KRA wants a share of dowry money.

There is a guy called Kamau.

When it was time to buy his wife, he mobilized his most monied buddies.

He put them in a WhatsApp group. The fundraising began.

Those boys were loaded. They were only 35.

By by the time they were done, they had contributed 4.5 million shillings.

Others who were not in the group wired money directly to Kamau's bank account.

The ruracio D-Day arrived.

And as always, the one and only Kikuyu ruracio anthem was tuned.

🎶 Wero... Werokamu guku kwa wa Kanini... Werokamu... 🎶

Before they could finish the song, more than 2,000 people had pulled up.

Wakaanza kutoa funjo. Then one man stood on a stool and announced they could not sit until they had given Kamau top up money to add to the dowry.

The donation book was hurriedly brought. People lined up. Cash started flowing.

By the end of the day, another 2.8 million shillings had been raised.

Kamau took the money and banked it.

Total dowry contribution sitting at his bank account: 8m shillings.

The ceremony became the talk of Gatundu South.

Kamau paid his dowry. Collected his wife. And went home peacefully.

• Lesson 1. Monied friends are good for paying dowry.

I have no clue how. But sometime later, Kamau was marked for a KRA tax audit.

KRA went straight for his bank statements. They found deposits of 8 million shillings.

Immediately, they baptized the entire amount as undeclared taxable income.

Then demanded: 30% income tax. Penalties plus interest.

Total bill: 2.5 million shillings plus.

When Kamau saw the tax bill, he went mad.

He could try to talk but words would not come out. He nearly swallowed his tongue.

When he came back to real life. He shipped a protest letter to KRA.

He explained the money was dowry contribution from his family, friends and well wishers.

- He produced WhatsApp group fundraising screenshots.

- He produced RTGS confirmations.

- He produced the donation book.

- He even produced videos of the ceremony.

Including footage of the Werokamu song.

KRA could not hear any of it. They only wanted 2.5 million.

When Kamau realized KRA was not playing, he ran to court.

He told the Tribunal:

- My lord, look. I have shown KRA where the money came from.

- I have shown KRA who contributed it.

- I have shown KRA the ceremony.

- What more do they want from me?

KRA responded.

And what they said nearly made the judges fall off their chairs.

They argued the evidence was not convincing.

Why?

• Because the 2,000 plus donors had not sworn affidavits confirming that the money they gave was a donation and not payment for goods or services.

The Tribunal looked at the matter in amusement.

Then ruled.

- Kamau had discharged his burden of proof in full.

- KRA had acted unreasonably by ignoring and disregarding the substantial evidence he provided.

- And most importantly: Income tax is a tax on income. It is not a tax on every deposit appearing in a bank account.

The Tribunal found that KRA was wrong to treat all bank deposits as taxable income without first removing proven non income items such as dowry contributions.

The tax demand was killed.

Kamau won.

KRA retreated to Times Tower. And rested.

Case closed.

• Lesson 2.

- Document everything.

- KRA will push. Push hard.

📍 Live from the @NSE_PLC earlier today

A defining moment for Kenya’s capital markets and housing finance.

Today, @kmrc_co listed its KES 3 Billion #SustainabilityBond, marking a major step in mobilizing long-term capital for affordable and sustainable homeownership.

The Note received applications worth KES 9.38 billion, signaling strong investor confidence in @kmrc_co's mandate to promote sustainable homeownership.

#KMRCxNCBA #KMRCSustainabilityBond #NCBABankingOnBelief

INSTEAD OF WATCHING AN HOUR OF NETFLIX TONIGHT.

This 1 hour Stanford lecture by Joel Peterson will teach you more about negotiation and getting what you want than most people learn in years.

Bookmark it and give it an hour, no matter what.

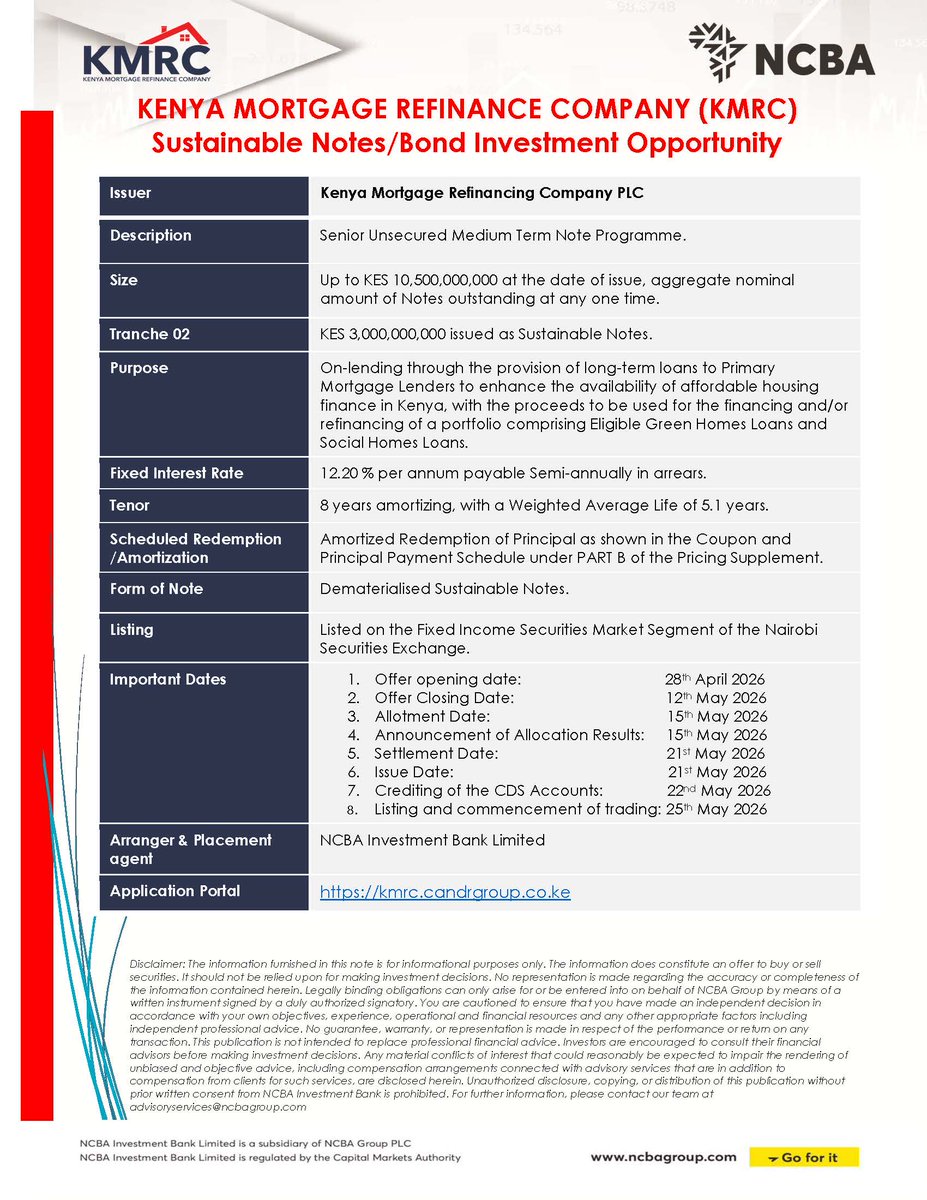

Invest in KMRC’s Sustainable Notes Tranche 02 and support affordable, green & social housing in Kenya.

Key Features;

✅ 12.20% p.a. paid semi-annually in arrears

✅ 8‑year amortizing

✅ KES 3B issued | NSE listed

🗓 28 Apr–12 May 2026

https://t.co/rhvkjigEgE

#KMRC #SustainableFinance #AffordableHousing #NSE

⏳ Closing Soon!

@kmrc_co job applications close on March 27th — don’t wait till the last minute!

If you’re ready for a role that drives real impact in Kenya’s housing finance space, this is your chance.

➡️ Head to our careers portal and submit your application today 👉 https://t.co/QggUnq0ByV

TRUMP: "This was our last, best chance to strike what we're doing right now and eliminate the intolerable threats posed by this sick and sinister regime."

"We're annihilating their navy. We've knocked out already 10 ships. They're at the bottom of the sea."

"We're ensuring that the Iranian regime cannot continue to arm, fund, and direct terrorist armies outside of their borders."

This is the story of how I cleared a 10-year mortgage in 2 years

In the year 2000, I signed for my first mortgage KSh 2.7 million, repayable over ten years, with a monthly installment of about KSh 37,000. At the time, it felt significant but manageable. Like many young professionals, I believed the difficult part was getting approved. Once the bank said yes, I was ready to sit back and relax knowing that in 10 years i will be a home owner.

That is what traps most people.

When many people secure a mortgage, they celebrate the approval rather than confront the obligation. They upgrade furniture, expand their lifestyle, and slowly adjust their expenses until the monthly payment blends into routine existence. Ten years quietly becomes normal. The loan stops feeling temporary and starts feeling permanent.

I had a mentor who refused to let that happen. Stewart Henderson, who was serving as CEO of Old Mutual at the time told me something that permanently changed my understanding of debt: a mortgage is not a commitment it is an emergency.

Then he introduced a rule that, at the time, felt extreme. Every month I earned commissions, I had to bring my statement to him before spending any money. We would sit down together and allocate it.

The bank required KSh 37,000.

Stewart ignored that number.

Instead, he focused on capacity. Whenever income rose, payments rose. Whenever earnings improved, we attacked the loan. He called it 𝐟𝐢𝐧𝐚𝐧𝐜𝐢𝐚𝐥 𝐚𝐠𝐠𝐫𝐞𝐬𝐬𝐢𝐨𝐧, treating debt as something to eliminate quickly rather than manage comfortably.

The first few months were uncomfortable. The natural instinct after earning more money is to reward yourself. Income creates a feeling of entitlement to enjoy what you worked hard for. But discipline does not negotiate with feelings. Every additional shilling was assigned before it reached my pocket.

Something surprising happened. As my income grew, but my lifestyle did not.

Because expenses stayed controlled, every increase in earnings accelerated repayment. The balance started shrinking visibly not yearly, but monthly. What had been structured as a ten-year obligation began to feel temporary.

Two years later, I made the final payment.

Now here’s the surprise, after I serviced the mortgage to completion, my mentor did not congratulate late me. He simply told me to start looking for the next property.

Most people follow a familiar sequence: earn, spend, then save what remains. I learned to earn, allocate, then live on the balance. The house was not paid off by income alone; it was paid off by priority.

Over the years, advising many individuals, I have noticed a consistent pattern. Nearly everyone wants financial freedom eventually, but very few accept financial discipline immediately. The distance between the two is not measured in years it is measured in habits.

Your path does not have to begin with a mortgage. In fact, for many people the smarter starting point is elsewhere, structured savings & investments, or disciplined accumulation strategies that eventually position you for homeownership without pressure.

Check out my latest article: From Tragedy to Prevention: Building Precautions, Regulatory Compliance, and the Case for Environmental Social Risk Management (ESRM) in Construction https://t.co/ATglRjIZ1H via @LinkedIn

Nokia CEO ended his speech saying this “we didn’t do anything wrong, but somehow, we lost”.

During the press conference to announce NOKIA being acquired by Microsoft, Nokia CEO ended his speech saying this “we didn’t do anything wrong, but somehow, we lost”.

Upon saying that, all his management team, himself included, teared sadly.

Nokia has been a respectable company. They didn’t do anything wrong in their business, however, the world changed too fast. Their opponents were too powerful.

They missed out on learning, they missed out on changing, and thus they lost the opportunity at hand to make it big.

Not only did they miss the opportunity to earn big money, they lost their chance of survival.

The message of this story is, if you don’t change, you shall be removed from the competition.

It’s not wrong if you don’t want to learn new things. However, if your thoughts and mindset cannot catch up with time, you will be eliminated.

Conclusion:

1. The advantage you have yesterday, will be replaced by the trends of tomorrow.

2. You don’t have to do anything wrong, as long as your competitors catch the wave and do it RIGHT, you can lose out and fail.

3. To change and improve yourself is giving yourself a second chance.

4. To be forced by others to change, is like being discarded.

5. Those who refuse to learn & improve, will definitely one day become redundant & not relevant to the industry.

They will learn the lesson in a hard & expensive way

#IkoKaziKE

President Trump just hosted a press briefing at the White House.

One by one, Trump and Pam Bondi delivered major announcements and clues on what's coming next—directly to the American people.

Here’s everything you should know (and no joke, it gets crazier the further you read):