20 years in global banks taught me what matters in investing and how much noise surrounds it. Bringing simplicity to find great companies and understand markets

@burrytracker You didn’t need to find Nvidia. You just needed to buy Microsoft, let it compound at ~15% a year plus dividends, and get rich slowly over 25 years. Buying quality and being patient pays off.

@EndTesla Yes, 2027 seems to be where the disappointment is.

The call arguably gave better longer-term visibility, especially into 2028, but the near-term AI semi ramp did not reset high enough for expectations.

Just came out of the $AVGO earnings call.

The stock is now down about 12%, but the call did not sound like an AI demand problem.

It sounded like the opposite.

Broadcom is moving from “big AI chip beneficiary” to a broader AI infrastructure platform across custom silicon, networking and financing/deployment partnerships.

KEY TAKEAWAYS

AI demand still looks extremely strong.

Management said demand for XPUs and networking is “insatiable” and highlighted over $30B of AI semiconductor bookings in the quarter, versus $10.8B shipped.

That matters because Broadcom is no longer only talking about the next quarter.

Visibility now extends into 2028, and management reiterated more than $100B of AI semiconductor revenue in FY27.

The customer base is broadening too.

Google remains strategic, but Anthropic, OpenAI, Meta and two other customers are now part of the multi-year AI ramp. Meta’s initial 1GW order has been received, with deliveries expected to start in the second half of 2027.

Networking remains central to the story.

Broadcom made clear that scalable AI clusters are not just about accelerators. Its role also includes switches, DSPs, lasers, NICs, routers, fabric and optical connectivity.

That is why the call was bigger than custom chips.

AVGO is increasingly tied to the full buildout problem: compute, cluster scale, power planning, networking and financing.

KEY QUESTIONS ANSWERED

The AI infrastructure runway still looks long.

The call suggested demand is pushing further into 2027 and 2028, not fading after the current buildout.

WHAT STILL NEEDS TO PROVE OUT

Expectations.

The business is executing exceptionally well, but the stock had already priced in a lot of good news.

Investors will now want to see whether bookings convert smoothly, supply keeps up, margin pressure stays mix-driven, and the 2027/2028 AI ramp arrives as planned.

Strong business.

Demanding stock.

The selloff says more about the bar than the direction of the AI infrastructure story.

$AVGO beat, but the bar was very high.

Revenue: $22.19B vs ~$22.1–$22.13B exp, +48% YoY

Adjusted EPS: $2.44 vs ~$2.40 exp (beat)

AI semiconductor revenue: $10.8B, +143% YoY

Q3 revenue guide: ~$29.4B vs ~$28.3–$28.7B exp

Broadcom delivered record revenue, strong earnings and another huge quarter for AI semiconductors.

But the market looked past the headline numbers. AI semiconductor revenue was below some expectations, free cash flow missed and the strong Q3 guide still may not have cleared the very high bar.

Stock: down 5% after hours.

Verdict: Broadcom continues to prove it is one of the biggest AI infrastructure beneficiaries across custom chips and networking. But after a strong run, the reaction shows investors wanted more than a beat and strong guidance. The debate now centers on how much future AI upside is already priced in.

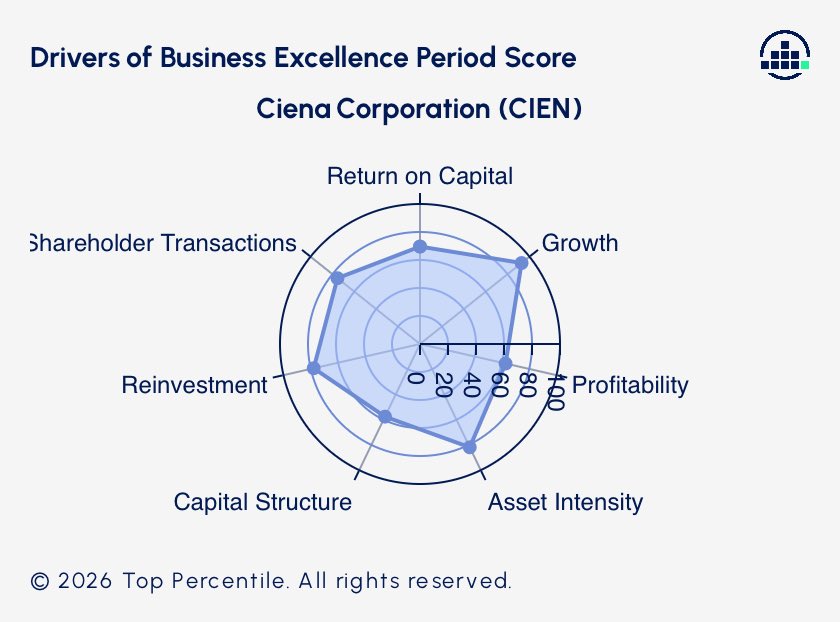

$CIEN Earnings (tomorrow, before open)

Optical networking company benefiting from rising bandwidth and data movement requirements across AI infrastructure.

Ciena’s fundamentals have improved as demand for high-speed networking has increased, although investors are still debating how much AI demand can offset softer spending from traditional telecom customers.

RECENT PRICE ACTION

+165.3% YTD

+15.9% over the last month

Last earnings move: -14.4%

WHAT HAPPENED AT LAST EARNINGS?

Ciena delivered solid results, supported by growing networking demand and improving order trends.

The stock fell as investors focused more on the pace of future growth and whether AI-related demand would be enough to offset weakness in traditional telecom spending.

WHAT HAPPENED LATELY?

The stock has rallied sharply as investors became more optimistic about the role of optical networking in AI infrastructure.

As AI clusters become larger and move more data, attention has increasingly shifted toward the networking layer that connects compute, memory and storage. Growing hyperscaler demand has further strengthened that narrative.

The chart attached shows an interesting profile: strong growth, reinvestment and capital allocation, but profitability remains the area investors are watching most closely.

KEY QUESTIONS FOR EARNINGS

Can AI-driven networking demand offset softer traditional telecom spending?

Can guidance support the stock’s huge move this year?

@RKLBMan@KobeissiLetter The chart is mapping stack exposure rather than business quality, so a company can be excellent without needing a lot of box ticked.

Curious which row or column looks off to you.

@topchoiceinvest I feel for you. Strong results, disappointing reaction.

But this was a high bar problem. $AVGO is still one of the better AI infrastructure stories.

@Mr_Derivatives Feels less like demand broke and more like expectations got heavy.

$AVGO still sounded strong on bookings, visibility and 2028 demand.

$CRWD beat and raised too, but that also wasn’t enough.

At this point, “very strong” can trade like disappointment.

@StockSavvyShay Less “next quarter upside.”

More “how long can this buildout last?”

The formal 2027 framework did not really reset higher, but deals like Anthropic/Google TPU access are why the call still pushed visibility further into 2028.

$CRWD beat and raised guidance, but the stock fell.

Revenue: $1.39B vs ~$1.36B exp (beat), +26% YoY

Adjusted EPS: $1.10 vs ~$1.07 exp (beat)

Free Cash Flow: $468M vs ~$447M exp

Net New ARR: $256M vs ~$249M exp

FY27 revenue guide: ~$5.94B midpoint (raised) vs ~$5.91B exp

CrowdStrike delivered another strong quarter, with revenue, earnings, cash flow and net new ARR all ahead of expectations.

The standout datapoint was net new ARR, which grew 32% YoY and helped push total ARR to $5.51B. Management also raised full-year expectations and pointed to growing momentum around AI security and platform adoption.

Stock: down 10% after hours.

Verdict: the quarter was strong, but expectations were stronger. After a nearly 70% rally in the last month, investors were looking for a bigger upside surprise. The debate now centers on whether AI security momentum and platform adoption can continue accelerating fast enough to justify the stock’s recent rally.

$CRWD Earnings (tomorrow, after close)

Cybersecurity platform using AI to help protect and automate enterprise security operations.

CrowdStrike remains one of the stronger businesses in the software sector, with investors increasingly viewing AI as a demand driver for cybersecurity rather than a disruption risk.

RECENT PRICE ACTION

+64.0% YTD

+68.8% over the last month

Last earnings move: +1.8%

WHAT HAPPENED AT LAST EARNINGS?

CrowdStrike delivered stronger-than-expected results, helped by continued platform adoption, ARR growth and improving profitability.

The stock moved only modestly higher as investors balanced strong execution against valuation and expectations.

WHAT HAPPENED LATELY?

The stock has surged over the last month as cybersecurity sentiment improved and investors became more constructive on AI-driven security demand.

That sharp rally raises the bar for earnings. CrowdStrike now needs to show that growth, platform adoption and AI security momentum are keeping up with the stock.

KEY QUESTIONS FOR EARNINGS

Can AI security become a meaningful growth driver?

Can platform adoption keep supporting ARR growth?

Can results justify the sharp move in the stock?

$AVGO beat, but the bar was very high.

Revenue: $22.19B vs ~$22.1–$22.13B exp, +48% YoY

Adjusted EPS: $2.44 vs ~$2.40 exp (beat)

AI semiconductor revenue: $10.8B, +143% YoY

Q3 revenue guide: ~$29.4B vs ~$28.3–$28.7B exp

Broadcom delivered record revenue, strong earnings and another huge quarter for AI semiconductors.

But the market looked past the headline numbers. AI semiconductor revenue was below some expectations, free cash flow missed and the strong Q3 guide still may not have cleared the very high bar.

Stock: down 5% after hours.

Verdict: Broadcom continues to prove it is one of the biggest AI infrastructure beneficiaries across custom chips and networking. But after a strong run, the reaction shows investors wanted more than a beat and strong guidance. The debate now centers on how much future AI upside is already priced in.

$AVGO Earnings (today, after close)

Semiconductor and infrastructure software giant benefiting from custom AI chips, networking and hyperscaler AI spending.

Broadcom’s fundamentals have strengthened significantly over the last few years as the company has expanded beyond traditional semiconductors into AI infrastructure, networking and software.

RECENT PRICE ACTION

* +39.1% YTD

* +14.3% over the last month

* Last earnings move: +6.0%

WHAT HAPPENED AT LAST EARNINGS?

Broadcom delivered stronger-than-expected results, helped by continued strength in AI semiconductors and networking.

Management also raised expectations for AI revenue, reinforcing confidence that Broadcom is becoming one of the largest beneficiaries of AI infrastructure spending.

WHAT HAPPENED LATELY?

The stock has continued climbing as investors became more confident in Broadcom’s position across custom AI chips and networking.

Recent attention has focused on growing AI spending from hyperscalers, with increasing expectations that Broadcom can benefit from both custom silicon and the networking infrastructure required to scale AI clusters.

KEY QUESTIONS FOR EARNINGS

* Can Broadcom keep expanding its AI opportunity beyond current expectations?

* Are custom AI chips and networking demand continuing to accelerate?

* Can guidance support the recent rise in expectations?

@PolymarketMoney $GOOGL was buying back stock recently and still had plenty of funding options.

So raising this much equity says something.

AI infrastructure spend may be getting bigger, faster and longer than even Google expected a few months ago.

@BourbonCap $PATH is quietly moving toward the top of the market on fundamentals.

But it is in the “no one cares” bucket - not AI infra, not semis, not space.

@stckpkr7000@amitisinvesting Revenue outlook increased by $1.5B.

Interconnect growth outlook increased from 50% to 70%+.

FY28 revenue still expected to grow ~45%.

Is that really mediocre?