$ASTS X is full of noise on this name.

Wrong counts, wrong levels, wrong conclusions.

I don't post for the likes. I post because the chart tells a clear story, and most people are reading it wrong.

See you at $170. You choose the winning team.

Even if this support breaks.

I am going all in at $9 at latest.

$SMR hitting $90 before 2030 is not unrealistic

This would be a 10x from $9 and still more than 5x right now

6 stocks I would buy right now

$JD - https://t.co/89x3uYdGY3

Among Chinese companies, JD remains one of the few major stocks that has yet to fully recover, but that may soon change.

JD operates China’s largest self-owned logistics network, covering 99% of the population, with over 90% of urban orders delivered within 24 hours. This unmatched fulfillment capability continues to be a key differentiator, anchoring JD’s leadership in reliability and customer experience.

JD Food Delivery has become a powerful growth engine, boosting both user acquisition and cross-selling. Daily orders have peaked at 25 million, supported by more than 1.5 million merchants and 150,000+ full-time riders, marking JD’s most successful new-business expansion since JD Health.

JD Logistics revenue grew 17% YoY, fueled by its expanded global footprint of over 130 warehouses across 23 countries. New facilities in the U.S., UK, and France, coupled with initiatives like JoyExpress in Saudi Arabia, underscore JD’s international ambitions. The company plans to introduce 1,000+ international brands via JD Super over the next three years, reinforcing its cross-border commerce ecosystem.

JD Health continues to scale rapidly, expanding into telemedicine, AI-driven prescription management, and rare disease treatment, diversifying the company’s healthcare footprint beyond e-pharmacy.

Meanwhile, Quarterly Active Customers (QAC) surged over 40% YoY, with shopping frequency climbing at a similar pace, exceeding 50% among JD Plus members, highlighting strong engagement and retention.

JD’s book value per share has remained above $19 billion since 2020, yet the stock has trended downward over that period, suggesting a significant disconnect between intrinsic value and market sentiment.

- $ACHR's cash soars to $1.7B** after $850M raise in Q2'25, ensuring strong runway for eVTOL development and commercialization. 🚀

- LA 2028 Olympics picks Archer** as exclusive air taxi provider, backed by White House Executive Order for U.S. eVTOL dominance. 🏅

- UAE Launch Edition takes off**: Midnight aircraft delivered, flight tests started, commercial payments expected in 2025. 🌍

- Production ramps up**: 6 Midnight aircraft in build, 3 in final assembly, FAA certification on track across Silicon Valley & Georgia facilities. 🛠️

- Defense program accelerates**: Acquired Overair patents & Mission Critical Composites assets, eyeing $13.4B Pentagon budget. 🛡️ $ACHR

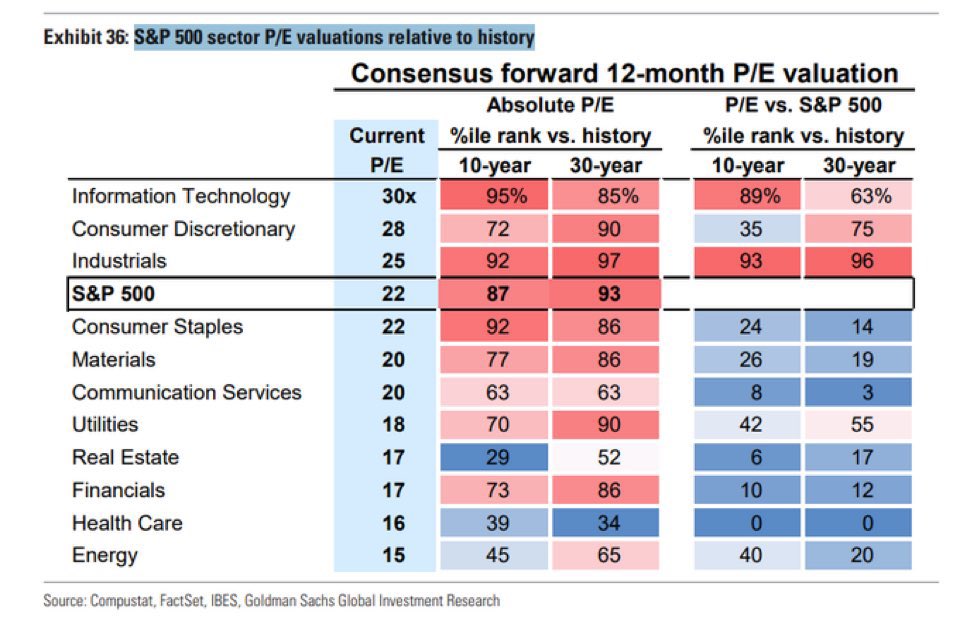

Healthcare is the only S&P 500 sector that is cheaper than both 10-year and 30-year averages according to Goldman Sachs.

That is an extremely attractive risk reward profile.

$UNH $OSCR $CI $ELV

15 NAMES UNDER $15B TRYING TO RIP APART THEIR INDUSTRIES

1. $TEM -- transforming diagnostics with AI

2. $OKLO-- compact nuclear energy

3. $ACHR -- replacing short-haul flights with eVTOLs

4. $ASTS -- replacing cell towers with satellite

5. $HIMS -- disrupting primary care & prescriptions

6. $ENVX -- making batteries that last longer & charge faster

7. $NVTS -- modernizing power semis for AI & EV

8. $IONQ -- pushing quantum to replace classical compute

9. $NBIS -- building an alternative to Big Cloud

10. $OSCR -- rebuilding insurance with full-stack tech

11. $EOSE -- storing clean energy w/o using lithium

12. $LMND -- automating consumer insurance

13. $GLBE -- streamlining cross-border e-commerce

14. $PRME -- creating off-the-shelf cancer treatments

15. $WGS -- advancing whole genome diagnostics

$XPEV has 2x potential in my view.

I know Chinese stocks tend to face a lot of skepticism but I still like a clean setup when I see one.

From my perspective, $XPEV is likely still completing its correction. I’m eyeing the $17 zone as a key area of interest. If structure holds, the upside toward $52 becomes very real.

This is a fast-growing company with rising delivery numbers, improving fundamentals, and a technical structure that deserves attention.

Conviction means acting before it’s obvious. That’s why this is on my radar.

For anyone wondering — no, this is not the right time to buy $HIMS.

Don’t chase the moving train.

Your second (and likely final) chance will come.

FOMO is expensive. Patience is free.

If you're buying stocks without research, why bother—especially with speculative ones? I’m long on $ACHR not for current earnings (they’re pre-revenue), but for these reasons:

1. Order Book: Archer’s indicative order book is valued at over $6B for ~700 aircraft. This includes a $3.5B base (Feb 2024) and a $500M deal with Japan Airlines (Nov 2024), per company updates.

2. Partnerships: Strong ties with United Airlines, Stellantis, Japan Airlines, and a new Abu Dhabi consortium signal solid backing.

3. Defense Strategy: A Dec 2024 partnership with Anduril for hybrid VTOL military aircraft opens a new revenue stream, backed by $430M raised.

4. Progress: FAA Phase 4 certification is advancing, with no delays reported. Production ramp-up is set for 2026, targeting 650 units/year in Georgia.

5. Launch: Commercial ops are slated for Q4 2025 in the UAE, not “this year”—a realistic timeline.

Nothing here has faltered; they’re even accelerating production plans. Panic sell if you want—I’m holding through at least 2027.