The current sYUSD 7d APY is 3.7%, above the 4-week treasury bill yield.

The yield comes from the YUSD reserve strategy, which allocates between the BTC funding rate carry.

Buy YUSD to start receiving yield: https://t.co/GKNvT0Kq0W

@astaaXBT@martenogrady@babylonlabs_io@aave@aegis_im The most up-to-date information about Aegis is on X. Nevertheless, we are trying to catch up with every request on Discord as well

If you have a specific request, please DM me

This is a real step for Bitcoin infrastructure.

@babylonlabs_io took native Bitcoin-backed borrowing to @aave v4 public testnet, built on Trustless Bitcoin Vaults. Post $BTC as collateral and borrow while keeping custody, with no wrapping and no moving across chains.

@aegis_im has been BTC-first from day one. Great to see more native $BTC credit shipping.

Try it below 👇

Native Bitcoin-backed borrowing is live on Public Testnet with @aave v4.

Powered by Babylon Trustless Bitcoin Vaults, users can post Bitcoin as collateral and borrow without giving up custody, wrapping, or bridging.

This is the latest step in building native Bitcoin-backed credit markets.

I get asked why $sYUSD yield is not a fixed number.

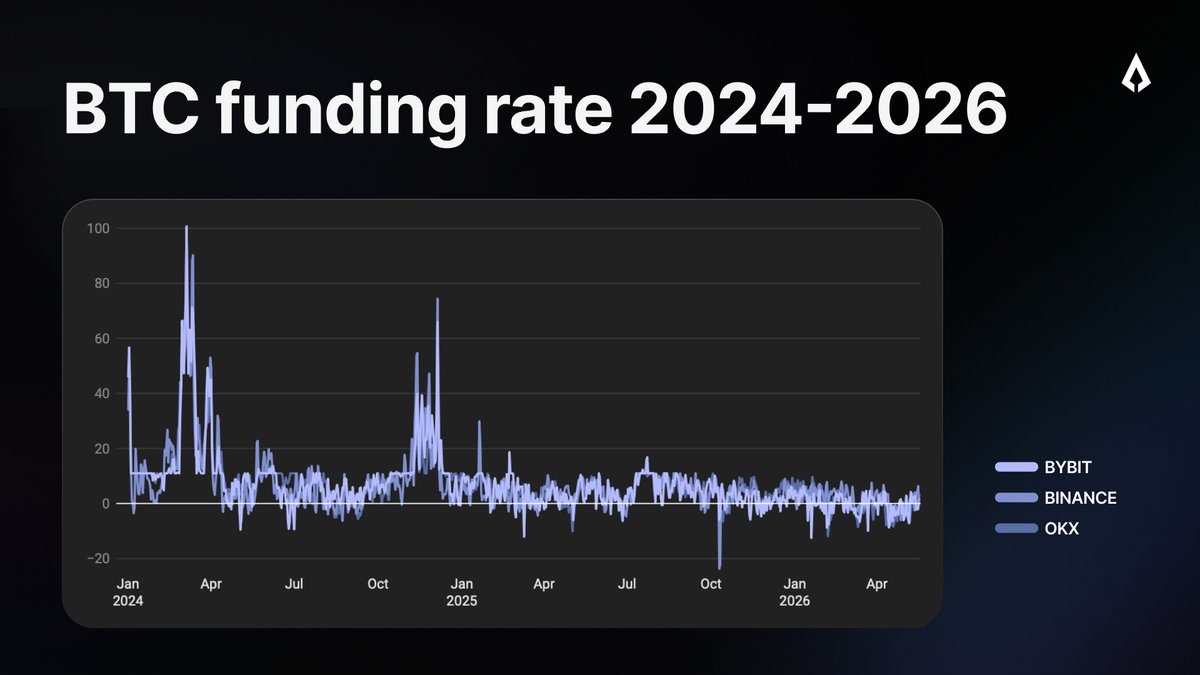

This chart is why. The annualized BTC funding carry that backs the yield ran a 12.2% mean in 2024, 4.4% in 2025 and 3.5% so far in 2026.

The $sYUSD APY tracks that realized carry every week. We do not quote a fixed rate we cannot earn.

On the negative funding days the insurance fund covers the outflow, so the realized yield to a holder does not go negative.

BTC perpetual funding rate carry is the source of $sYUSD yield.

This chart plots the daily BTC funding rate across @binance, @bybit_official and @okx from January 2024 through May 2026, annualized.

The carry compressed every year:

• 2024 mean: 12.2%

• 2025 mean: 4.4%

• 2026 year to date: 3.5%

It peaked at 92.57% on March 5, 2024 and reached a low of -8.16% on October 10, 2025. The last 30 days of the set averaged -1.2%.

$sYUSD paid yield every week across the full period.

When funding is positive the short BTC perpetual position earns carry and Aegis distributes that carry to $sYUSD holders. When funding is negative the Aegis insurance fund covers the funding outflow and holders do not realize a negative yield day.

Proof of reserves: https://t.co/tRbjZlo4sZ

What matters most is being transparent about the underlying strategies and risks you're taking on.

Aegis stays 100% transparent, relying on @AccountableData to show everyone what's happening behind the curtain.

1/ 5 yield-bearing stablecoins. 5 different yield sources.

A research thread on where the yield actually comes from in sUSDe, sUSDS, sUSDai, sjUSD and sYUSD 🧵

sjUSD continues to generate yield through the JLP strategy.

jUSD uses JLP as collateral. JLP accrues trading fees, funding payments and liquidation proceeds from @JupiterExchange Perps. Aegis hedges BTC, ETH and SOL exposure to keep the position delta-neutral.

7d APY: 5.8%

Buy sjUSD: https://t.co/ag8BGR1sF0

Aegis is keeping its mandate to make sure everything is secure on-chain as well as off-chain.

We will continue on collaborating with the leading auditing firms on smart contract and opsec side.

The Sherlock @sherlockdefi collaborative audit of the Aegis V2 contracts is complete.

No critical issues were found. Severity counts: 0 High, 0 Medium, 2 Low.

All Sherlock recommendations have been implemented in the final commit. The audited Aegis contracts are safe.

Full audit report: https://t.co/Ow65tnVeZR

Aegis holds zero exposure to rsETH or any Kelp DAO assets across YUSD and jUSD backing.

Our team is tracking potential second-order market effects and will communicate promptly if anything material emerges.

As always, our collateral and positions are fully transparent and verifiable in real time: https://t.co/tRbjZlnwDr

8/ Institutional LPs have been stuck in these funds for years. Can't exit. Getting half the returns they were promised. Marks nobody can verify.

Now the same assets are being packaged for crypto markets.

That's not democratization of finance. That's a distribution problem being solved at your expense.

So the real question — can crypto actually fix this, or is it just a better-looking wrapper?

1/ Crypto is going all-in on tokenizing private credit and private equity.

BlackRock, Apollo, KKR, Franklin Templeton — everyone's building on-chain wrappers for these assets.

Before you ape in, you should understand what's actually inside. 🧵

7/ So back to tokenization.

The pitch is: "these assets are finally liquid and accessible to everyone, on-chain."

But tokenization doesn't make a Level 3 asset less illiquid. It doesn't make an unverifiable NAV more real.

It doesn't fix gated redemptions.

It just finds a new buyer.