عيدكم مبارك وكل عام وأنتم بخير 🌙

Wishing you and your loved ones a blessed and joyful Eid, filled with peace and prosperity

#EidMubarak#عيد_مبارك#Fatra

Private credit in 2025:

→ Hundreds of pages of legal agreements

→ Borrowing base calculated in spreadsheets

→ PDFs emailed to paying agents

→ Days (sometimes weeks) for a single drawdown

Making credit programmable = encoding those rules into smart contracts so the ops execute automatically.

The legal agreement stays. The manual work disappears.

Full episode with the amazing @cryptoreine 👇

https://t.co/usjsRFPW2I

TradFi allocators don’t need another pitch deck.

They need:

→ Risk tranching that fits legacy portfolio frameworks

→ Verifiable collateral data (not self-reported)

→ Real secondary market liquidity

→ Fraud & double-pledging mitigation they can audit

That’s what determines cost of capital in tokenized SME credit.

Full podcast with @cryptoreine dropping soon. 👀

#Fintech #TokenizedCredit #GCC

👉🏼 2%.

That’s how much bank lending GCC SMEs receive and despite being the backbone of the regional economy.

Across MENA, the number is slightly better at 8%. But with a $210–240B financing gap, “slightly better” doesn’t cut it.

The money exists. The businesses exist. The infrastructure connecting them doesn’t yet.

Source: World Bank / Union of Arab Banks

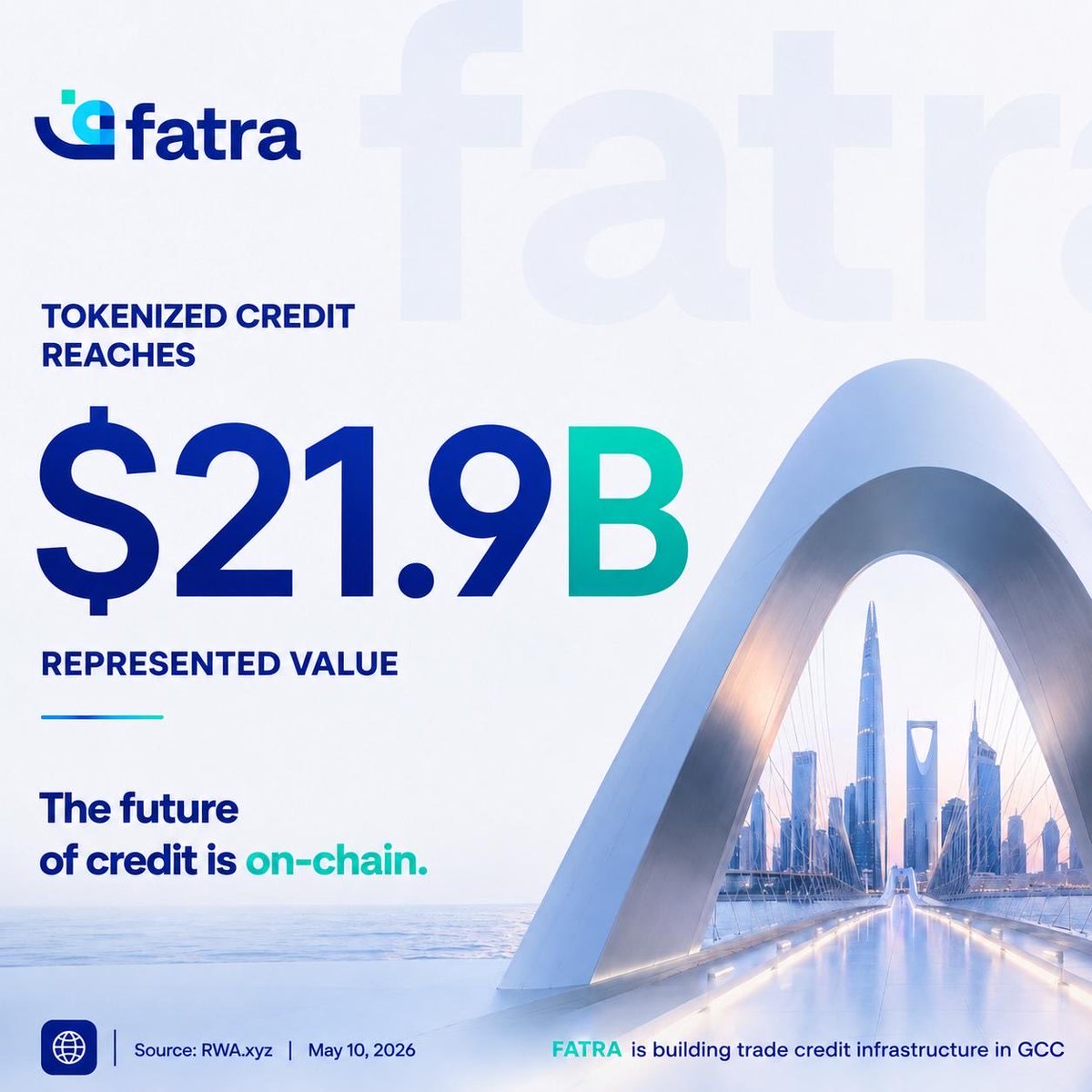

Tokenized private credit continues to mature as one of the strongest real-world asset segments in digital finance.

With represented value reaching $21.9B, the market is steadily moving toward more efficient, transparent, and globally accessible credit infrastructure.

At FATRA, we are focused on building institutional-grade trade credit infrastructure for SMEs across the GCC.

Source: https://t.co/rwke53g2XT

Private credit is quietly becoming one of the most active sectors in onchain finance.

The latest data from Pantera Capital State of Tokenization report shows private credit leading DeFi utilization at 64.3%, highlighting how capital markets are gradually moving toward more composable and programmable infrastructure.

A new market structure is emerging. Fatra is building with that direction in mind.

Everyone’s celebrating $27B in tokenized RWAs. Here’s what the data actually shows:

In 4 out of 5 asset classes, 89%+ of value sits in the top 5% of wallets.

Most of it never moves.

• The average tokenized Treasury holder transacts once every 6 months. Alt funds even less. These assets are minted, allocated, and held. No collateral. No lending. No composability. Just a better-looking spreadsheet entry.

• The one exception? Tokenized equities. $566 average transfer. Nearly 2M transactions per month. Retail is already here, just not where anyone expected.

• This reveals the real gap in RWA markets today. Tokenization solved issuance. It hasn’t solved utility.

An asset that earns yield in a wallet but can’t be posted as collateral, borrowed against, or moved between protocols isn’t a financial instrument. It’s a record of ownership.

The $400T opportunity doesn’t unlock when more assets get minted. It unlocks when existing ones start working. That’s the infrastructure layer FATRA is building toward.

New podcast is LIVE

In the 6th episode of the Fatra Protocol Podcast we are joined by Mr. James Ross to discuss the evolution of blockchain high-net-worth (HNWI) capital and how it is positioning itself within Real-World Asset (RWA) markets and tokenized financial infrastructure.

Watch now on YouTube: https://t.co/V6qmAFD4EI

Fatra is pleased to announce the signing of a Memorandum of Understanding (MoU) with Agama Finance (@agamafinance), establishing a framework to explore potential collaboration in the development of liquidity solutions for tokenized private credit.

The discussions between both parties will focus on evaluating mechanisms that could enhance capital efficiency for liquidity providers (LPs), including the possibility of enabling access to liquidity against tokenized positions, subject to further structuring, technical alignment, and regulatory considerations.

This engagement reflects a shared interest in advancing institutional-grade infrastructure within the tokenized asset space. Both parties will continue to assess areas of alignment and feasibility before any formal integration or implementation is pursued.

Further updates will be communicated as discussions progress.

Everyone talks about regulation as the biggest RWA bottleneck. But the data points elsewhere.

Today, $313B+ in stablecoin liquidity already sits onchain, while tokenized RWAs remain a fraction of that capital base.

Demand may not be the constraint. Liquidity design may be. Here’s the problem: Traditional assets often operate with T+2 settlement, gated redemption windows, or periodic liquidity events.

Onchain markets operate 24/7/365, that mismatch creates friction and this friction kills secondary markets. Meanwhile, projections point to $18.9T in tokenized assets by 2033. That scale doesn’t happen without better liquidity rails.

Which is why attention is shifting toward new infrastructure primitives like NAV-based vault models and programmable redemption mechanisms.

Most people assumed the first major RWA breakthrough would be spot ownership.

The @Securitize data suggests otherwise: RWA perpetuals grew 40x in six months, while broader onchain derivatives contracted. Their share of total onchain derivatives volume climbed from 0.1% to 10%. Some projections now point to 50% by 2028.

That signals something important: Markets may prefer access before ownership.

Before investors want to hold tokenized real-world assets directly, they may first want to trade exposure to them. That changes how this market develops.

It suggests the first scalable RWA opportunity may emerge through:

synthetic exposure

derivatives liquidity

leveraged market access

programmable market structure

The implication is bigger than volume growth. It may mean RWA adoption starts through trading rails, not asset wrappers. That’s a very different future.

FATRA is paying attention to where the market is actually forming.

The AMA on Wednesday was a blast.

We broke down how FATRA is building SME credit infrastructure in the GCC, connecting SMEs, banks, insurers, and global investors through tokenized credit pools.

SMEs in the region still face major financing gaps, while traditional banks struggle to efficiently serve this segment. FATRA solves this by structuring SME loans into transparent, risk-managed pools accessible to global capital.

Tokenization sits in the background to reduce friction and unlock liquidity, while SMEs continue using familiar financial tools.

Big thanks to everyone who joined. More sessions coming soon.

Re-listen now: https://t.co/r0xDqHzNLq

We’re live today at 4:30 PM for an AMA on Organizing SME Credit: From Traditional Structures to Tokenization.

Join us as we unpack what Fatra is building, why it matters, and how tokenized credit can reshape SME lending.

Speakers:

Khaled AlHadramy

Meshari Al-Munaikh

Dr. Mehdi Alizadeh

See you there.

https://t.co/CyrsMBY48Z

Reminder: AMA Today at 4:30 PM

“Organizing SME Credit: From Traditional Structures to Tokenization”

We’ll break down:

– What Fatra is actually building

– Why it matters now

– How tokenized credit fits into the bigger picture

Speakers:

Khaled AlHadramy

Meshari Al-Munaikh

Dr. Mehdi Alizadeh

If you care about where real-world finance meets crypto — this one’s worth your time.

Don’t miss it. See you there.

Not all credit behaves the same.

SME trade credit is short-duration by nature — measured in weeks or months, not years.

This fundamentally changes how risk, liquidity, and capital allocation should be approached.

Short duration isn’t a weakness.

It’s a structural characteristic.

Important; unfortunately, our guest speaker Tomer Bariach will not be able to attend the upcoming AMA. We will invite him next time.

See you at the event!

AMA this Wednesday, 4:30 PM!

“Organizing SME Credit: From Traditional Structures to Tokenization”

Intro session: what Fatra is building, why it matters, and where tokenized credit fits.

Speakers:

Khaled AlHadramy

Meshari Al-Munaikh

Dr. Mehdi Alizadeh

Guest: Tomer Bariach

Don’t miss it. Stay tuned and see you soon!

Everyone is talking about RWA. Almost no one is talking about how it actually works.

The real engine is institutional liquidity in tokenized credit: slow, constrained, and completely different from retail flow.

Episode 05 of the Fatra Protocol Podcast with Martijn Pullen goes into the mechanics behind it, not the marketing around it.

Watch: https://t.co/qGYU0pCqXd