The official cost of acquisition ratio gives us a clear baseline for what the company considers each scrip to be worth:

1. Vedanta Ltd (Residual): 52.34% (Rs 405/share)

2. Vedanta Oil and Energy: 21.49% (Rs 166/share)

3. Vedanta Power Limited (Power vehicle): 12.23% (Rs 95/share)

4. Vedanta Aluminium Metal (VAML): 7.15% (Rs 55/share)

5. Vedanta Iron & Steel (VISL): 6.79% (Rs 52/share)

@Nagar9887Nagar@equities_samjho share gira tha par tushar ji ka conviction nai gira tha. you could have make 3x had u bought the shares when it came around 5k

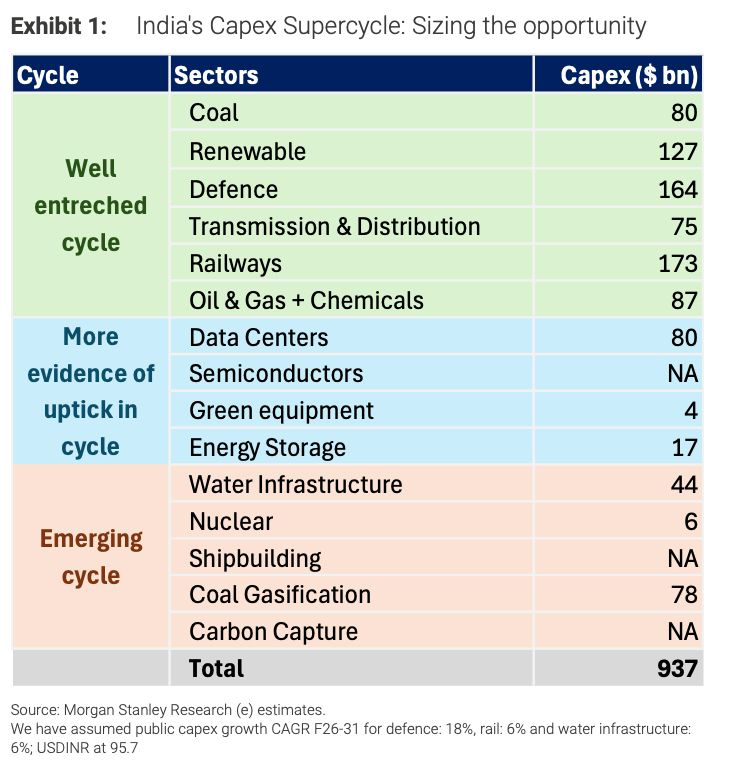

India's investment rate is expected to go from 34.6% of GDP today to 37.5% by FY30.

Last time such a capex cycle was seen in 2004-08 period but the nature of capex this time is completely different

And one can divide this into 3 buckets -

1) Well-Entrenched (money already flowing): Coal, Renewables, Transmission, Defence, Railways, Oil & Gas

2) Uptick Evidence (gaining momentum): Data Centers, Semis, Green Equipment, BESS

3) Emerging (early innings, high optionality): Nuclear, Water, Shipbuilding, Coal Gasification, Carbon Capture

Coal is not a legacy constraint. India hit a peak demand record of 271 GW on May 21, 2026 for the 4th consecutive all-time high. Thermal anchored the grid at ~63% of generation. At night, ~190 GW of coal ran at near-full capacity with shortages still touching 5.4 GW. NTPC is adding 13 GW. BHEL and L&T are reporting record order inflows.

India added a record 44.6 GW solar + 6 GW wind in FY26. Impressive. But CERC's new Deviation Settlement Mechanism (Apr-26) is quietly ending the "Must Run" free pass for RE generators. By 2031, solar/wind will face the same grid scheduling penalties as coal plants. Standalone RE is dead. RE + Storage is the only viable model going forward. Every new project will need BESS embedded.

BESS could be the defining investment theme of India over the next decade. Battery costs down 70% in 3 years. 117 GWh tendered cumulatively. CEA targets 80 GW by FY36. India is still 90% import-dependent on China for the battery value chain. One needs to check up on how the value chain gets created.

The HVDC cycle is just starting. RE generation is concentrated (Rajasthan: 119 GW, South India: 106 GW). Demand is everywhere else. ±800 kV HVDC = 6 GW bulk transfer over 1,000–2,000 km. India needs 120–130 GW across ~22 corridors. Current installed: ~18 GW. That's a 6x scale-up. Combined CEA + Brahmaputra Basin capex = Rs14.3 trillion in transmission alone. GE Vernova, Hitachi Energy, Siemens Energy sit at the centre of this (Around them is a big value chain that is there). India has no fully integrated domestic HVDC OEM yet.

Nuclear the structural shift is real this time. SHANTI Act passed. 60-year state monopoly dismantled. FDI up to 49% allowed. PFBR achieved first criticality in April 2026 India entered Stage 2 of its nuclear programme. Target: 8.8 GW today → 100 GW by 2047. ~$200bn cumulative opportunity. Maharashtra alone signed nuclear MoUs worth Rs6.5 trillion with Reliance, NTPC, Adani, and others.

L&T targeting 3x nuclear revenue in 5 years. BHEL can currently supply 30–40% of a nuclear plant's bill of materials.

Also semiconductor ecosystem is getting created. 6 months ago this was all policy announcements but Micron ATMP inaugurated. Kaynes OSAT running. CG Power scaling. Tata-ASML MoU signed for Dholera fab (28nm–110nm nodes, 50,000 wafers/month). First sellable wafers expected: late 2026. India's semis market: $25–30bn today → $ 110bn by 2030. ISM 2.0 launched.

And then there is the DC boom that is coming to India. India's installed DC capacity: 1.8 GW → 10.5 GW by FY31 (AI: 6.8 GW, non-AI: 3.7 GW). Microsoft: $ 17.5bn. Google-AdaniConneX: $ 15bn. AWS: $ 15.3bn combined. Reliance-Brookfield-Digital Realty JV: $ 11bn. ~$75bn announced in 5 years. Hyperscalers are treating India as a geopolitical hedge which has stable democracy, growing digital market, coal baseload + RE mix. Power systems alone = $ 20bn opportunity for industrials.

This isn't a government-funded capex cycle hoping private capital shows up.

Corporate debt/GDP: 52% (vs 61% pre-pandemic). Industrial credit growth: 15% YoY. Bank NPAs: 2.5% at multi-year lows. Gross FDI: $ 94.5bn in FY26, +17% YoY.

Private capex to grow at ~16% CAGR through FY31. Investment rate peaks at ~37.5% of GDP.

Source - Morgan Stanely

#SME#AFCOM#AfcomHoldings

Afcom Holdings Q4 & 12M FY26 Concall Highlights

👉 FY27 & Future Outlook

▫️ Revenue Guidance:

💠With fleet expansion, FY27 revenue expected to be much more than double FY26 levels on a conservative basis (actual likely higher as capacity increase >2x).

💠 Management: “On a conservative estimate also … it will be much more than double.”

💠 FY26 achieved ₹587.72 Cr with essentially 2 aircrafts operating at high utilization

▫️ Wide-body (B777) Economics:

💠Each B777 expected to deliver ~3x revenue of a current 737-800 (conservative estimate).

💠 Based on 14-15 rotations/month, long-haul sectors (10-12+ hrs), ~75% load factor.

💠 Full 4 wide-bodies + 5 narrow-bodies = 9 aircraft fleet targeted by mid-next calendar year (H2 CY2027).

▫️ Demand & Yield Outlook:

💠Regional air cargo demand structurally growing.

💠Middle East disruptions provided temporary boost in Q4 & early FY27; even after normalization, rates expected to settle higher than pre-crisis levels (post-COVID analogy).

💠 Focus remains on yield per kg and revenue per trip rather than pure volume.

💠 Current utilization ~81% gross weight; scope to improve further with more capacity and balanced charter/regular mix.

▫️ Cost & Margin Drivers:

💠 ATF fully passed through (100%) via fuel surcharge — no margin dilution expected.

💠 Designated Indian Carrier status delivers 5-7% overall operating cost reduction (VAT exemption on ATF in Tamil Nadu + other statutory benefits) — full benefit to reflect in FY27.

💠 EBITDA margins expected to stay healthy; further upside possible from scale and efficiency.

▫️ Cash Flow & Balance Sheet:

💠Operations turned cash flow positive (~₹36 Cr in FY26).

💠Receivables controlled (~60 days on recent billings, zero >6 months outstanding).

👉 Current Projects & Future Pipeline

▫️ Fleet Expansion (Immediate Pipeline):

💠 4th & 5th narrow-body (B737): On the way; to be operational before next quarter (Q1 FY27).

💠Deposits paid; fully funded. Minor customs/other expenses covered from internal resources.

▫️ Wide-body B777 (4 units):

💠Financial closure completed via QIP (₹199.85 Cr raised).

💠Timelines: At least 2 by end of calendar 2026; at least 1 operational by end of FY27 (conservative).

💠Full fleet ramp targeted H2 CY2027.

💠 3rd aircraft already operational (fresh off C-check; reserved for contracted flying starting end of June 2026).

▫️ New Routes & Network Expansion:

💠 Dubai World Central (DWC): Successful inaugural freighter flight — strengthens UAE/Middle East connectivity.

💠 Nauru Air Corporation (Republic of Nauru): Strategic alliance signed; foray into Australian & Pacific region countries. Multiple MOUs executed for diversified opportunities.

💠 Noida Airport: Afcom to be the first cargo aircraft to land at the new cargo terminal (inauguration ~June 17, 2026). Plans to start Delhi international operations (major gateway) + Mumbai.

💠 Existing network (ASEAN, Sri Lanka, Maldives dry-lease, Middle East) to be augmented with additional transshipment hub flights.

▫️ Capacity & Contracted Flying:

💠 High demand environment — “we are short of capacity; every additional kg will be fully utilized.”

💠 Q4 saw 415 pure charters out of 602 total trips (surge due to disruptions). Contracted flying lined up for new aircraft.

💠 Selective order intake to maintain balance between charters and weight-based cargo while protecting yields

👉 Other Notable Points

▫️ Operational Metrics FY26:

💠1,923 trips | 24,353 tons handled

💠 Avg yield: $2.54/kg | Cost: $1.58/kg

💠Q4 yield improved to $2.72/kg despite higher charter mix.

💠 Chennai airport international cargo growth (12.5%) 2.3x national average — Afcom major contributor.

▫️ Awards & Recognition (FY26):

- Top Airline by Air-to-Air Import 2026 – Velana Awards (Maldives)

- Freighter of the Year 2026 – Velana Awards

- Fast Growing Cargo Freighter of the Year 2025 – 6th ACE Awards

▫️ Capital & Compliance:

💠₹199.85 Cr QIP successfully completed (26.3 lakh shares @ ₹759.72) — fully earmarked for fleet expansion.

💠No further fundraise required for planned 9-aircraft fleet.

💠IND-AS transition completed; all mainboard compliances in place.

▫️ Key Q&A Takeaways:

💠 Fleet funding: Fully covered for 4th/5th narrow-bodies + 4 wide-bodies via QIP + internal accruals.

💠ATF impact: 100% pass-through confirmed; Designated Carrier benefit (5-7% cost saving) already partially visible in March and will fully kick in FY27.

💠Utilization & Charters: Higher charter mix in Q4 helped asset rotation during disruptions but slightly impacted overall weight utilization (one-way charters). Focus shifting to balanced mix.

💠Post-disruption outlook: Demand remains elevated vs normal; sea freight also facing cost pressures — air cargo remains essential.

💠Forex & Billing: >60% revenue in USD.

💠 Competition & Moat: Service excellence, flexibility, new routes, and Designated Carrier status as key differentiators