MicroStrategy has hacked the debt markets.

They're borrowing $8.2 BILLION at 0% interest while everyone else pays 5%. How? They're selling volatility disguised as bonds - turning their own chaos into free money. This is financial engineering at its most unhinged 🧵

$chwy "low tens of millions" in ai efficiencies, but no clear roi or rev boost, just "structural efficiency" gains, sounds like spend with unclear payoff

https://t.co/QTbBoI9hH5

#AI#AIbubble

CHWY just reported Q1'26 — and Wall Street is already calling it "cautious".

Here are the 3 things from the call the Street is sleeping on:

1/ THE SLEEPER STORY: They quietly downgraded their own product initiatives mid-quarter

2/ Consumer softening hit late Q1, but CHWY maintains 7.5% EBITDA margins while adding 200k customers

3/ Modern Animal acquisition masks underlying deceleration in their core clinic strategy

Full Call Sheet + Delta Sheet + my grades (Disclosure B- / Financial Quality B): https://t.co/q0zhSBYE9p

What's your biggest takeaway — Is the $290M combined clinic revenue target at steady state a margin trap or a moat builder? Drop it below. $CHWY

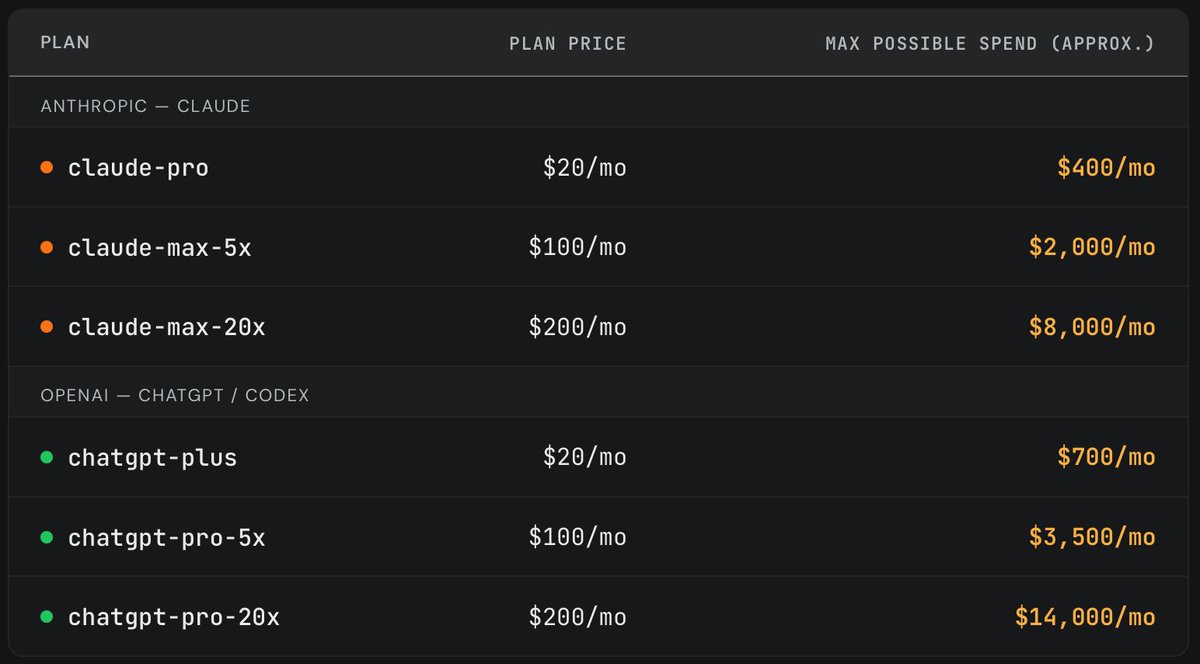

Recently, we purchased one of each Anthropic/OpenAI subscription plan and randomly ran long horizon coding tasks until we exhausted the weekly limit. It's widely believed that a $200/month plan maxes out at ~$2000/month worth of tokens (assuming API pricing). However, we found that the subscriptions are actually far more generous. (2/4)

$WSM: BOTTOM LINE is #AI conversion - Olive driving checkout at 'high multiple of site averages' while everyone fixates on tariff noise. The obvious headline is 4.8% comp acceleration, but the real signal is furniture trends accelerating significantly from Q4 - this is the #housingcycle inflection. The binding constraint isn't demand or supply chain (they're crushing both) - it's their ability to scale AI productivity gains fast enough to offset tariff margin pressure. Laura's most revealing quote: 'We're becoming an AI-fueled company' not just deploying tools. My view changes if they start quantifying AI impact with specific conversion rates and cost savings rather than qualitative multiples.

$WSM Q1'27 — What You Missed

1/ #AI is quietly becoming a conversion machine while everyone obsesses over tariffs - ‘We’re becoming an AI-fueled company’

2/ 4.8% comp acceleration masks the real story: furniture is back

3/ They stopped giving B2B pipeline specifics and pivoted to 'awards' talk

https://t.co/Lc9CAWa00P

anthropic: $24bn of A2 notes priced at 5.75% yield, $6bn of A1 notes at 1% over treasuries, $4.5bn of junior debt at 8.5%

https://t.co/CMLhvCE6Io

#credit#AI

$panw lots of ai hype, but no clear roi or spending control, just "significant investment" and "r&D acceleration

https://t.co/K5WhsO4Tsk

#AI#AIbubble

$VEEV: veeva's approach to ai in life sciences. "We're not making AI tooling. We're actually agentic labor to solve the problem. We are the believers in simplification and standardization of the industry, and that's how the industry will grow and Veeva will grow along with it." - Peter Gassner

🔴 $TJX insider sale

Ernie Herrman (CEO & President)

sold 67,551 shares at ~$158.29 avg — $11M

tjx ceo sells 67,551 shares in routine transaction

https://t.co/2quXjqdFVC

#insidertrading#stocks#investing

$dollargeneral lots of ai hype, still "early in our ai journey" with no concrete progress or roi to show, just vague plans to "accelerate investments

https://t.co/TYuVEIgzlZ

#AI#AIbubble

$MDT: medtronic's strategy to lead in the electrophysiology space. "Now through innovation, purposeful investment and global execution, we plan to completely surround the electrophysiology space and offer patients and physicians a more complete, end-to-end set of EP solutions." - Geoffrey Martha

PANW just reported Q3'26 — and Wall Street is already calling it "execution".

Here are the 3 things from the call the Street is sleeping on:

1/ Hardware business quietly having its best decade on AI data center demand

2/ CyberArk integration running 3-6 months ahead of schedule on profitability

3/ Prisma AIRS tripled customer count to 300+ but they're still not giving unit economics

Full Call Sheet + Delta Sheet + my grades (Disclosure A- / Financial Quality B+): https://t.co/BjPqkxxkcs

What's your biggest takeaway — Is the 40% hardware growth a structural AI data center cycle or a cyclical refresh that reverses when component costs normalize? Drop it below. $PANW

$ulta lots of ai hype, not much on spend or roi, "'early days'" indeed, still waiting for proof it's more than just a buzzword

https://t.co/Tdu0oFGxNY

#AI#AIbubble