1/ We are launching 0dAMM with @avnu_fi.

A new onchain market structure for STRK: tight, transparent, programmable liquidity built directly on Starknet.

A few notes after integrating both read and write priority fees on HL:

- Many have been wondering why priority fee revenue hasn't ramped faster. It's a combination of two things. Makers need time to integrate, but the bigger issue is the validators, they have to explicitly enable the gossip priority config to respect the read auction ordering. Not all validators have done this yet, which means winning the gossip auction today doesn't guarantee you actually get prioritized access to the mempool. Rn you might end up burning your precious HYPE for nothing

- Many retail traders don't know this, but before this upgrade you needed to pay validators to get access to sentry peering or other kind of dedicated setups in order to have competitive latency as an API trader, which had a cost of a few tens of thousands of dollars per month depending on the provider. This upgrade directly targets these setups, and will internalize most of these fees into HYPE burning. It's hard to estimate the exact numbers, but I would say that this upgrade just added $500k-$1m monthly buying pressure on HYPE, with potential for write fees to grow much more.

- This is a first step from the HL team to try to internalize more revenue from latency and infra investments that most HFT teams spend. This is something traditional exchanges have been trying to do for a while (IEX introduced a 350μs speed bump and refused to offer colocation entirely, NYSE/CME keep building bigger colo facilities to capture more of this spend), and the biggest risk is destroying your microstructure because the exchange becomes too expensive for makers, or too slow. But the risk is definetly worth the reward. BIS research estimates the HFT arms race extracts $5B/yr in global equities alone, or about 0.5bps on all volume. Growth mode assets on HL charge 0.45 - 0.9bps in taker fees, so if priority fees capture even a fraction of that 0.5bps equivalent, that's potentially doubling protocol revenue on these markets. I'd estimate monthly infra spending from HFT teams on HL today to be in the ballpark of $5-10M between sentry peering, server optimization, and brainpower. Priority fees are how the protocol captures a share of that. My bold take is that trading fees will compress over time as competition forces HL to stay in growth mode for HIP-3 markets. Priority fees won't since they're driven by the arms race itself, which grows with more volume. My guess is this revenue line becomes more than half of HL's revenue in a few years if they manage to capture more flow from TradFi.

Perpetual futures will become a primary venue for price discovery in TradFi markets, but they will not replace dated futures and options.

Today, price discovery happens across different instruments. Equities and FX primarily trade on spot markets, while commodities and energy rely on dated futures.

USDC-settled perpetuals offer structural advantages that make them a strong alternative for trading and liquidity concentration:

1. They trade 24/7

2. They aggregate liquidity into a single order book and are structurally standardized

3. They enable higher capital efficiency through continuous margining

Importantly, many of these advantages are structural. Traditional financial markets are not 24/7 not only due to historical inertia, but because risk management and settlement operate in discrete cycles. Margining is not continuous, and collateral transfers and custody updates occur in batches, requiring system-wide coordination.

At the same time, traditional derivatives markets fragment liquidity. Dated futures split liquidity across expiries, while options spread it further across expiries and strikes. As a result, liquidity is distributed across many instruments.

Perpetuals reverse this dynamic by consolidating liquidity into a single instrument per asset and providing a standardized structure across markets, with no rolling and simpler basis management. This makes them easier to hedge and trade.

Perpetuals also allow for more capital-efficient use of margin through continuous risk management and liquidation mechanisms, although this comes with different risk trade-offs compared to the more conservative, discrete systems used in TradFi.

Given these dynamics, USDC-settled perpetuals will become a primary venue for trading and price discovery in TradFi assets over time. However, several challenges remain:

1. Trust and inertia: Institutions will need time to build confidence in crypto-native infrastructure and adapt their internal processes and risk frameworks, for example moving from futures term structure to perp funding dynamics.

2. Index definition: Perpetual markets depend on a clear and reliable reference price. For TradFi assets, this requires consistent and widely accepted methodologies. This means spot-based references for equities and FX, and derived spot prices from futures for commodities and energy. In practice, areas like futures roll and non-trading hours are not yet fully standardised across the industry. We also recognise that the current approach used by Extended is not yet ideal, and we are actively working to improve the definition of a fair and robust reference price.

Even if perps become dominant for trading, they will not replace dated futures and options, as these serve different purposes:

1. Dated futures provide time-specific hedging and a strong link to the real economy through physical delivery and convergence to spot at expiry.

2. Options provide convex payoffs and enable trading and hedging of volatility.

In summary, perpetuals are structurally better suited for liquidity aggregation and continuous trading, and will play a leading role in price discovery. However, they will coexist with dated futures and options, which remain essential for time-specific hedging and non-linear risk management.

Bridging perps and TradFi represents one of the largest and most durable opportunities in financial markets and is a core focus for Extended.

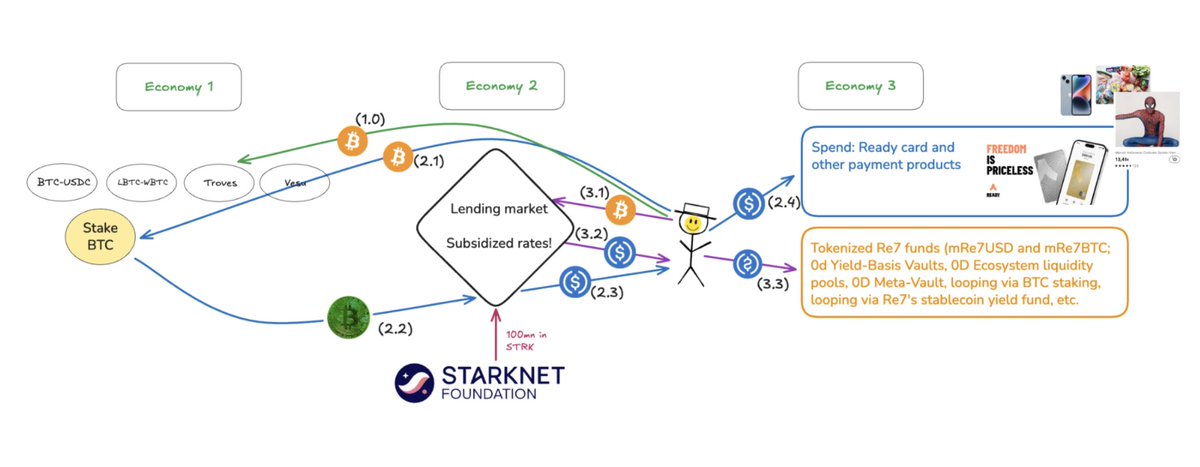

We're launching two yield products in 2 weeks, one on USDC around 20% APY and one BTC around 10% APY, all gross fees.

If that's interesting to you DMs open, I'd love your feedback on the r/r and on caps.

cc @0DFinance

8 new ways to put your BTC to work.

All available on Starknet right now.

Bridge when you’re ready, but make sure you actually know what BTCFi on Starknet can do for you.

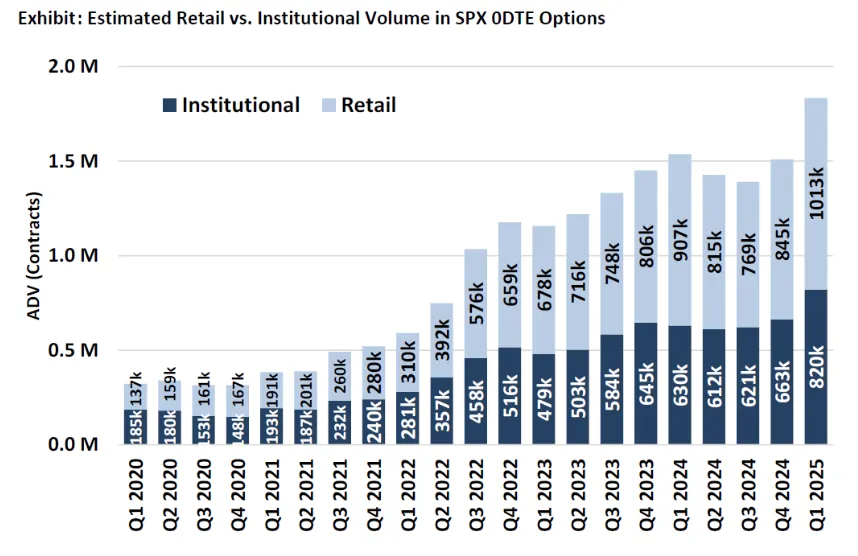

The perps vs CFDs debate is the wrong one, the real debate should be perps vs 0DTE, especially in the short term.

To simplify there's roughly 2 categories of flow for a stock perp instrument: speculation and hedging. Given how early we are, liquidity is order of magnitude worse than what you could get on any broker. It would be a big strategic mistake for any exchange to target the hedging flow, because it's a highly price sensitive flow.

The only way to even stand a chance to compete with the traditional financial market in the long term is to first attract the speculative flow through a high leverage offer 24/7. Good news is retail traders are starving for this kind of products, just take a look at the 0DTE retail volume growth.

How is a perp superior to 0DTE for speculation? It's far easier to understand, you just need a slider for leverage and one for margin + a button and you directly understand your exposure, you get no theta bleeding and it's a far better experience for micro sizing. Just take a look at the @liquidtrading UX, in 2 clicks you get linear exposure to any underlying

Only after winning this segment can you start thinking about winning the hedging battle. And this is where it gets interesting, why would any hedge fund prefer a perp exposure over their current combination of futures + options + TRS?

It seems very clear to me that perps (in a mature stage with predictable funding rates and spreads) are a better hedging tool than futures, especially because there's no need to roll positions. The TRS flow, the institutional twin of CFDs, is also realistically absorbable by perps, because it has the same payoff, and having a shared margin would make it more efficient. And btw if one instrument absorbs the flow of two different ones, it will be much more liquid, and thus efficient. Only the option stack should remain here, because of their convexity.

There are still many things that could go wrong, especially with oracles, and the path to deep liquidity, but I think at this point given the multiple world class teams going after it that it's not an if question but a when question.

🚨 AVNU x BTCFi

BTCFi just launched to make Starknet the Bitcoin place to be. Here’s what we shipped:

1. Native integration of new BTC liquidity (@Re7Labs + @Splinefinance) for better trading execution

2. All BTC flavors now usable as gas tokens via the Paymaster

3. Curated token list for BTC assets

tldr; If you trade on Starknet, you trade on avnu 👇

The new BTC economy is live.

@Starknet's BTCfi brings new protocols, yield opportunities, sustainable ecosystem growth, and deep liquidity to Starknet. It’s been designed to ensure your Bitcoin remains safe while it’s put to work.

An overview of how BTCfi works in thread 🧵