The response to the 11th BlackRock Applied Research Award has been truly outstanding! We received a record number of high-quality submissions from PhD candidates. This success wouldn't be possible without IFA and @IIM_Vizag.

@VoicesofIndAcad@PhD_Genie

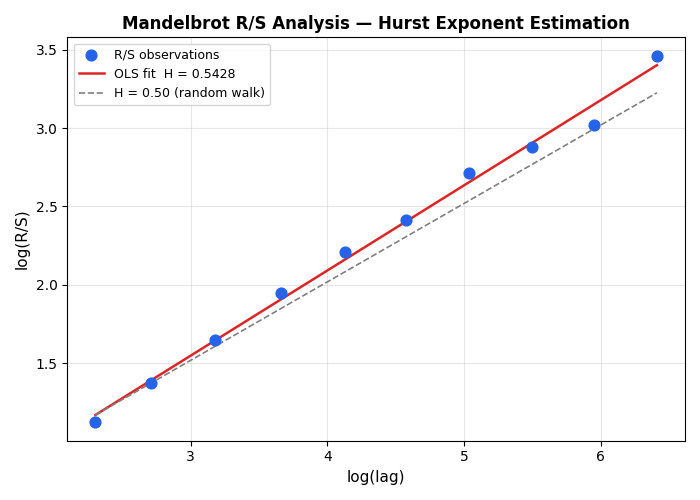

Heard an argument about market retracement by golden ratio of 61.8%. That reminds me of Mandelbrot set- so ran the simulation on Nifty 50 data set. The 10 year projection from 2016 to 2026 comes to be median of 22400, which is starting about 8000 Nifty point it came very close to current market rate. What will be Nifty value in next 10 years ?

@tinvk1@Rajatsharma_87@sachin_rt I appreciate the subtle swing in old ball leather. Try yourself, at least let's make a list of the swing bowlers in India as arm chair critique.

In quantitative finance, we often focus on the "what" and the "how" through data and models. However, Professor Robert Shiller’s work highlights the "why"—the contagious narratives that influence human behavior and, ultimately, the global economy.

Understanding the "epidemiology" of economic stories—from the Great Depression to the rise of #crypto—is more relevant today than ever. In an age of instant information, the stories we tell can be as impactful as the underlying fundamentals.

Try this course @coursera

Imagine a classroom in Tihu College, Assam. It is a humble setting where local students come to learn the basics of physics. At the front of the room stands a man who looks like any other dedicated prof. But when the bell rings & the students leave, Atanu Nath plugs back into the global grid. He is calculating the g-2 factor: a measurement so precise it is like measuring the distance from Earth to the Moon with the accuracy of a human hair.

The Muon is like a fat version of an electron. According to every physics book written in the last 50 yrs, it should wobble at a specific rate when put in a magnetic field. But it does not It wobbles differently. Prof. Nath was part of the elite global team that tracked this tiny, impossible discrepancy.

The Northeast has always been a Silo of culture & resilience, but in the world of high-energy particle physics, it was often a Ghost region. By winning the 2026 Breakthrough Prize, Prof. Nath shattered that ceiling. He proved that a scientist from Lalabazar, Hailakandi, can sit at the same table as the legends of Brookhaven & CERN.

Even with a Breakthrough Prize (and its multi-million dollar purse shared among the team), Prof. Nath remains an Assistant Prof at a local college. He represents the India Bull spirit: the refusal to move to the Big City because the mind can travel further than the body ever could.

Revisiting Momentum investing

Momentum-the tendency of past winners to continue outperforming past losers over intermediate horizons-is among the most robust anomalies in empirical finance. Its behavioural foundations, rooted in investor overconfidence and self-attribution bias, imply that the full premium can only be harvested through a zero-investment long-short portfolio that simultaneously exploits the continuation of winners and the further decline of losers. Yet every momentum-oriented mutual fund and index product available to Indian investors-including the benchmark Nifty200 Momentum 30 Index and its associated exchange-traded funds-is structurally long-only. We argue that this is not a minor implementation detail but a fundamental misalignment between the economic mechanism generating the momentum premium and the investment vehicle used to capture it. Using the Nifty 50 universe, we construct a standard 12-1 month cross-sectional momentum strategy and demonstrate that the long-short (WML) portfolio delivers materially higher risk-adjusted returns than the long-only winner decile alone. We further document the structural barriers regulatory constraints on short-selling by mutual funds under SEBI regulations, limited Securities Lending and Borrowing (SLB) depth, and product-design inertia-that prevent Indian fund managers from capturing the complete premium. Our findings suggest that Indian momentum funds are more aptly described as heuristic, discretion-laden products than as fully quantitative implementations of the academically established momentum factor. We conclude with proposals for a richer product architecture, including long-short Specialised Investment Funds (SIF) under the recently introduced SEBI framework.

#stockmarket