Welcome to the captivating realm of crypto, where knowledge, inspiration, and a touch of wit converge in perfect harmony. Prepare to embark on a journey..

Something quiet happened at @ethena this month.

USDC inside the protocol went from $21M to $280M in 30 days. No new incentive program.

My read is that's smart money rotating into USDe exposure via USDC, not retail yield farming.

The more interesting move: USDTB went from $581M to $1.06B. USDTB is Blackrock's tokenized T-bill product. It's now sitting inside Ethena's collateral stack and it doubled in a month.

Total Ethena TVL: $5.52B, up 24.2% in 30 days. Quiet Monday. Not quiet for Ethena.

One year ago Morpho had $3.75B in TVL. Today it's $7.35B.

Aave had $27.22B one year ago. Today it's $13.95B.

My read on why: @Morpho runs permissionless credit markets. Curators build any market they want, lenders pick their own risk exposure, rates are set by supply and demand. @aave pools collateral and sets parameters by committee. One model gives users choices. The other gives them safety.

In a risk-on environment, safety loses to yield. That's what the data shows.

Aave still holds $13.95B to Morpho's $7.35B — the gap is wide. But the trajectories crossed a year ago and haven't looked back. If Morpho holds this rate, it closes within $2-3B of Aave TVL by end of year.

Down week. Didn't change what protocols are actually paying.

Two rates I'm watching this Friday.

@EmberProtocol on Ethereum: 12.52% APY on USDC, no emissions in that number at all. $38M in active deposits on DefiLlama.

Smaller pool than I'd usually feature but the yield source is real borrowing demand, not a rewards program.

@alturax on Hyperliquid L1: 17.5% on USDT0. $25.8M TVL. Newer chain. Yield is borrowing fees, not incentives.

Higher rate, higher concentration risk. That tradeoff is worth knowing before touching it.

Neither is a recommendation. Both are worth knowing.

Hyperliquid as a product is very good. I’m extremely bullish on it. The ecosystem around it, not so much.

USDH lasted seven months. Native stablecoin. Launched September 2025. 50/50 buyback flywheel. BlackRock reserves. Validator vote picked Native Markets over Paxos and Frax. Sunsetted May 14, 2026. Supply peaked near $100M. USDC on Hyperliquid hit $5B in the same window. Coinbase took the USDC treasury role. The native stablecoin thesis is over.

HIP-3 sounds healthy on paper. $3B in 30-day volume across builder-deployed perp DEXs. Around 17,650 unique traders. Then you look at where it sits. https://t.co/GgvTt0KSxv holds 90%+ of HIP-3 open interest. 23 of the top 30 builder pairs are tokenized stocks and commodities. All one operator. Permissionless markets right now means one builder shipping.

The HIP-3 oracle is capped at 1% movement per tick. Safety design choice. It also means fast-moving or discontinuous markets (sports, niche prediction, anything with gap risk) can’t function under the constraint. Jsquare flagged this in January. Nobody seriously discussed it since.

HyperEVM TVL sits around $1.5 to $2B. Looks healthy until you check composition. Kinetiq is HYPE staked as kHYPE. It makes up 90.4% of Pendle’s HyperEVM TVL. HyperLend, Felix, Hyperbeat all run lending where HYPE is the dominant collateral. Hypurr was airdropped to early HYPE farmers. Floor tracks HYPE. The ecosystem isn’t diversified. It’s HYPE in different wrappers.

@HyperliquidX share of decentralized derivatives volume went from 80% in mid-2025 to 20% by late 2025. Aster took the volume. Lighter took the rest. The B2B pivot, “AWS for liquidity,” handed product velocity to third parties before any of them could carry it.

The product is very good. Top blockchain by fees. Billions in daily volume. Genuine PMF on perps. The ecosystem around it is a marketing layer wrapped around airdrop expectations. Most HYPE holders aren’t bullish on the apps. They’re bullish on HYPE and farming whatever season 3 turns out to be.

HIP-4 went live May 2. BTC binary contracts aimed at Polymarket. Zero fees to open. First thing the chain has shipped recently that could pull in users who aren’t already farming HYPE. Until that proves out, what counts as the ecosystem here is one builder doing 90% of the work.

Name one app on Hyperliquid that survives if HYPE goes to zero.

So @megaeth just shut down Terminal in week 3 of a planned 8-week season.

Third operational failure in six months.

The pre-deposit in November broke so badly the team refunded $500M and called it “sloppy.” The TGE on April 30 opened at $0.22, now trades at $0.08. Down 63% from ATH in three weeks while the broader market sits roughly flat.

The macro excuse doesn’t hold. MEGA is down 12.7% this week. Comparable L2s are down 2.9%. Protocol-specific underperformance, not sector weakness.

TVL went from nearly $600M post-TGE to $89M. Almost all of it was USDm yield-chasing capital that showed up for the rewards and now has a reason to leave with Terminal cut short.

88% of the 10B supply hasn’t unlocked yet. KPI-tied vesting helps in theory, but only if the network actually hits the milestones. With incentives getting restructured instead of expanded, that’s a real question now.

My stance only changes if Terminal’s Rabbithole successor ships and retains users without new bonus emissions, TVL holds above $200M for 30+ days organically, and the team stops cancelling programs they just announced.

Until that happens, the supply overhang alone caps any recovery.

The @LayerZero_Core exodus is now $4B in one week.

I'm Bearish on LayerZero's institutional position over the next 3-6 months.

My stance only changes if: verified independent validation AND a major protocol returns. Neither has happened.

@Lombard_Finance moved $1B in Bitcoin-backed assets to @chainlink CCIP. LBTC and BTC.b, across Solana, Ethereum, and Berachain. That follows Kraken's $3B migration earlier this week. Coinbase moved $7B last year. Kelp DAO, Solv Protocol, and Re have also exited. Four billion dollars in 72 hours from a single trigger event.

Lombard's reasoning: independent node operators, built-in rate limits, burn-and-mint architecture. This is an operational decision after a security review, not a panic exit.

The 2023 Multichain collapse followed the same arc one exploit, then a migration wave. That took weeks to unfold. This is moving in days. The pace gives LayerZero less recovery time between announcements.

Protocols still on LayerZero have a decision to make. Each new announcement makes that decision easier to justify in one direction.

Lido TVL is down 4.27% today. $20.14B. That's the biggest single-day move of any major protocol in a session where everything is red.

ETH is down 2.82%. BTC down 2.27%. Total DeFi TVL off 1.36%. Lido is moving roughly twice as hard as the broader market.

ethereum:0x5a98fcbea516cf06857215779fd812ca3bef1b32 is down 0.53%.

Yesterday LDO was up 3.45% while Lido TVL was falling 1.63%.

Today the TVL drop is accelerating and LDO is barely moving with it.

Renzo is at $198M now down 43% in seven days so some of the liquid staking outflow is category-wide, not just Lido.

Ethereum hit a monthly ATH in transactions last month. It didn't make anyone's feed.

April 2026 was the worst month for DeFi hacks on record $577M drained, mostly by Lazarus. Kelp/LayerZero blame war, Aave in federal court, Strategy floating a BTC sale, North Korean hackers accounting for 76% of the year's losses was all over the timeline.

Meanwhile: 48.7 million transactions on Ethereum in April. ATH. ETH price holding at $2,370. TVL rebuilding to $85.9B.

The CFTC just told non-custodial developers they don't need to register as brokers. And they're writing it into law.

In March, Phantom received a no-action letter. It can connect users to regulated derivatives perpetuals and event contracts without registering as an introducing broker. The CFTC's position: building a non-custodial interface is not operating as a financial intermediary. The software routes. It doesn't hold.

This week, the agency said it's cementing that stance into formal rulemaking. Non-custodial developer protection not as a favor, as a rule.

This matters for every protocol building front-end access to DeFi. The regulatory floor just got defined. The CFTC is not treating non-custodial software as a regulated business. It's treating it as software.

so @zachxbt has released 53 pages of tracing more than 90 million dollars over a DEX.

romance scams, trafficking, investment fraud, the Chinese underground markets in 2022 and 2023 57 to 60 percent of any Tokenlon swaps in 2022 and 2023. Named addresses. Named flows. Over $90 million.

The answer given by Tokenlon: "We do not hold user funds. The transactions are publicly verifiable. Both accurate. It is not the defense, but the problem.

Chain analytics firms charge governments millions of dollars each year for precisely this ability. The report was complimentary. The result was the same.

The counterargument will be that imposition will require time that regulators will eventually pick up. These flows were cross-border, China-related. All jurisdictions to which the report was sent had no powers to act on it. That is not delay. That is the architecture.

On-chain transparency is not a negative incentive. It is a ledger. The ledger must have a person with a sense of jurisdiction, authority, and institutional will so as to transform data into consequence. This lay in the open. ZachXBT found it. The infrastructure was designed to work and it has done so.

Nothing moved.

Aave V3 just posted its first green 7 day since the Kelp DAO exploit. +1.86%. $14.08B TVL. @aave

A few things worth knowing here:

• Wasabi Protocol: $5M+ drained April 30 wasabideployer.eth held sole ADMIN_ROLE no multisig, no timelock. Malicious contract upgrades hit Ethereum, Base, Blast, and Berachain. Berachain told users to withdraw immediately. @wasabi_protocol

• Carrot shut down the same day Drift exploit fallout. Withdrawal window open until May 14.

• April closed at 28 exploits, $635M total AAVE down 0.27%. TVL holds. Buyback pause is live.

Watch Solana TVL Carrot's window is open and contagion is still moving.

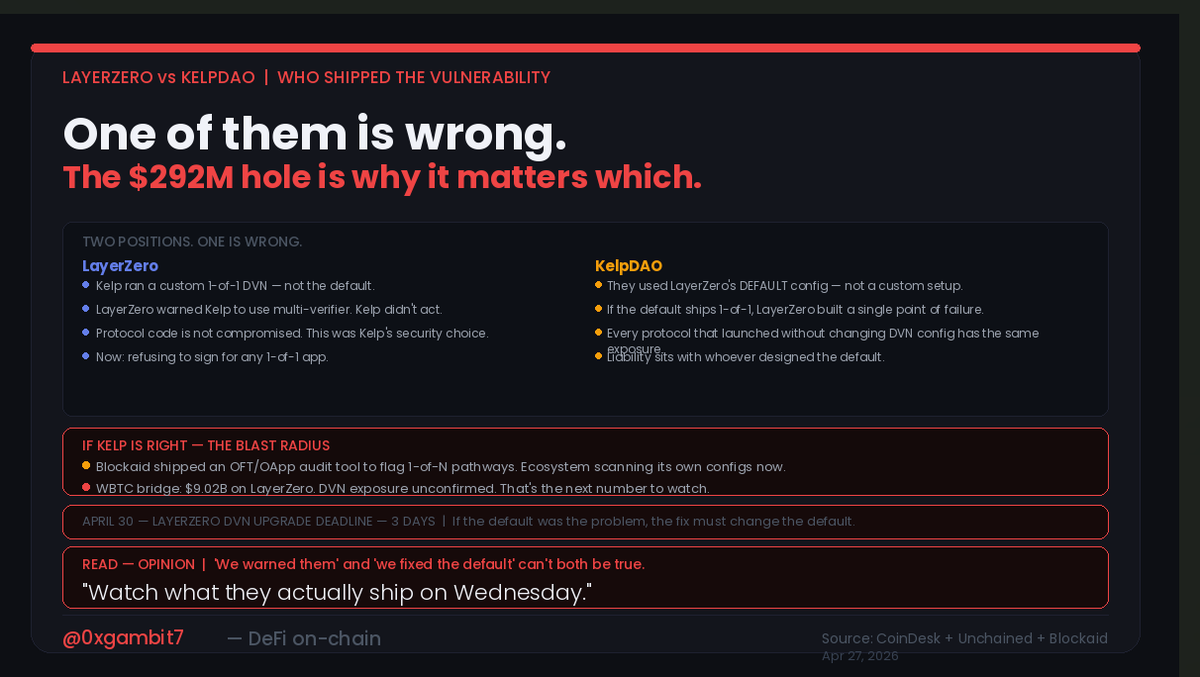

Kelp says they used LayerZero's default config. LayerZero says they didn't.

One of them is wrong.

A few things worth knowing here:

• LayerZero's position: Kelp ran a custom 1-of-1 DVN single verifier, single point of failure. LayerZero warned them to switch to multi-verifier. They didn't move. Now refusing to sign messages for any 1-of-1 app.

• Kelp's position: That was the default. Not a custom setup. If true, every protocol on LayerZero that launched without touching DVN config carries the same exposure.

• Blockaid already shipped an OFT/OApp audit tool flagging 1-of-N pathways. The ecosystem is scanning its own configs right now.

• April 30 LayerZero's self-imposed DVN upgrade deadline. 3 days. If the default was the problem, the fix needs to change the default not bury a warning in the docs.

So even if LayerZero ships Wednesday, "we warned them" and "we fixed the default" can't both be true.

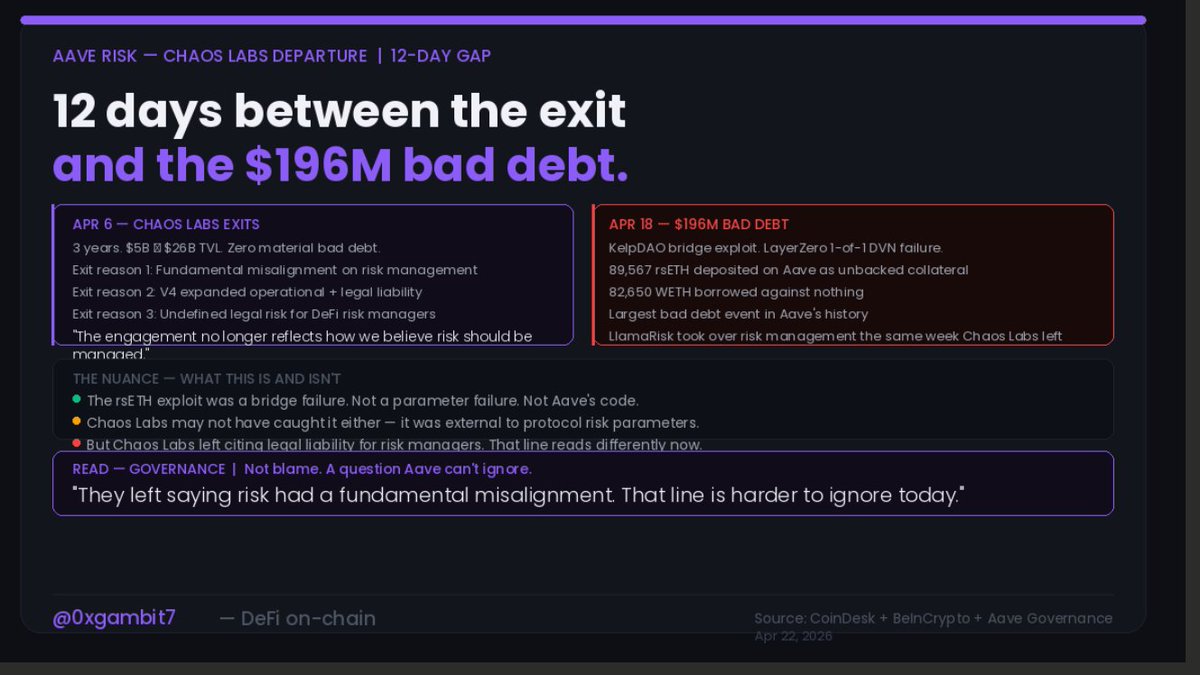

Chaos Labs managed Aave's risk for 3 years.

$5B to $26B TVL. Zero material bad debt.

They left April 6. Said there was a "fundamental misalignment on risk management." Said V4 expanded operational and legal liability in ways they weren't willing to absorb. Said the engagement no longer reflected how they believe risk should be managed.

12 days later: $196M bad debt. Largest in Aave's history.

The nuance is important. The rsETH exploit was a bridge failure LayerZero's 1 of 1 DVN. Not a parameter failure. Not Aave's code. Chaos Labs may not have caught it either. That's an external risk.

But they left citing legal liability for DeFi risk managers. That line reads differently today.

LlamaRisk took over the same week Chaos Labs walked. They inherited a protocol at $26B TVL with zero runway to stress-test the handover. Whether that had anything to do with what happened April 18 nobody can say cleanly.

3 years. Zero bad debt. 12 days after they leave: $196M. The timing is what it is.

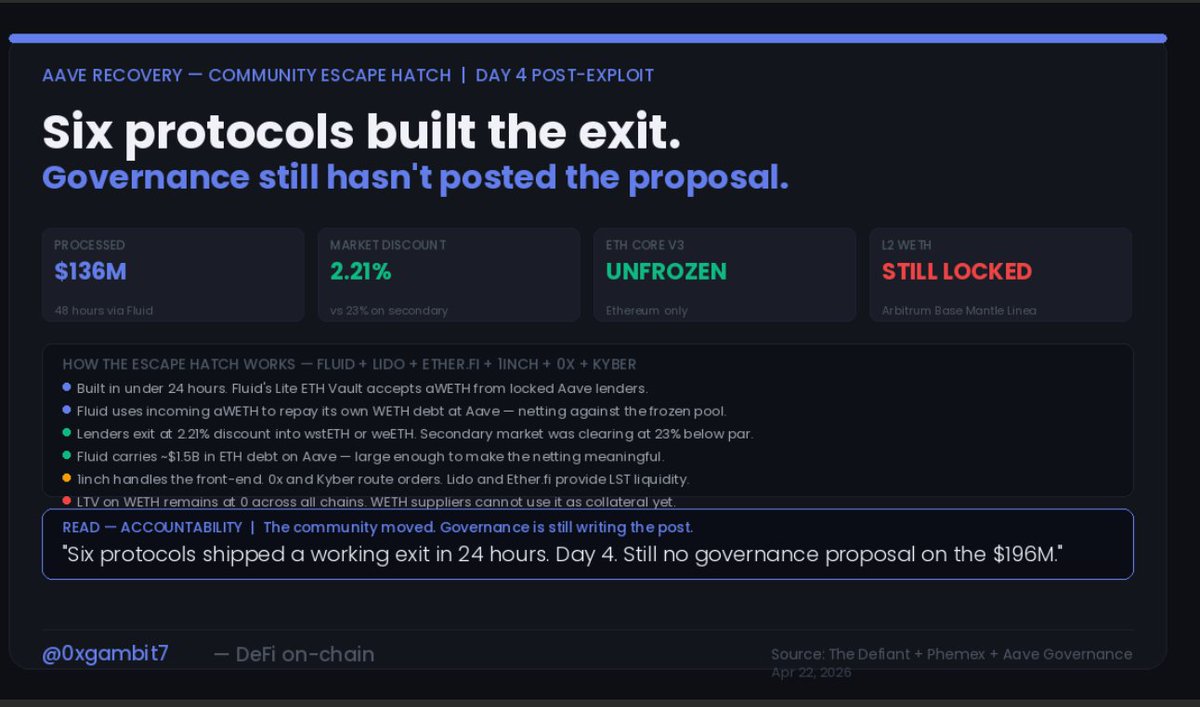

Aave's WETH pool hit 100% utilization April 18. Governance said they'd explore paths. That was 4 days ago.

In the meantime, six protocols built the exit.

Fluid launched an aWETH Redemption Protocol in under 24 hours. Lido, https://t.co/sEFfIa8JJN, 1inch, 0x, and Kyber plugged in. Here's how it works: you hand Fluid your aWETH, Fluid uses it to repay its own WETH debt at Aave, and you get wstETH or weETH out the other side.

The pool shrinks. Your position unlocks. Exit cost: 2.21% discount. Secondary markets were clearing at 23% below par. $136M processed in 48 hours.

Fluid carries roughly $1.5B in ETH debt on Aave. That size is what makes the netting work.

Ethereum Core V3 WETH is now unfrozen. L2s Arbitrum, Base, Mantle, Linea still locked. WETH LTV is still 0 across all chains. Not over.

The community solution was live before the governance proposal existed.