China’s urban renewal 15th FYP sparks a rally in A-share real estate stocks. Urban renewal generally means higher steel-to-cement ratios psm than greenfield builds ie bullish for iron ore demand if it scales. $BDI #DryBulk#IronOre

US-China grains deal isn’t signed, and volume was announced by the US, not China. Need firm delivery obligations to materially shift trade flows. Brazil’s record crop and cost advantage will favor Brazil-to-China shipments.

https://t.co/Ctff8DUq1E

China’s U.S. soybean buys are a positive, signaling potential Panamax/Handy upside on U.S.–Pacific routes. Treat it as a bullish trigger, not a trend shift (yet). #drybulk#FFA#shipping

https://t.co/RoSfpVJhMO

The upcoming China coastal weather pattern acts as a short-term stabilizer, especially Nov/Dec FFAs. Expect temporary congestion-led firmness, likely marking the end of the correction phase and start of a short rebound window into early Nov. #drybulk#shipping#FFA

BHP still quietly selling iron ore into China even after CMRG’s warning. Reminds me how often sentiment and reality diverge in this market. Ore still moves when the price is right.

Capes likely to ease into late Oct as recent momentum fades, with a short correction expected in early Nov before stabilizing and turning higher mid-month. Dec should find support near 25k. #Capes#Drybulk#FFA#Shipping

Market’s calling Vale’s Q3 inventory build (4.5 Mt) a potential positive freight signal. I’m not convinced as this pattern recurs frequently as production peaks and cargoes sit in transit. Classic seasonal build, not demand surge #Vale#Drybulk#Shipping#FFA

After the sharp drop, Capes are stabilizing near key support. Next catalyst: China weather disruptions from Oct 17 may squeeze Pacific tonnage if port delays rise. Temporary rate support possible. Watch congestion + front-loading risk. #Shipping#Drybulk#FFA

US-owned, China-built ships now exempt. On paper, clear. In practice, messy. Enforcement’s self-declared, no checks. Ports = judge + jury.

✅China-built ships → clear

✅Repairs → clear

❌Ownership chains, territories, control → not clear

Basically: interpret at your own risk

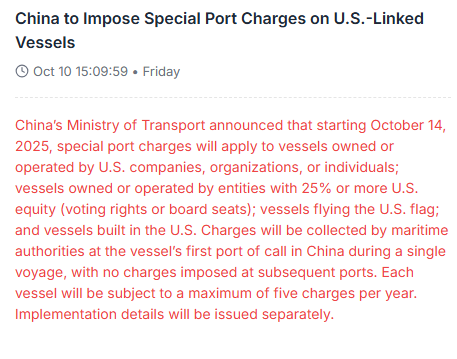

China’s new port charges on US-linked vessels will accelerate US–China maritime decoupling, raise freight costs, and shift trade flows toward non-US tonnage.

A gradual drift lower is likely to persist over the next few days before stabilizing into mid-Oct. With strong winds forecast in North China from 17 Oct, Capes might see a meaningful recovery attempt as weather disruptions tighten the prompt balance. #Shipping#Capesize#Drybulk

After the recent washout, the Capesize market is staging a technical rebound today but doesn’t seem to be a full-fledged trend reversal. With ballast supply increasing and Brazilian maintenance looming, the recovery is likely to be short-lived, fading by mid-Oct.

China’s ban on all BHP cargoes looks mostly symbolic or a negotiation tactic. Though a short-term drag on freight, it could be resolved by end of Golden Week. #Shipping#Capesize#FFA

China’s freeze on BHP iron ore cargoes may reduce Pacific Capesize demand near-term, but could boost ton-mile if mills pivot to Brazil, adding fresh volatility to freight.

Trade: short Oct vs long Nov FFA spread is working out well #Shipping#Drybulk#Capesize

From founders to fall guys? Jens Jacobsen’s exit seals the end of Costamare’s legacy. Cargill’s ‘tie-up’ looks more like a hostile coup. My bet? They scooped $CMDB at fire-sale prices as this bulker play is sinking fast while Cargill laughs to the bank. #Shipping#Drybulk

Early Oct faces clear downside risk from Golden Week, ballasters and Brazil maintenance. A brief post-GW bounce may fade quickly. Early Nov could inherit Oct weakness but Vale’s unfinished CoAs could open room for upside surprises later. #Capesize#Drybulk#Shipping#FFA