That been said, a potential reduction in middle distillates shipments to Europe following Houthi attacks in the Red Sea might help alleviate the tightness in Asia Pacific by keeping more supply within the region.

#OOTT#ESAIEnergy#RedSea

Due to scheduled maintenance in China, Japan, South Korea, and other Asian countries, refinery throughput will fall to 30.5 million b/d in the first half of 2024, before growing by 1 million b/d in the second half.

As a result, regional balance for middle distillates will tighten during maintenance. This will support ULSD spreads to crude in Singapore for the first half of 2023.

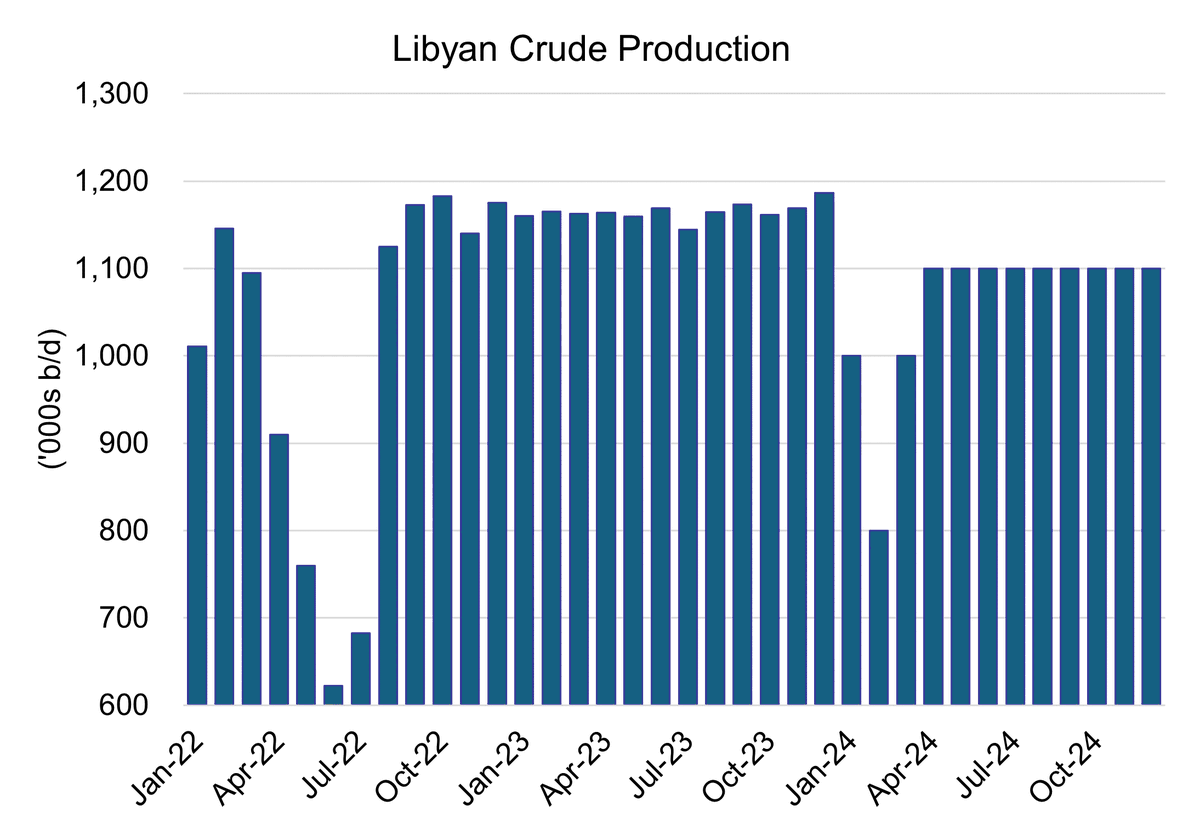

in Libya. Angola’s departure from OPEC raises questions about the group's cohesion. Meanwhile, the conflict in the Middle East risks escalating following the continued US strikes on Yemen.

#OOTT#ESAIEnergy#Libya#Angola#OPEC

Protestors in Libya, with possible backing from factions in the civil conflict, have shut down the Sharara oil field leading to a 300,000 b/d drop in crude production. A resolution with the protestors remains likely but the resurgence of conflict should never be ruled out

In December, China’s crude oil imports rose by 1 million b/d month-on-month to 11.4 million b/d. Our fundamental analysis suggest that China will require 11.3 million b/d of crude imports in 2024, just 100,000 b/d higher than 2023.

Moreover, heavy maintenance starting in the second quarter will pressure refinery throughput and lower crude imports. We expect crude imports in the first quarter to remain unchanged from the last quarter at 11.1 million b/d, before falling to 10.8 million b/d

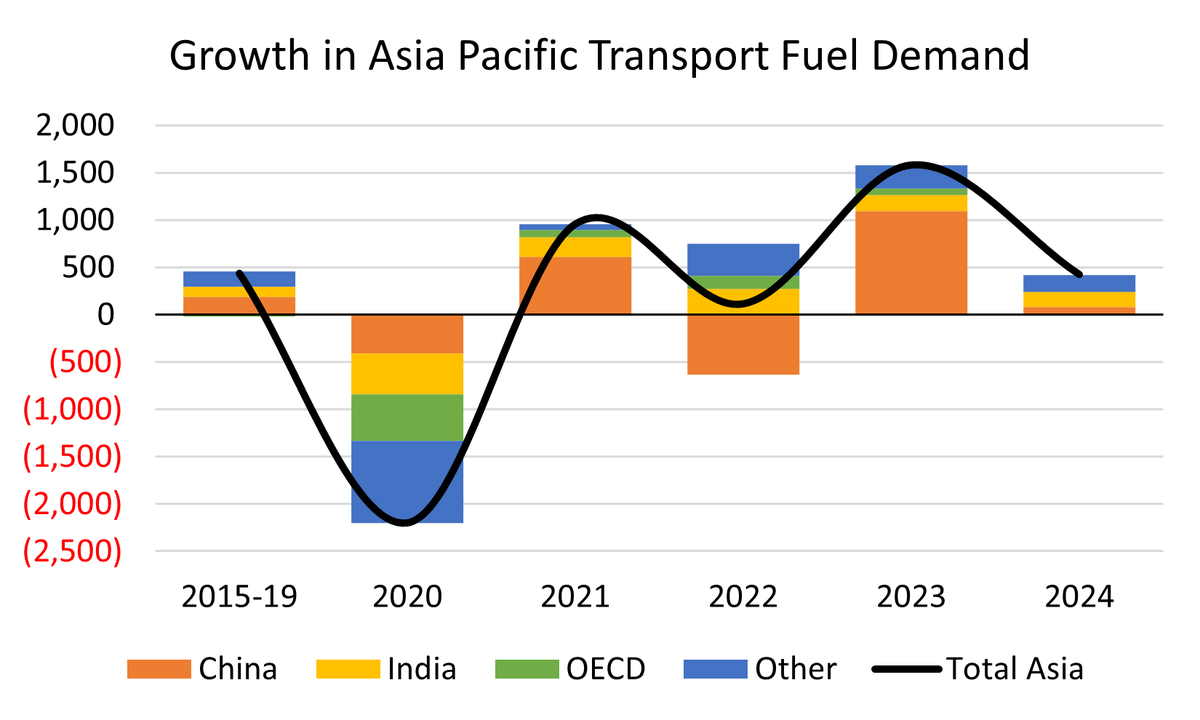

including a plateau in OECD demand, a sharp slowdown in China, continued strength in India and Southeast Asia, as well as downside risks in a few unstable and vulnerable economies such as Pakistan and Myanmar.

#OOTT#ESAIEnergy#OECD#Fuel#Demand

In 2024, demand for transport fuels in Asia Pacific will grow by 420,000 b/d, compared to a surge of nearly 1.6 million b/d in 2023. After fuel demand reached a full recovery last year, this slowdown is the result of multiple factors,

The war in Ukraine will continue through 2024 with Russian missile attacks and airstrikes escalating against major Ukrainian cities. However, the war will likely see less military mobility than in 2023.

Atlantic trade as 46 percent of all trade happening between Asia and the United States transits through the Canal and as China and East Asia continue to become important trading partners for Latin America

#OOTT#ESAIEnergy#PanamaCanal

The Panama Canal Authority (ACP) reduced the number of booking slots for ships transiting the canal. On average 13,000 ships transit this route every year, about 36 ships per day. This route is essential for Pacific -

US Shale consolidation continues to gain steam in 2023, particularly in the Permian Basin, where over 20 deals exceeding $100 billion have taken place. But consolidation is also benefiting operations in the Rockies, where rig productivity is increasing through longer laterals

on newly acquired contiguous acreage. ESAI Energy projects combined growth of a 100,000 b/d in 2024 from the Bakken and Niobrara. We have also adjusted our US supply forecast for 2024 upward due to better than expected productivity and increased drilling activity

ESAI Energy expects throughput to be relatively flat in 2024 as the weakness in diesel demand diminishes a bit. Meanwhile, the EU is considering new steps to reduce natural gas imports from Russia.

#OOTT#ESAIEnergy#Diesel#EU#Russia

Weaker European diesel demand and maintenance at refineries have reduced refinery throughput in 2023. In addition, diesel imports are down. 2023’s throughput is 11.3 million b/d, nearly 60,000 b/d lower than in 2022.

particularly Saudi Arabia on energy policy. The UAE will find it difficult to continue to be a leader in the fight against climate change and to be a member in OPEC.

#OOTT#ESAIEnergy#Energy#OPEC#COP28

The OPEC+ deal announced in November will effectively take an additional 700,000 b/d of crude oil off the market. Most of the announced 2.2 million b/d are cuts that have already occurred.

The voluntary nature of this round of cuts reignited the debate over the ability of OPEC+ to reach consensus deals with quotas and enforcement.

Meanwhile, COP28 further highlights the growing divergence between the UAE and the rest of the Arab Gulf,