This week’s Weekly Market Commentary discusses how Middle East tensions have dominated markets since late February, with ongoing uncertainty offset by diplomatic progress that has supported equities while risks remain reflected in f https://t.co/X8tbhJy2AP

LPL’s Chief Economist Jeffrey Roach analyzes supply shocks as a result of the Iran conflict, potential Fed actions, and the roles artificial intelligence could soon be playing in the wider economy. https://t.co/Dk2aGi8Wg9

LPL Research provides Q1 2026 insights from the LPL Financial Coverage List to pinpoint where large cap equity managers are leaning into opportunity and risk. https://t.co/dXjk0LKNYv

This week’s Weekly Market Commentary discusses how investors can uncover opportunities by finding growth that the market does not fully anticipate, whether through attractively valued slow growers or faster-growing businesses whose https://t.co/hqYGX8DlUA

In this week’s Market Signals podcast, Adam Turnquist, Chief Technical Strategist, and Tom Shipp, Head of Equity Research, examine the market’s return to record highs through both fundamental and technical lenses. https://t.co/Y3u67z0zqU

This week’s Weekly Market Commentary discusses how U.S.-only fixed income portfolios are increasingly concentrated and that selectively adding global bonds—particularly emerging market debt and currency-hedged non‑U.S. developed bon https://t.co/ENwfLLLMKD

This week's Weekly Market Commentary discusses ongoing geopolitical risks stemming from strikes on Iran and the effective closure of the Strait of Hormuz, noting that while markets often recover quickly from conflicts, uncertainty r https://t.co/seHsOMQBlv

Geopolitical tensions surrounding Iran have increased market volatility, but history shows stocks often prove more resilient than they feel in the moment, especially when economic and earnings fundamentals remain intact. While today https://t.co/IbR5DyaVn0

LPL's Weekly Market Performance for the week of March 16, 2026, highlights the latest geopolitical developments, Fed decision, and global market headlines. https://t.co/NhXBAv7G3V

LPL's Weekly Market Performance for the week of March 9, 2026, highlights geopolitical developments, earnings, and commodity moves and their impact on markets. https://t.co/EaYHhznyyr

Most people think retirement success depends on how much money you’ve saved.

But there’s another factor that can matter just as much.

The order of market returns.

Two retirees can start with the exact same situation:

• $1,000,000 invested

• $50,000 withdrawn each year

• The same average market return

Yet one portfolio lasts… and the other runs out.

Why?

Because when you're withdrawing income, early market declines can have a lasting impact.

This is called Sequence of Returns Risk.

It’s one of the biggest risks in retirement planning that most people have never heard of.

I recorded a video discussing this risk and one way we help to mitigate it.

Check it out! 👇

https://t.co/19A7ot6UEa

The recent escalation in Iran has disrupted global energy markets, but history shows markets often recover quickly once conditions stabilize. Despite near‑term volatility, economic strength, supportive fiscal policy, and easing infl https://t.co/GDaAzpYask

💰 $1,000,000 doesn’t automatically make you a millionaire.

Not if a large portion of it still belongs to the IRS.

In my latest newsletter, I talked about a few planning moves you can make today that your future millionaire self will thank you for…

Things like:

• Building tax diversification

• Strategically harvesting capital gains and losses

• Using lower-income “gap years” to convert Pre-Tax Money

These strategies aren’t about chasing higher returns.

They’re about making sure more of what you build actually stays yours.

Because wealth isn’t just about the number in your account.

It’s about how much of it you get to keep.

If insights like these would be helpful for you, you can sign up for the newsletter below 👇

https://t.co/9tquVqoPEc

💣 Inherited IRAs can quietly become a tax nightmare.

I recently met with someone who inherited a sizable traditional IRA from a loved one.

They had done the responsible thing — they left the account invested and let it grow.

But there was one problem.

They didn’t have a withdrawal strategy.

Under current rules, most inherited IRAs must be fully distributed within 10 years. Every dollar that comes out of that account is treated as taxable income.

And here’s where it sneaks up on people.

If the account grows for several years and withdrawals are delayed, you can end up taking large distributions later, pushing yourself into much higher tax brackets.

Without a plan, it can start to feel like you're writing a massive check to the IRS.

But the good news is that this is very manageable with the right strategy.

Planning withdrawals across multiple years can help smooth out income and reduce tax impact. In some cases, we can also offset that income by:

• Increasing pre-tax contributions to your own 401(k) or IRA

• Using business deductions or retirement plans if you’re self-employed

• Coordinating withdrawals with lower-income years

The key is simple: don’t wait until year 8, 9, or 10 to start thinking about it.

If you’ve inherited an IRA and haven’t walked through a long-term withdrawal strategy, it may be worth taking a closer look.

A little planning now can save a lot of taxes later.

LPL Research’s Strategic and Tactical Asset Allocation Committee (STAAC) is pleased to provide our Capital Market Assumptions (CMA) and Strategic Asset Allocation (SAA) as of January 2026. The CMA and SAA provide guidance on longer- https://t.co/7Unl6170Sn

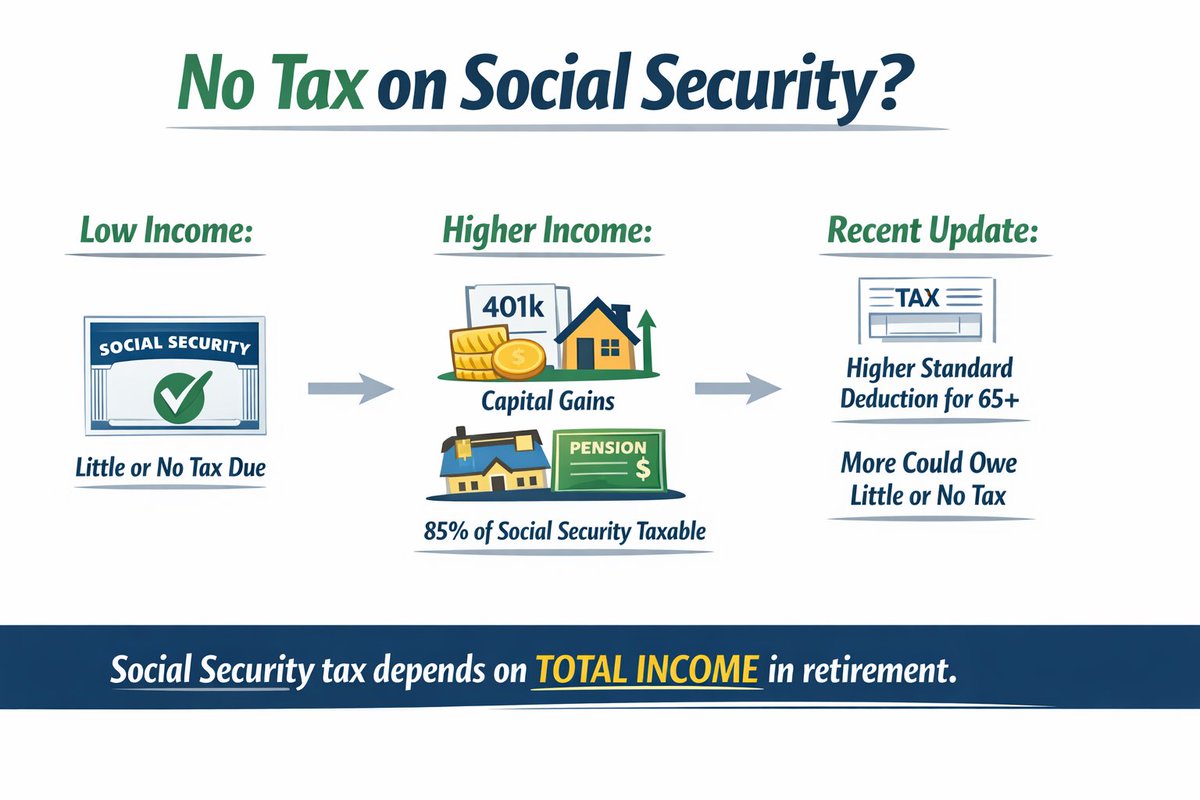

💬 “No Tax on Social Security.”

I recently heard someone describe this as a major “change.”

But that’s not entirely accurate.

There has been no fundamental change to how Social Security is taxed.

Social Security benefits are taxed based on your total income, not in isolation. They’re combined with other sources — like IRA withdrawals, pensions, and capital gains — and then applied to a formula that determines how much of your benefit becomes taxable.

Up to 85% of your Social Security can be subject to income tax, depending on your overall income.

For individuals living primarily on Social Security, it’s often true that little to none of it is taxed — especially after applying the standard deduction.

But for many retirees who are also:

Withdrawing from pre-tax 401(k)s or IRAs

Receiving pension income

Realizing capital gains

…it’s common for the full 85% of benefits to be included in taxable income.

So what actually changed?

Under the OBBBA, the standard deduction for individuals and couples age 65+ increased (depending on income). That means more retirees who live mostly on Social Security may owe little or no tax.

That’s a positive development.

But saying “No Tax on Social Security” across the board is misleading.

The better conversation isn’t about slogans. It’s about strategy.

With coordinated planning, we can:

Project how much of your Social Security will be taxable

Manage withdrawals to control income levels

Use Roth and non-retirement accounts to reduce tax exposure

Minimize Medicare premium surcharges

You may not control the tax formula — but you can control how your retirement income is structured around it.

And that’s where real value lives.

This week’s Weekly Market Commentary discusses LPL Research’s Strategic Asset Allocation (SAA), the long‑term framework that guides how diversified portfolios are built to deliver more stable outcomes across evolving market environm https://t.co/KXISJrUOBe

Advice tells you what to do. Planning tells you why.

“Max your 401(k).”

“Pay off your debt.”

“Invest more.”

Sounds responsible. Sounds smart.

But here’s the problem — advice doesn’t know your life.

It doesn’t know:

The stress you feel when cash gets tight

The dreams you have for your kids

The business you’re thinking about starting

The fear of making the wrong move

Advice is loud. Planning is personal.

Planning starts with questions like:

What matters most to you?

What keeps you up at night?

What kind of life are you actually trying to build?

Because money isn’t math.

It’s emotion. It’s security. It’s freedom.

You can follow all the right advice and still feel uncertain.

But when you have a plan — one built around your values and your reality — the noise gets quieter.

Advice gives direction.

Planning gives peace.