1/ 🧵 $CNTN raised "$545M" via PIPE in November 2025 — but 85% was in-kind $CC tokens, not cash. Only ~$80M was real dollars.

The real story is how many CC tokens are sitting in that treasury. Let me break it down. 👇

Some large US players want to liquidate $MSTR, very concentrated selling via TWAPs but it ain't working, $BTC will have another +1.00% candle at the US close

Too many people expecting more downside on $BTC, max pain is a short squeeze while $NQ pumps back fueled by shorts opening, adding more fuel to the fire before down again

@Tokenoya Won't happen at 50bps trading fees, if you wanna purchase in large volumes you OTC buy them from large holders (Super Validators from the early days) or OTC buy them from LP's, MMs - ETF product like these have a timely limited availability and solely attracts retail, 50 IQ funds

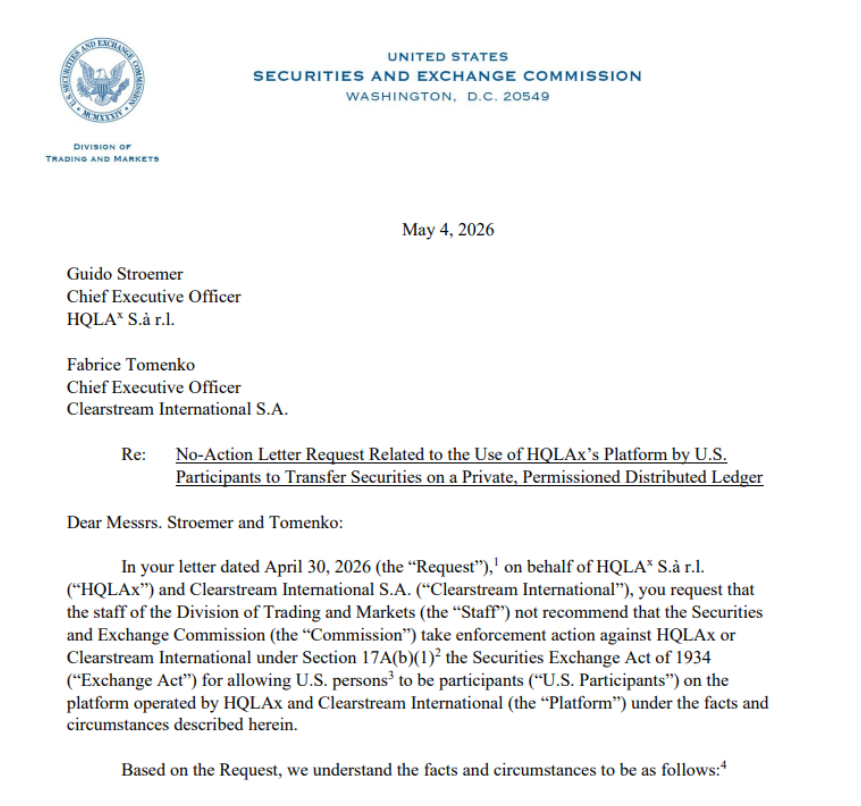

SEC just issued No-Action Letter for HQLAˣ + Clearstream

HQLAˣ migrating from R3 Corda to Canton Network $CC after fresh investment from Broadridge + Digital Asset.

Deutsche Börse owned Clearstream’s D7 DLT utilizing Canton DAML for tokenized securities & collateral mobility.

Green candle therapy happening on $CC.

$CC remains a misunderstood protocol backed by TradFi giants building their public, permissioned Blockchain as a settlement layer for the tokenisation of any financial asset.

Largest asymmetrical bet in the space.

@EricBalchunas The audacity to charge 50bps while BTC and ETH ETFs are around 20bps, low volume, spreads, yada yada - enjoy the fees as long as it lasts, competition prices products like $TCAN quickly out

@LeilaniFarms Dilution runway is much bigger than $300M. CNTN filed a $2B shelf (S-3) in Jan 2026 — only ~$390M used so far. ~$1.6B still available.

SV yield: weight 4 (escrowed, milestone-dependent), earning ~15-20M CC/yr (~$2.3-3.1M). CIP-0105 locks 70% — under $1m liquid at current prices

@LeilaniFarms CNTN holds SV weight 4 (escrowed, milestone-dependent) out of an estimated ~100-130 total SV weight across 13 validators. Post-halving, the SV pool earns ~ CNTN's share is roughly 15-20M CC/year (~$2.3-3.1M at current prices). CIP-0105 locks 70%, leaving only ~$700K-900K liquid/y

Cash investors paid $3.075/share for a treasury where the in-kind CC was marked at double spot — how is that not getting screwed?

Fully diluted ~211M shares. mNAV: ~$2.50. Stock at $3.17 = 27% premium.

**UPDATE: 10-K is out.**

$CNTN holds 3.34B $CC (fair value $502M) and $17M cash as of Dec 31, 2025.

Cost basis: ~$524M → implied avg acquisition price of ~$0.157/CC. That's 2x+ the $0.06-0.09 spot at PIPE close. In-kind contributors valued their CC at a significant premium.

6/ 🎯 The Catalyst

Q4 10-Q drops early April (est. April 3-10). First time actual CC holdings get disclosed.

That number — 6B or 13B — changes everything. Expect volume.

Watch for it. 👀

1/ 🧵 $CNTN raised "$545M" via PIPE in November 2025 — but 85% was in-kind $CC tokens, not cash. Only ~$80M was real dollars.

The real story is how many CC tokens are sitting in that treasury. Let me break it down. 👇

5/ 📈 Why This Is Bullish

Even at the conservative 6.6B CC estimate, that's a massive token position locked inside a NASDAQ-listed vehicle. mNAV sits around ~$3.40 — stock at ~$3.17. Almost no premium priced in.

If CC reprices higher, every $CNTN share benefits.

---

4/ 🤔 Why Does The Valuation Matter?

Shares were fixed at $3.075. The CC valuation only changes how many tokens went into the treasury.

Lower CC price = more tokens per share = fatter treasury for all shareholders. The 10-Q will reveal which end of the 6-13B range we're at.

2/ 💰 The Cash vs In-Kind Split

~$80M came from actual cash investors — likely ARK, Broadridge, Tradeweb, Kraken, Clear Street, Polychain.

The other ~$465M? CC tokens contributed by DRW, Liberty City, Digital Asset, and ecosystem insiders. All shares issued at $3.075.