materials: The book is his main publication where he details his "Black Ops" strategies for settling debts and repairing credit. You can find it on Amazon or through major book retailers. Clean Up Your Credit!: A Black Ops Guide to Credit Repair and Restoration Credit Restoration Coaching: His methods and quotes are frequently cited in credit repair forums and by individuals following his specific debt-settlement systems. Media and Interviews: As a former bank vice president and collection agency owner, his expertise is often quoted in financial advice articles focusing on aggressive credit recovery. Clean Up Your Credit! : A Black Ops Guide to Credit Repair and Restoration by RJ Mansfield * Call Number: eBOOK. * Publisher: Guilford, Connecticut : Lyons Press, [2022] * Target Age: Adults.📷Brooklyn Public Library📷 Clean Up Your Credit!: A Black Ops Guide to Credit Repair and Restoration says ... you could do this yourself but if you try to go it alone, the credit repair journey can be a nightmare. This book introduces a step-by-step credit repair system📷https://t.co/zAcaSWp5fM📷 A Black Ops Guide to Credit Repair and Restoration : Mansfield, ...About the Author RJ Mansfield is a credit repair coach who has helped hundreds of clients improve their credit scores. How does RJ Mansfield's approach differ from traditional credit repair? "Black Ops" strategies focus on aggressive legal technicalities rather than standard negotiation.RJ Mansfield, known as the "Debt Assassin," differentiates his approach. through what he calls Legal "Quirks" While traditional credit repair focuses on settling debts or removing inaccuracies, Mansfield teaches how to use specific "quirks" in consumer protection laws to remove negative items that are actually yours. Aggressive Litigation: His system includes step-by-step guides and actual legal documents used to file lawsuits against major credit bureaus in small claims court. Traditional services never provide these tools for individual litigation. "Insider" Experience: Unlike most credit coaches, Mansfield was a bank vice president in charge of collections and owned a collection agency. He uses his knowledge of how the industry operates "from the inside" to challenge credit reporting agencies. Radical Proof-of-Concept: To prove his methods, Mansfield famously intentionally defaulted on all his own debts—including a mortgage and car—dropping his score to 461 before restoring it to 742 in five months. Focus on Speed: Mansfield provides a significantly faster restoration timeline (months vs. years) by bypassing standard dispute channels in favor of more aggressive challenges. For those looking to apply these methods, he details them in Clean Up Your Credit!: A Black Ops Guide to Credit Repair and Restoration. Go to https://t.co/AIkNbiSwWO](https://pbs.twimg.com/media/HGv12F4aEAA0N1i.jpg)