Many think they are high risk takers - hence deserve high returns. But many fail to you understand the real meaning of Risk - "Permanant Loss of Capital". And it pinched hard when you really lose money.

And for those who imagine of making big money in #Crypto, is better to learn from others mistake before diving in.

#SEBI Investor Survey 2025, indicating the HIGH risk tolerance levels among Indian households is just 5.6%

Majority of Indian investors (79.7%) prioritize the safety of their money over higher returns. And only 14.7% fall are willing to accept some risk for better returns.

Just like grading through classes from LKG to +2, retail investors need to start with simple mutual funds like liquid funds, short term funds, conservative hybrid funds, then elevate to variety of equity funds before directly experimenting with riskier assets.

Are you a long term investor...

Do you want to make money work for you?

Then here's is an article for you...

https://t.co/Fc0ppgWhKu

#LongTermInvesting#MutualFund#sip

𝗧𝗵𝗲 𝗿𝗮𝗯𝗯𝗶𝘁, 𝘁𝗵𝗲 𝗱𝗲𝗲𝗿 𝗮𝗻𝗱 𝘁𝗵𝗲 𝗺𝗮𝗿𝗸𝗲𝘁 𝘁𝗶𝗺𝗶𝗻𝗴 𝘁𝗿𝗮𝗽

Our hunter-gatherer ancestors had to balance two instincts, protect what they already had, and take a chance to improve their future.

Investors face the same dilemma every time markets look expensive.

Do you hold on to the rabbit already in hand? Or do you put it down and chase the deer?

Market timing promises a magical third option.

This week’s Truth Be Told column in @bsindia #BusinessStandardlooks at why that promise is so tempting, and why it can hurt more than it helps.

Article link:https://t.co/ktpBmvdlAh or read the column given below.

#TruthBeTold #MarketTiming #InvestorBehaviour #FinancialPlanning #PersonalFinance

@saurabhsmittal@securingLives

Utpal Seth on Rakesh Jhunjhunwala’s bet on Metro Brands.

He made 300x returns on this private investment.

“We invested in Metro brands because of it’s discipline on inventory management, the sales per Sq. Ft., the gross margins and the profit after tax as percentage of sales was exceptional.”

“Only the growth rate was not high but we realised that if growth changes, the multiples could be very different.”

“Management team was also open to understand, benchmark and learn. And hence, we made 300x returns in it.”

- Utpal Seth.

Discl: Stocks discussed are not a recommendation. Please consult a SEBI/SEC regd. advisor

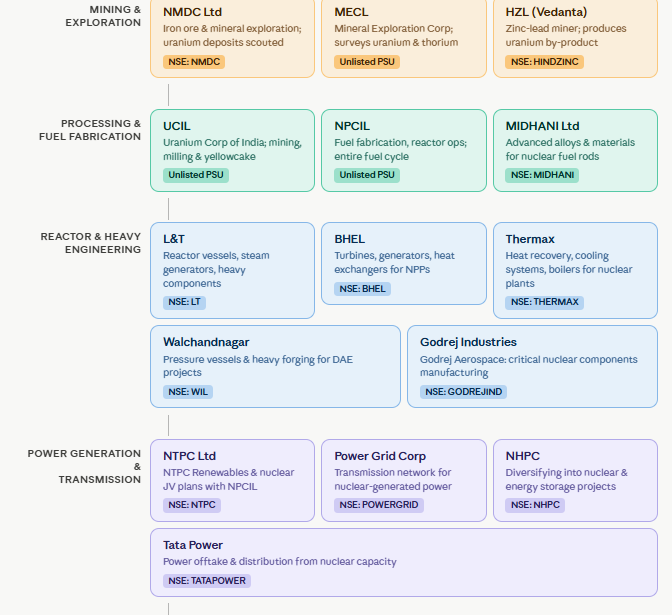

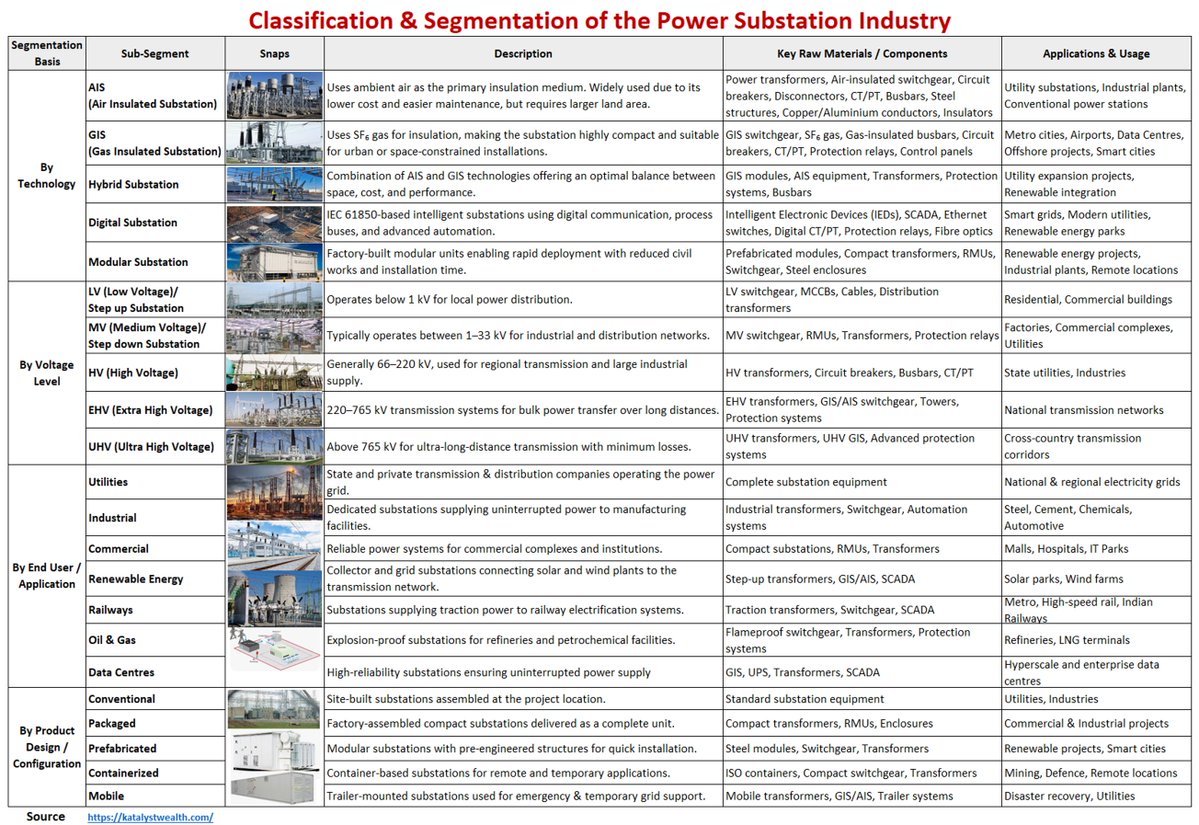

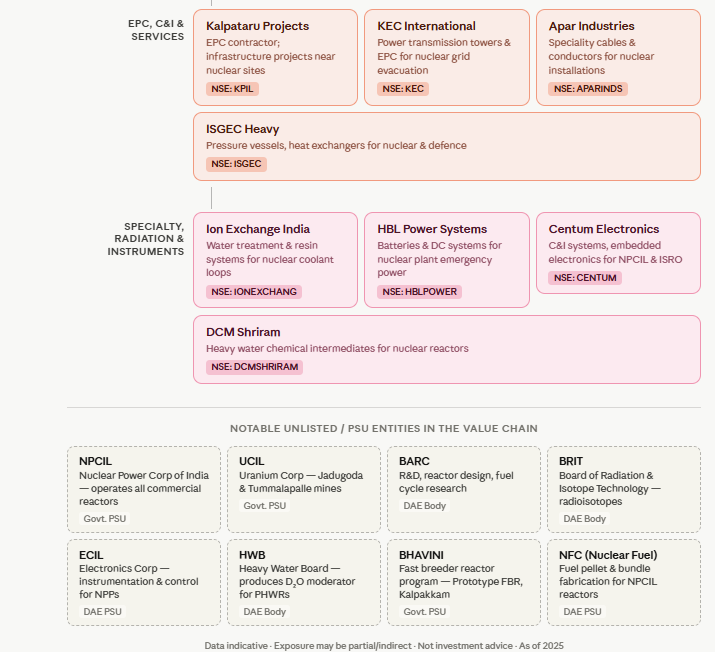

Electricity doesn't travel directly from Power plant to your home

It passes through one of the most critical parts of the power ecosystem: Electric Substations

Electric Substations are the silent backbone of India's energy transition and a major investment opportunity

(1/n)

#Seminconductor is the Buzz word.

But, then how to understand the semiconductor value chain in broader level right from Quartz to Chip application.?

Here is one small effort from my side, putting together all those links in a easy to understand, for retail investors.

Reweet🙏

The beauty contest called investing

My Paisanomics column in the Mumbai Mirror.

Investing isn't just about finding the best asset. It's about guessing what everyone else will want to buy next.

That's the beauty contest economist John Maynard Keynes described nearly nine decades back.

As Keynes put it, markets are driven by what "the average opinion expects the average opinion to be."

In the age of WhatsApp, Telegram and financial influencers, that game spreads faster than ever.

Bitcoin. Crypto. Gold. Silver. Small caps. F&O. Online money games. Even SIPs.

When "everyone's doing it" becomes the investment thesis, prices can overshoot, valuations drift away from fundamentals, and future returns suffer.

The crowd can make you money for a while. It can also take it away just as quickly.

The hardest part of investing isn't finding the next winner – it's resisting the temptation to chase whatever everyone else already loves.

https://t.co/MRHdhbCUDG

Gr8 visual on how UPI works. And the numbers behind it are staggering.

Transaction volume grew from 2 crore in FY17 to 24,162 crore in FY26, a nearly 12,000x jump. Value rose from ₹0.07 lakh crore to ₹314 lakh crore, over 4,000x.

Phenomenal ! Only India could have done the technological pole vaulting .

Most investors sell their best compounders way too early. They see “fair value” in their mind and exit lock, stock, and barrel. Do NOT sell merely because something is fairly valued. Why?

As a great business compounds earnings and scales, it attracts big institutional money. Their required rate of return is much lower than yours. They happily pay higher multiples → your “fairly valued” stock keeps running. This is literally how multi-baggers are made after the initial re-rating.

Combine the 4 zones with Reverse DCF, instead of building a dreamy DCF to justify the price. Use reverse DCF — not to justify the price, but to interrogate whether the market’s embedded expectations can realistically come true.

Ask: “Under what conditions would the market’s current expectations actually come true?” If those conditions look unrealistic → you’re probably in Zone 3 or 4.

Liquidity and Interest rates are the gravity that pulls all these zones. When rates rise and liquidity dries, the zones shift left, and that's the time to sell.

Some practical aspects of invetsing and portfolio construction

Model 1: Use AI like a Ferrari, not autopilot

AI is incredibly powerful for retail investors — but only if you respect its limits.

• Data cleaning is 80% of the work (don’t dump raw 600-page PDFs)

• Create a curated “binder” document first

• Make the model confirm it understood context

• Run 4-5 LLMs as a “council” playing devil’s advocate

• Then apply human judgment, experience & justification.

AI narrows the search dramatically. It does not replace thinking.

Model 2: Ruthlessly eliminate 99.5% of stocks first. There are 4,000+ listed companies. You only need ~20 high-conviction ideas.

Eliminate top-down on fragility, leverage, stressed promoters, anything outside your competence or time horizon. This removes ~97% of the universe.

Then go deep, not wide. Missing some gems is a feature, not a bug. The science ends at 97-98%. After that, qualitative judgment (promoter behavior, runway, treatment of minorities) takes over. Investing is the last liberal art.

Model 4: Prepare for asymmetric bets (don’t try to predict).

You cannot predict black swans. But you can prepare. Best asymmetric opportunities appear when frightened or leveraged sellers are forced to sell (2008, 2020).

• Map the full range of outcomes + probabilities

• Seek disconfirming evidence (when you like a company, read only the bad reports)

• Do a pre-mortem before investing

• Fix a ruthless sell trigger in advance

• Keep a “tenth man” in your process

Downside should be finite and knowable. Upside can be open-ended.

Model 5: Portfolio construction & temperament. Concentration is powerful but behavioural, not scientific.

• Barbell: ~80% in 7-8 stable core compounders (sleep-well-at-night) + ~20% in 10-12 small optionality bets

• Only 16-18 genuinely non-correlated ideas are enough

• As your capital base compounds and you have more to lose → become more conservative (he now leans 20:80 instead of 80:20)

Invest bottom-up, but always worry top-down.

These 5 models work together: AI helps you process information faster →Ruthless filtering reduces noise →

Valuation zones + reverse DCF keep you disciplined →

Asymmetric bet thinking protects capital → Barbell portfolio + temperament lets you stay invested through cycles.

The goal isn’t to be right on every stock. It’s to build a process where good things happen more often than bad ones over decades. The biggest edge in investing today is not more information. It’s better filters, clearer mental models, and stronger temperament.

https://t.co/0etO30hyb0

Research suggests that re-reading with a highlighter is nearly useless.

So I pulled together 63 techniques that actually move the needle, ranked by how much each one improves retention.

These protocols can help anyone whose work depends on absorbing, remembering, and using information every day.

Full guide in the newsletter.

(1/4)

Equity Returns Estimates for FY27

2000 to 2024: P/E multiples went from 11x to 22x. EPS Growth: 9% CAGR. Equity Returns: 12% CAGR. Now P/E cannot go from 22x to 44x. So, equity returns must be solely funded by EPS Growth.

PE Expansion Era Is Over

a. PPFAS Rajeev Thakkar told ET: “People must get accustomed to lower equity returns now.” Why is the seller himself saying: “My product is no longer attractive?”

b. From 2000 to 2024, Indian equities delivered 12% CAGR returns for two reasons:

(1) EPS Growth was 9% CAGR; and (2) PE multiples doubled from 11x to 22x because investors were betting on India growth story. (So, doubling of the multiple roughly added 3% CAGR on top of EPS Growth of 9% CAGR.)

c. Now that engine of PE expansion cannot run again because there is no mind-blowing India growth narrative anymore. So, going forward, equity returns must be funded almost entirely by EPS Growth (plus dividend yield) alone.

Equity Returns Formula

Total Equity Return = EPS Growth + PE Multiple Change + Dividend Yield

EPS Growth =

Corporate Earnings Growth

PE Multiple Change =

PE Expansion or Contraction

(What multiple the investors are willing to pay per rupee of earnings)

Nifty EPS Growth in FY27

FY25: Est 15%; Actual 3.4%

FY26: Est 12%; Actual 4.5%

FY27: Estimated 8.5%

Note: 8.5% is Bank of America (BofA) estimate, which is the most trusted.

Dividend Yield for Nifty 50 = 1.20% (historic low)

Total Equity Return in FY27

SCENARIO 1: BULLS ARE RIGHT

EPS Growth: 11%

(Beats BofA estimates)

PE Change: 0%

(Nifty PE stays 22x)

Dividend Yield: 1.2%

Total Equity Return = EPS Growth + PE Multiple Change + Dividend Yield

= 11% + 0% + 1.2%

= 12.2%

SCENARIO 2: BASE CASE

EPS Growth: 8.5%

(Matching BofA estimates)

PE Contraction: -1.5%

(Mild downward PE revision)

Dividend Yield: 1.2%

Total Equity Return:

= 8.5% - 1.5% + 1.2%

= 8.2%

SCENARIO 3: BEARS ARE RIGHT

EPS Growth: 4%

(Below BofA estimates)

PE Contraction: -10% (not 10x)

Dividend Yield: 1.2%

Total Equity Return =

= 4% - 10% + 1.2%

= -4.8% (Negative Return)

Equity Risk Premium (ERP)

ERP is the additional gain (compared to fixed income) for bearing the financial risk + psychological stress of investing in a volatile asset.

Is it Worth the Pain?

BULL CASE

Equity Return: 12.2%

Less LTCG: 12.5%

Net Return: 10.68%

FD return: 7%

Less Tax: 30%

Net Return: 4.9%

ERP = 10.68% – 4.9%

= 5.78%

BASE CASE

Equity Return: 8.2%

Less LTCG: 12.5%

Net Return: 7.18%

FD return: 7%

Less Tax: 30%

Net Return: 4.9%

ERP = 7.18% - 4.9%

= 2.3%

Strategy for Retail Investors

a. If you are a bull, it is worth going 100% into equities because the Risk Premium (Extra Gain) is 5.78% over & above FDs, which will strongly compound over time.

b. If you believe the base case, then a small risk premium (extra gain) of 2.3% may not be worth the pain if you are investing for less than 5 years.

Over a long period, this small premium will also compound. But for below 5 yrs horizon, the pain-reward ratio looks poor.

c. For bears and believers in the base case scenario, it may be best to diversify into gold, FDs, and selective equities.

Gold can give superior returns (than 2.3% CAGR). Cash can deliver life-changing returns if the market crashes and you are the only buyer in town.

d. Extraordinary returns can still be made in this market if you are a good stock researcher, and have the temperament to stay invested, come hell or high water. Most people overestimate their ability.

Endquote [Original]

A stock circulates on X after the money has been made. If you have found a stock on X, you have not discovered it. You have been introduced to it.

@arabicatrader

Many investors wonder which investment option to choose. While we generalize by saying - go by your risk profile - here is an article that is aimed at giving some clarity:

https://t.co/nPcPHV40mi

For more information - kindly reply message to 9944193339

#mutualfunds #indianstocks #pms

Day 173: FATCA (Foreign Account Tax Compliance Act)

Ever wondered why banks, mutual funds, and brokers ask you to complete a FATCA declaration?

FATCA is a global tax compliance framework introduced by the United States in 2010 to improve financial transparency and curb offshore tax evasion.

For investors, FATCA isn't about paying additional tax—it's about accurate disclosure and compliance.

✅ Mandatory during KYC

✅ Required for Mutual Funds & Demat Accounts

✅ Helps ensure global tax transparency

Understanding compliance is as important as understanding investments.

#FATCA #FinancialLiteracy #MutualFunds #KYC #TaxCompliance

Recently attended a fund manager meeting on pharma and health care sector.

Posted article on this sector and one of the ways you could participate in this sector...

https://t.co/uRSfTYml53

Some are good at giving lectures and writing books. Just like majority, they are good at postmortem analysis. And he is not alone. They are Fit to be tutors at some educational institution. Nothing beyond it. It is our mistake in glorifying them as stars. Let us celebrate/follow only those who walk the talk.

Very detailed perspective on impact on AI on IT services industry. I subscribe to this view. I think AI will create more opportunity for IT industry than risk. #narrative @TCS @nasscom @carnelian_asset