Automation is becoming a core layer of DeFi.

Vaults, strategies, and agents increasingly manage capital flows without constant human intervention.

This changes how liquidity behaves. Rebalancing becomes continuous. Incentives propagate faster. Capital rotates with less friction.

As automation scales, the design challenge shifts toward coordinating many automated actors operating on the same liquidity rails.

As DeFi matures, the main constraint is shifting from innovation to coordination. Many protocols can attract liquidity. Fewer can maintain it when conditions change.

Liquidity moves quickly, reacts to incentives, and concentrates around efficiency.

Infrastructure design increasingly revolves around one question: How does capital behave when everyone tries to move at the same time?

@marilyn100x@growthepie_eth Lower fees expand what strategies are viable on-chain.

Positions that were previously too small to justify gas can now be managed actively.

That opens the door to more accessible stablecoin lending, liquidity provision, and structured DeFi strategies.

Stablecoins are quietly reshaping how capital moves in DeFi.

When the base asset remains stable, strategies become easier to structure and risk becomes easier to measure. Lending, liquidity provision, and basis trades start to look less like speculation and more like capital allocation.

As stablecoin liquidity grows, DeFi begins to resemble a programmable financial market built around stable settlement layers.

Liquidity depth is often mistaken for TVL. They are not equivalent.

TVL measures parked capital. Depth measures executable size under stress. In calm conditions, both look sufficient. In volatility, only one absorbs flow without dislocation.

Designing DeFi infrastructure means asking:

- How fast can liquidity exit?

- Who warehouses imbalance?

- What incentives persist when spreads widen?

Capital efficiency matters. Liquidity resilience matters more.

Stablecoins are becoming core settlement layers inside DeFi.

As they scale, they change how capital can be deployed. Treasury management, lending, basis trades, and liquidity provision become accessible without embedding directional exposure. This expands the design space for stable-denominated strategies.

For many portfolios, that means participation in on-chain markets while keeping volatility tightly controlled.

The structural shift is simple: When the unit of account stabilizes, capital allocation becomes more deliberate.

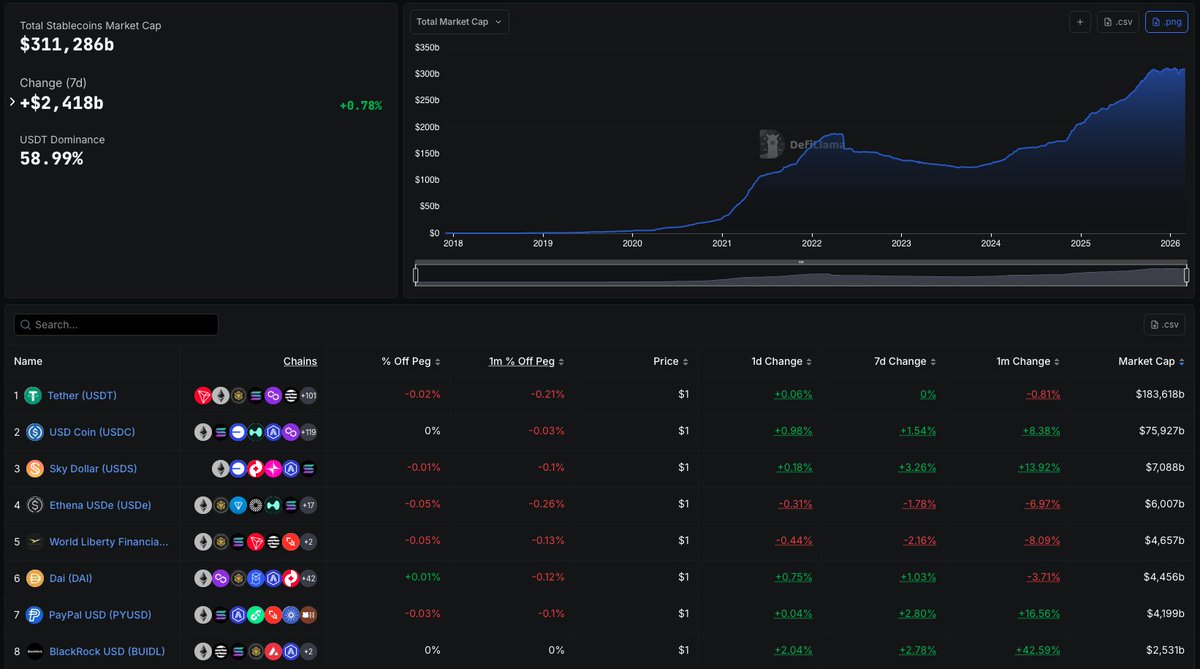

Source: @DefiLlama

Lower fees compress the minimum viable position size.

That expands participation because capital no longer needs to amortize high gas costs. Smaller portfolios can rebalance, hedge, or lend without friction dominating returns.

When transaction costs fall, DeFi shifts from whale-dominated flow to broader capital distribution.

If agents start allocating capital autonomously, the key variable becomes coordination.

When many systems optimize similar signals, liquidity can synchronize.

That increases speed and tightens feedback loops. The structural question is how markets behave when execution is machine-native, continuous, and incentive-driven.

DeFi discussion still centers on yield.The structural variable is liquidity coordination under stress.

When volatility expands, three dynamics matter:

- Withdrawal sequencing

- Inventory absorption

- Automation vs discretion in rule enforcement

- Most systems optimize for capital efficiency in stable conditions.

Fewer are designed for asymmetric behavior, inventory imbalances, and strategic exits. The relevant question is how liquidity behaves when it becomes active, not passive.

Infrastructure defines coordination rules for that moment.

If a platform like Meta integrates stablecoins natively, the key variable becomes velocity, not just supply.

High-frequency retail payments create continuous settlement flows, which changes reserve management, short-term rates exposure, and on/off-ramp liquidity demand.

At scale, stablecoins start behaving less like parked capital and more like monetary infrastructure.

Liquidity is becoming more engineered than directional.

In early DeFi, capital chased upside. Today, capital optimizes structure.

- Stablecoins monetize balance sheets.

- LPs monetize volatility.

- Stakers monetize security budgets.

- Perp venues monetize leverage demand.

Different revenue sources. Different risk surfaces.

The next cycle likely won’t be about “what goes up.” It will be about which liquidity models remain stable when volatility compresses and which ones require constant narrative fuel to function.

Price formation in crypto is still dominated by marginal liquidity, not fundamental cash flow.

When ETFs, derivatives, and basket products concentrate exposure, capital moves at the index level first and discriminates later.

Until liquidity fragments by asset quality, beta tends to override fundamentals in the short term.

Record staking levels also change Ethereum’s liquidity profile.

As more ETH sits in staking derivatives or validators, the freely tradable float tightens. That affects collateral dynamics, funding markets, and how volatility propagates through DeFi.

If activity continues to grow on top of a constrained float, market structure becomes part of the story.

The currency mix likely shapes liquidity behavior under stress.

Stablecoins with smaller absolute supply but higher relative deployment may experience sharper utilization swings when demand changes.

That has implications for rate volatility, pool depth, and how quickly liquidity migrates across venues.

If AI agents become persistent economic actors, they will require programmable balance sheets — wallets that can manage collateral, margin, and risk autonomously.

That introduces new design pressure on on-chain liquidity: continuous rebalancing, automated hedging, and capital efficiency at machine frequency.

The opportunity isn’t just more users. It’s a different class of liquidity demand altogether.

This ranking becomes more interesting when you look at how fees are generated.

Some protocols monetize transaction flow. Others monetize balance sheet exposure to short-term rates.

As rates move or volatility compresses, the composition of this table can shift materially, even if user activity doesn’t. Fee size matters. Fee sensitivity matters more.

Most people DCA into a downtrend. Few realize AMMs let you get paid to do it.

If you want to accumulate a token that’s trending lower, the default approach is simple: buy spot over time. But AMMs introduce a different execution model.

Instead of placing periodic market buys, you provide liquidity against a strong asset (e.g. USDC) within a defined range. As price declines into your range, the pool gradually converts your capital into the token you want to accumulate.

You are effectively:

- Buying more as price falls

- Letting volatility execute the trade

- Earning fees while flow passes through your range

This is not yield farming. It’s inventory acquisition through mechanism design.

Structurally, the difference looks like this:

DCA = time-based execution.

LP accumulation = volatility-conditioned execution.

But the trade-off matters. When you LP, you are short convexity.

- You earn fees during churn.

- You accumulate faster if price bleeds lower.

- You give up upside if price rips aggressively.

So the real question isn’t “are the fees attractive?”

It’s:

Are you comfortable exchanging convex upside for flow monetization while building inventory?

Used correctly, LP positions aren’t just passive yield tools. They’re programmable accumulation strategies embedded in market structure.

Strong framing.

One additional lens: exchanges also differ in how liquidity risk is allocated.

In CEX models, risk is largely internalized within a corporate balance sheet. In DEX models, risk is modularized and distributed across LPs through mechanism design.

That difference tends to matter most during volatility, not during normal execution.

@FourVork Most of this is operational literacy. The harder question is structural:

Who provides balance sheet when markets gap, and how is that risk priced on-chain?

That’s where DeFi stops being a playground and becomes market structure.

how to master defi

- get an understanding of how ethereum works

- do basic swaps on uniswap, lend on aave

- ask yourself how it works under the hood, try to answer

- learn defi basics from youtube and protocol docs

- study AMMs (uniswap v2/v3, balancer, curve), liquidity provisioning, impermanent loos, lending protocols, LTV

- find a protocol with a liquidity mining campaign (like @katana) and start farming incentives on LPs

- study tokenomics and emissions. at some point research ve 3,3 as well

- study smart contract risks, read rektnews

- learn mev, slippage, oracles

- research different types of bridges

- learn onchain analysis with arkham/etherscan/nansen

- understand narratives and capital rotation

- learn how to do R:R assesment, make sure you are good at DYOR

- start farming in defi with bigger capital, diversify farms

- start reading vitalik's blog, cobie's blog, hack post mortems, messari crypto reports

- learn how to read solidity, at least things you'll need on etherescan

- ask smart people or LLMs hard questions on defi. Use gemini's canvas to repeat

- feel free to ask me recomendations on who to follow and what tools to learn

learning the fundamentels is the best thing you can do in a bad market.

good luck