Let me get this straight -

$GOOG just limited $META usage of Gemini due to limited capacity

Meta signed $48B of deals with $CRWV and $NBIS

And suddenly people are saying that Meta has excess capacity?

Seems like Meta wants to get their valuation up before diluting…

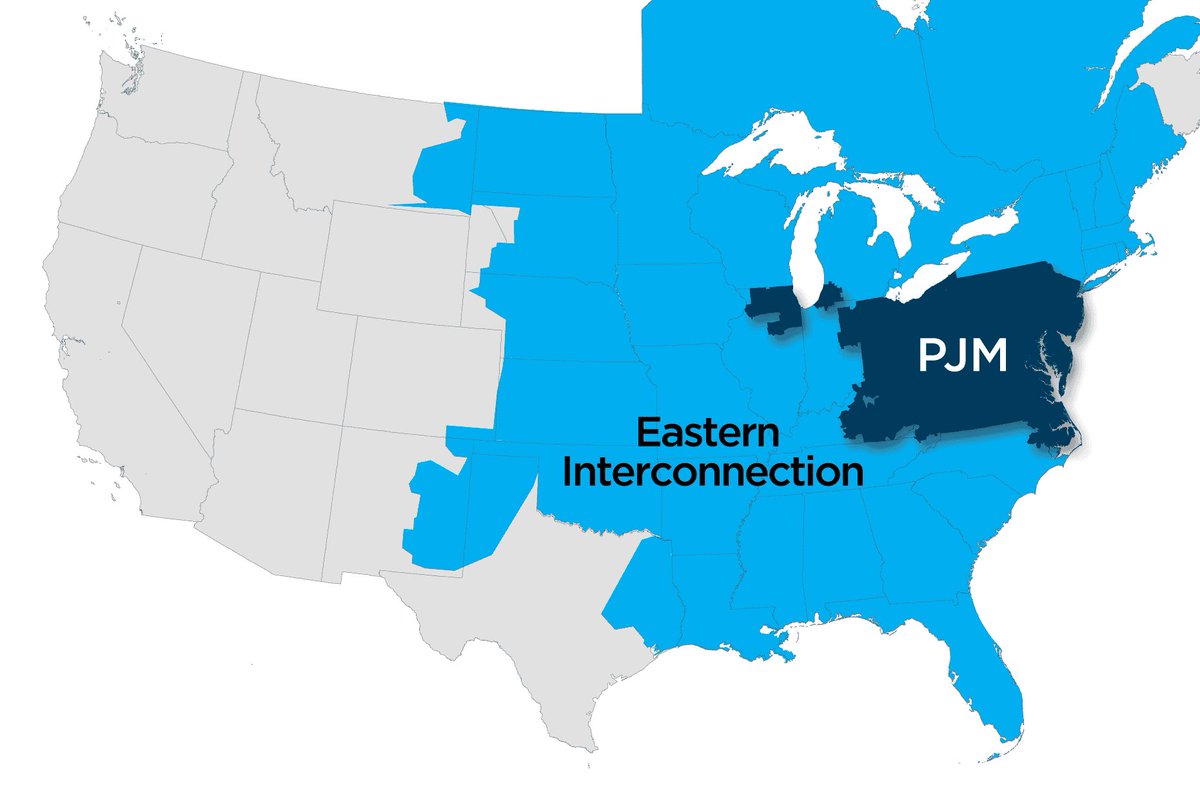

PJM, the grid operator covering Virginia and D.C., faced a formal emergency order from the Department of Energy amid extreme heat and tight capacity from recent data center expansions.

The order allows for temporary pollution-limit waivers to avoid blackouts.

The first large scale emergency of many. The grid needs expanding.

$ECG $MYRG $CAT

Based purely on fundamentals, $SEZL remains the highest quality BNPL firm, as well as potentially one of the best fintech choices in the market.

Granted, quality doesn’t matter when no matter the company, the industry sees persistent drawdowns on a daily basis.

Lots of people talking about "hyperscalers will reduce 2027 capex to protect their FCF/share price".

Does being the hyperscaler that admits defeat to the other hyperscalers in this AI race really create favorable sentiment for the stock?

I would argue no.

Obviously there may be oversupply down the line, but no matter how much money these memory makers dump right now, supply will be low until minimum 2028. Fabs just take too long to build.

Bunch of people freaking out about this - isn’t this exactly what you’d expect? Why would companies not take advantage of this multi year demand, now backed by more and more contracts.

$MU $DRAM

📢 𝐉𝐔𝐒𝐓 𝐈𝐍: Samsung to unveil KRW 1,000 trillion (about $650bn) 10-year South Korea investment plan - $MU $SNDK $STX $WDC $NVDA $AMD

Samsung will unveil on the 29th at the Blue House a KRW 1,000 trillion (about $650 billion) investment blueprint over the next decade for semiconductors, AI data centers, secondary batteries and displays — a package Samsung says consolidates planned capex across its core businesses and equals roughly half of South Korea’s GDP.

Samsung is considering about KRW 300 trillion for semiconductor fabs in the Gwangju–Jeollanam‑do area, aligned with the government’s plan for a second southwestern semiconductor cluster; Samsung Electronics chairman Lee Jae‑yong conveyed the proposal to President Lee after a meeting on the 25th.

$KXIAY is $SNDK but a few months behind. Eventually that gap will close and the share price will catch up.

All a matter of time. All things considered I think Kioxia is still relatively unheard of.

Kioxia is rapidly emerging as one of the most leveraged ways to play the AI infrastructure buildout beyond the usual GPU names.

JPMorgan’s report highlights a point that many investors still underestimate: AI is not just a compute story. It is increasingly a storage story. Every AI model requires vast amounts of data to be stored, retrieved, indexed, cached, and processed. As inference workloads scale, the amount of NAND flash and enterprise SSD capacity required grows alongside compute demand.

The investment case rests on three powerful forces converging simultaneously. First, AI is driving a structural shift toward higher-value enterprise SSDs. Kioxia expects data center demand to grow from roughly 30% of total NAND demand today to around 50% by 2028. This is important because enterprise SSDs carry significantly better economics than consumer storage products. The mix shift alone can drive margin expansion even before considering industry pricing.

Second, Kioxia is benefiting from technological leadership. The transition to BiCS Gen 8/10 should lower cost per bit while supporting higher-performance products optimized for AI inference workloads. JPMorgan expects the enterprise SSD mix to rise from 34% in FY2025 to 67% by FY2028, creating substantial operating leverage.

Third, the company sits directly in the AI infrastructure stack through products such as KV Cache storage, high-performance AI SSDs, and ultra-high-capacity drives designed for inference clusters. As models become larger and context windows expand, storage increasingly becomes a bottleneck alongside compute and networking.

The numbers are remarkable. JPMorgan now forecasts roughly 160% EPS CAGR over the next three years and has raised its price target from ¥80,000 to ¥155,000. Revenue is expected to increase almost eightfold between FY2026 and FY2029 while EBITDA margins approach 80%.

More importantly, this reinforces a broader investment theme we have discussed repeatedly: AI beneficiaries extend far beyond NVIDIA. The market initially focused on GPUs, then networking, then memory. The next layer is storage. Every token generated by an AI model ultimately depends on data being stored and retrieved efficiently.

The biggest risk remains the same risk facing every semiconductor cycle: overinvestment. NAND has historically been one of the most cyclical industries in technology because periods of strong profitability often trigger aggressive capacity expansion. JPMorgan explicitly identifies future oversupply as the key downside risk.

Nevertheless, the report reinforces our long-standing view that AI infrastructure remains significantly broader than the market appreciates. GPUs receive most of the attention, but storage, memory, networking, power infrastructure, and data centers are all becoming critical bottlenecks. Kioxia sits at the intersection of several of those trends.

In many ways, AI is creating a new hierarchy of infrastructure. First came compute. Then networking. Then memory. Storage appears increasingly likely to be the next major beneficiary.

Feels like $CRWV is one company that gets a government investment if/when the government decides to invest in AI companies.

*The* American compute company with a massive backlog working with Nvidia, OpenAI, Anthropic, Meta, Google, etc.

If the government takes stakes in AI companies, they’ll likely select important American companies that need the capital. Given the debt situation here you could say they need it.

They’re much more critical to the AI ecosystem than most people think.

If CoreWeave blows up it’d be trouble for the AI trade. Everyone knows about their debt, the government showing support would likely ease a lot of the fears surrounding the company.

Slightly disappointing ER from $PPIH this morning. EPS came in quite low due to Middle East project uncertainty.

More importantly though, backlog has increased, primarily driven by new AI-related projects in their new Ohio facility.

AI-related rerate thesis is still in play.

$PGY CEO Gal Krubiner just bought ~250k of $PGY stock on the open market, with an average price of approximately $15.10

Seen so many people say - "if the valuation is so low, why isn't management buying"

Now we have an answer. They are.

Why are so many accounts talking about buying $IBM at the open tomorrow morning because of what Trump said about the company?

That clip was from December 10th last year.

$HPS.A has done me well since my entry on the breakout.

Prior to adding a bit more, cost basis was around $215.

Added a few days ago seeing that volume is still quite low, even after the run up. There is still more room to run.