Developer of quantitative models. Creating systematic approaches to Risk, Sentiment, Macro & Statistical analysis. Where others speculate, we systematize.

We created a free tool that shows you exactly how much carry costs eat into your returns when your account currency doesn't match what you trade.

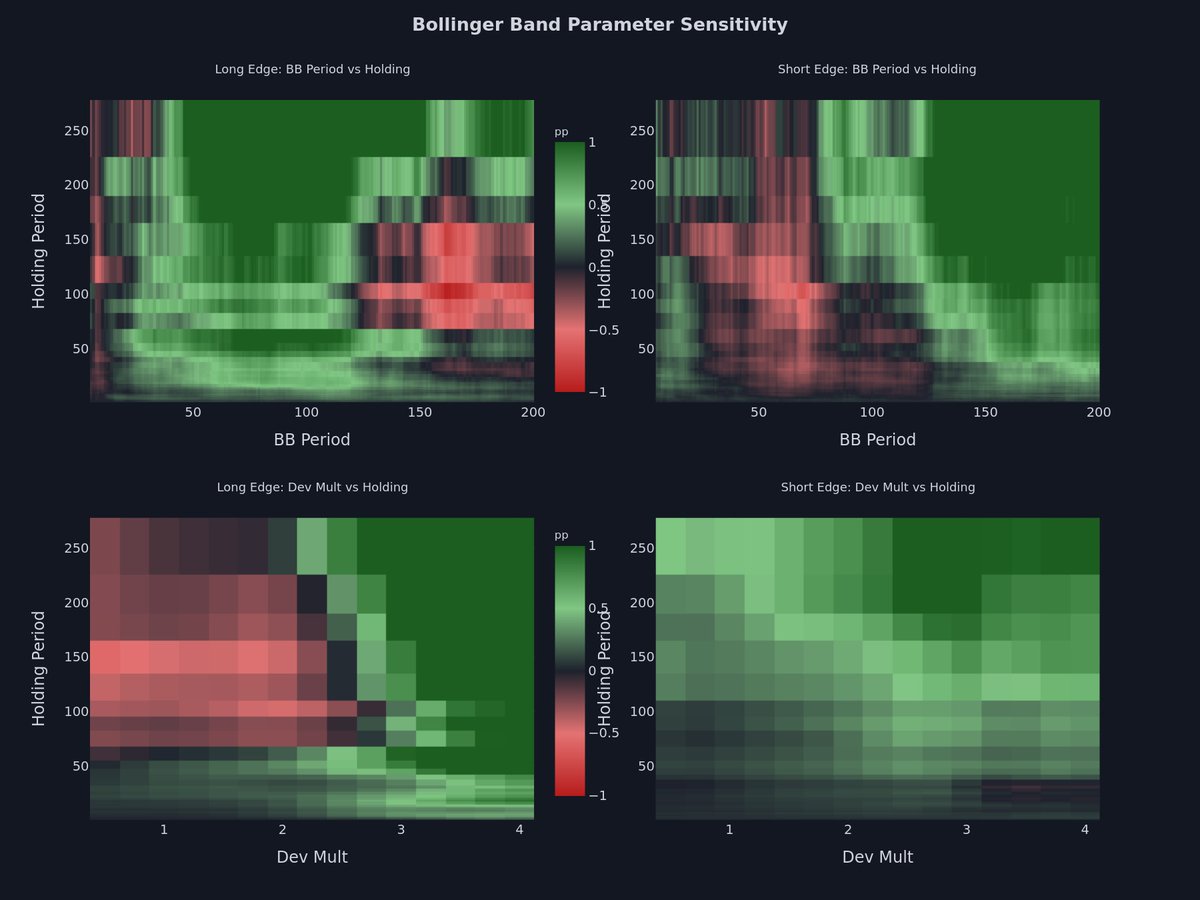

@tradingview

https://t.co/uCtE8MKojY

Dividend investing is one of the most popular strategies among. The idea is straightforward: buy stocks that pay regular dividends, and you receive a steady stream of income. But there is a problem with this framework.

@tradingview

https://t.co/ZQkSfhPKeU

Most risk indicators react to price. The Market Entropy Index measures what happens underneath: when sector participation narrows, direction breaks down, and credit markets stop pricing risk. A leading indicator, not a crash detector.

@tradingview

https://t.co/ks4ZcS8lZS

VAA is live on TradingView.

Tracks breadth momentum across 7 ETFs and switches between offensive and defensive allocation monthly. Based on Keller & Keuning (2017, SSRN 3002624).

https://t.co/vv6ifiSXKL

@tradingview

The 60/40 Portfolio Has a Regime Problem

A 2026 review article makes the case that static 60/40 allocation is structurally exposed to regime changes. The fix is not to abandon diversification but to make it conditional on the macro state.

https://t.co/znCmb4Eh9E

Your Backtest Is Lying to You

This article explains the three methods we use in our published research, then looks at what professional quantitative researchers add on top of that.

https://t.co/W0PwVciuZh

@tradingview

@ScoutAI_Trading Fair point on risk management being underweighted in most ML-for-trading research. The paper does address this partly through its gatekeeping layer (turnover penalties, drawdown constraints, multi-model risk adjustment).

An AI That Discovers Its Own Trading Factors. Does It Actually Work?

A recent paper from HKUST proposes an autonomous AI system that generates, tests, and refines its own equity factors without human guidance.

https://t.co/vRxPHIg9F0

We tested 6M VWAP configurations. Crossover: 0 significant results. Mean reversion: 150,000+. The most popular VWAP strategy is worthless. Full study:

https://t.co/lTYj0mU7wW

@tradingview@alphatrends@investingidiocy