Berkshire $BRK.B discipline with target income.

1⃣ Portfolio: BRK.B plus top 20 holdings of Berkshire

2⃣Income: 15% Target Annual Income Paid Monthly

Learn More: https://t.co/gRPafMl8If

Investing involves risk, principal loss is possible.

Distributed by Foreside Fund Services LLC.

The closest precedent is Japan. Tokyo spent a decade on governance reform before global investors repriced it. Korea is running the same playbook in a third of the time, and it layered the reform on top of the most important hardware chokepoint in AI.

Policy-driven re-ratings are durable. Policy plus an earnings supercycle is rare. Korea has both.

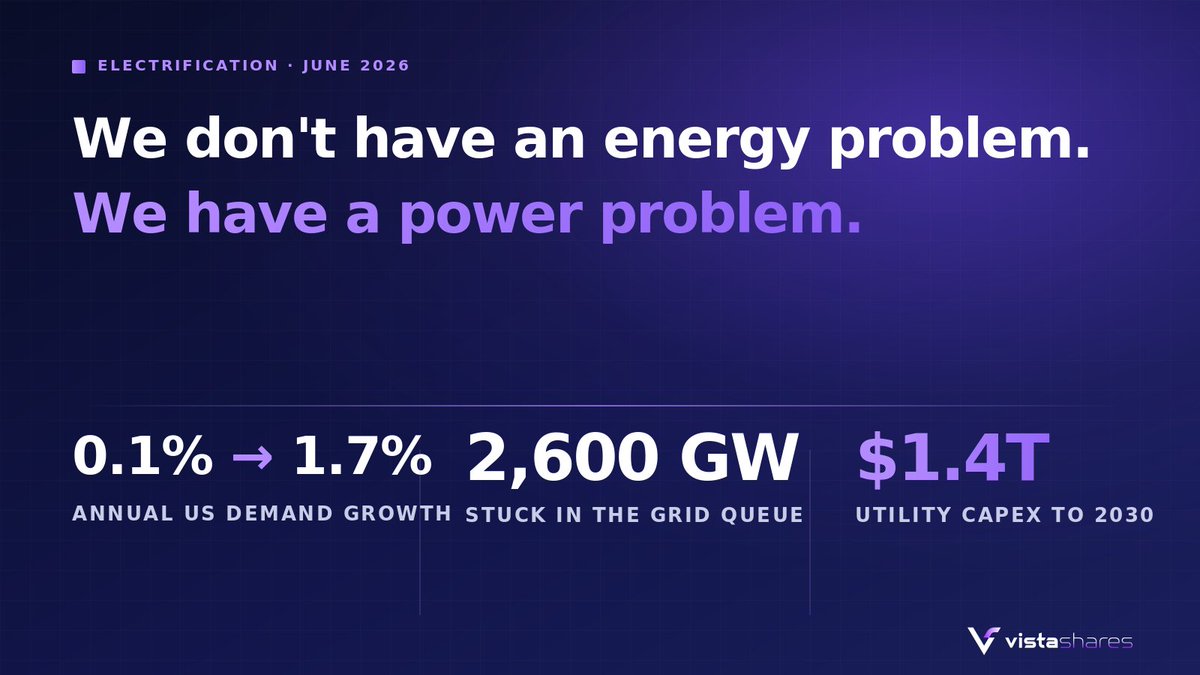

For the better part of two decades, American electricity demand barely moved. Utilities built little new capacity to deliver it, because they did not need to.

That era is over. Demand is rising again, and the grid already cannot keep up with what we use today, let alone what AI is about to add.

The United States does not have an energy problem. It has a power problem. We can make the electrons. We cannot get them to where they are needed.

$POW is the AI Power Infrastructure ETF

#electrification

Some are reading Apple's efficiency pitch as bearish for compute. It is the opposite.

Routing and on-device inference make AI cheaper per query. Cheaper per query means the world runs far more queries. Apple just put a frontier-class assistant in front of more than a billion devices, then built the plumbing to reach for the cloud the moment the on-device model is not enough.

Efficiency does not shrink the compute market. It expands it. The cheaper inference gets, the more of it everything consumes.

That is the demand curve the infrastructure owns.

The tell isn't that chips fell. Expensive things fall on bad news. That's what expensive means.

The tell is what the money did next. On the worst tape of the year it didn't go to cash. It went to Berkshire, insurers, and balance sheets that don't need the cycle to cooperate.

Capital is already voting on the next regime. Friday was just the first roll call.

For two-plus years, the trade that worked was crowding into the most expensive names in the market.

The top 10 stocks peaked at a record 40.7% of the S&P 500 last year. They are still nearly 40% of the index today.

The equity risk premium has shrunk to almost nothing, the thinnest since the dot-com era. The market is priced for everything to go right.

The crowd calls this momentum. What it actually is: the narrowest margin of safety in a generation.

Name the last regime that turned before the crowd saw it coming.

$QUSA ETF USA Quality Stocks Plus 15% Annual Income Paid Monthly.

Learn More: https://t.co/fPPL9hbaTq

The data center buildout has a twin. Grid capex just caught up to AI capex. $650 billion each in 2026.

Rystad Energy puts global grid spending above $650 billion this year, up 5% from last year and more than double 2020. Microsoft, Amazon, Google, Meta, and Oracle will spend roughly the same on capex this year, most of it on AI data centers. Everyone watches the data center number. Almost nobody watches the grid number. They are the same number.

Inside the Rystad report, the doubling since 2020 is explained by price inflation. Grid equipment got expensive because everyone needs it at once and nobody can make it fast enough.

→ Transformer and circuit breaker lead times in the US and Europe: 2 to 3 years, double the 2019 wait

→ A manufacturing expansion wave starts this year and runs through 2028, led by the US, the world's largest transformer importer

→ Near-term demand is utilities rebuilding the grid. The long-term demand, data centers and industrial electrification, is still ahead

When the queue is years long, the supplier sets the price. $650 billion a year is flowing toward the companies that make transformers, switchgear, and cable. And the buildout is still early.

$POW the AI Power Infrastructure ETF

https://t.co/5SXXSTZ6q7

The detail everyone is skipping: this is equity, not debt.

The 2001 telecom bust was lethal because the buildout was levered. Vendor financing, junk bonds, balance sheets that couldn't take a miss. Alphabet is funding compute with stock sales to the strongest balance sheet on earth. If returns disappoint, the loss sits where it can be absorbed.

That's the difference between a capex cycle and a credit cycle. So far, AI is the former.

Berkshire Hathaway just anchored Alphabet's roughly $80 billion equity raise with a $10 billion check. Greg Abel signed off on a weekend call, at a 5.5 to 6.5% discount to market.

Two signals matter more than the headline:

1. Hyperscaler AI capex has outgrown operating cash flow. When Alphabet sells stock to fund compute, the buildout has entered a new financing regime: equity raises, private placements, anchor investors. This is how railroads and telecom networks got built.

2. The most conservative balance sheet in America is now funding it. Buffett avoided tech for decades because he couldn't underwrite the winners. Abel just made Alphabet a top-4 Berkshire holding, rivaling Coca-Cola. With nearly $400 billion in cash to deploy, this is where he chose to put it.

When value capital starts financing the AI buildout on negotiated terms, it stops being a momentum trade and becomes a capital cycle.

Follow the capex. $AIS $POW $OMAH

https://t.co/HHnhNKfHql

Berkshire Hathaway just anchored Alphabet's roughly $80 billion equity raise with a $10 billion check. Greg Abel signed off on a weekend call, at a 5.5 to 6.5% discount to market.

Two signals matter more than the headline:

1. Hyperscaler AI capex has outgrown operating cash flow. When Alphabet sells stock to fund compute, the buildout has entered a new financing regime: equity raises, private placements, anchor investors. This is how railroads and telecom networks got built.

2. The most conservative balance sheet in America is now funding it. Buffett avoided tech for decades because he couldn't underwrite the winners. Abel just made Alphabet a top-4 Berkshire holding, rivaling Coca-Cola. With nearly $400 billion in cash to deploy, this is where he chose to put it.

When value capital starts financing the AI buildout on negotiated terms, it stops being a momentum trade and becomes a capital cycle.

Follow the capex. $AIS $POW $OMAH

https://t.co/HHnhNKfHql

$OMAH ETF holds Berkshire’s top names while seeking consistent income through options.

Learn More: https://t.co/fYfhe1nFti

Investing involves risk - Loss of Principal is Possible

Distributed by Foresides Fund Services

AI runs on power and the grid is racing to keep up. $POW invests in the infrastructure enabling datacenters, energy storage, and smart distribution networks that power the AI economy.

Learn More: https://t.co/8jIqNbtlfL

#electrification

Investing involves risk. Principal loss is possible. Distributed by Foreside Fund Services, LLC.

The US is trying to win the AI race on a power grid it can no longer build for itself.

Roughly 80 percent of its large power transformers are imported. The wait for a new one has gone from six weeks to as long as three years.

The constraint on AI is no longer the chip. It is the hardware that moves electricity, and a short list of companies controls it.

Everyone is racing to own the intelligence. Far fewer own what it physically runs on.

Which side do you think has more pricing power over the next decade? $POW physical AI infrastructure or $AIS AI intelligence infrastructure?

Everyone is hunting for the next bottleneck in AI.

Two years ago it was advanced packaging. $TSM CoWoS was sold out and the whole buildout waited on it.

Then it was memory. HBM became the tightest component in the stack, sold out through 2026.

Now it's power. You can get an AI chip faster than you can get a transformer, which runs three to four years out.

The bottleneck keeps moving. The capex keeps compounding. Stop guessing the chokepoint and follow the spend. $AIS & $POW follow this strategy.

What layer do you think binds next?

$AIS Outperforming $AIQ, $CHAT, $ARTY

Most AI ETFs own the same names.

$AIS doesn't - it focuses on the infrastructure companies powering AI growth - the "picks & shovels" behind the global AI value chain.

That difference is showing up clearly:

$AIS Outperforming $AIQ, $CHAT, $ARTY

Most AI ETFs own the same names.

$AIS doesn't - it focuses on the infrastructure companies powering AI growth - the "picks & shovels" behind the global AI value chain.

That difference is showing up clearly: