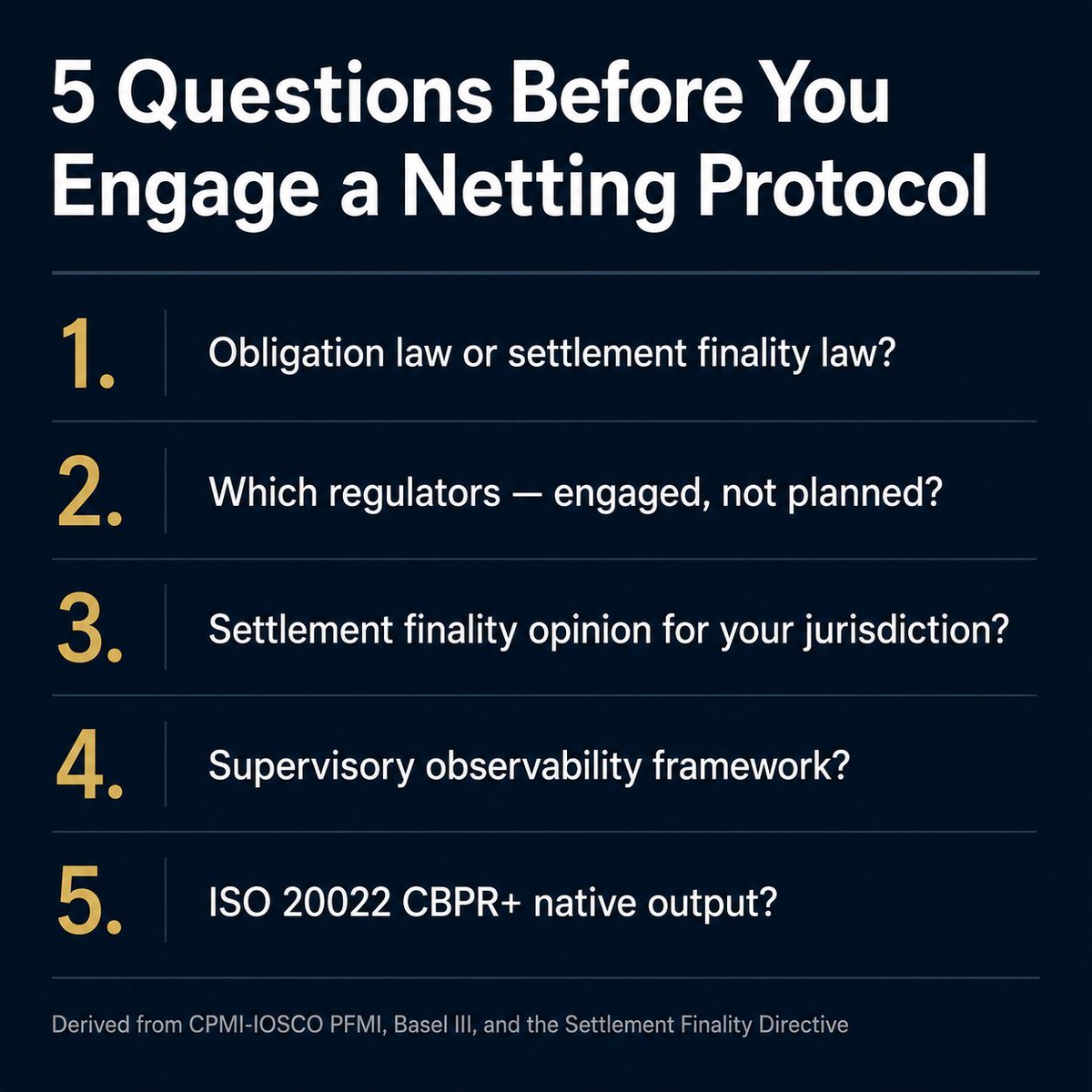

Five questions every bank should ask before engaging with a netting protocol.

These aren't proprietary criteria. They're derived from CPMI-IOSCO PFMI, Basel III, and the Settlement Finality Directive. They apply to any netting infrastructure, regardless of the underlying technology.

1. Under what legal framework does the netting operate — obligation law or settlement finality law?

The threshold question. The answer determines enforceability in insolvency, supervisory treatment, and whether your legal team can issue an internal approval.

2. Which regulators has the operator engaged, and in what capacity?

Active engagement — not "we plan to engage regulators eventually." Sandbox applications. Formal supervisory dialogue. Innovation hub conversations. Infrastructure that deliberately avoids financial regulation is not designed for institutions whose regulators expect to know what settlement systems you use.

3. Is there a settlement finality opinion for your jurisdiction?

PFMI Principle 8. Legal opinions confirming finality are expensive, jurisdiction-specific, and time-consuming. Their absence is a red flag no amount of technical sophistication can offset.

4. Can your supervisor access the infrastructure under a defined observability framework?

Central banks expect to see positions, risk exposures, and compliance decisions. If the infrastructure can't provide tiered, scoped, auditable access to supervisory authorities — your institution can't use it at scale.

5. Are settlement instructions generated in ISO 20022 CBPR+ format natively?

After the November 2025 CBPR+ migration, this is the institutional standard. Net settlement instructions that require format translation introduce operational risk your operations team will not accept.

Pass/fail. If the protocol you're evaluating meets all five, it was built for institutional adoption. If it meets some — it may be built for a different market.

Full analysis: https://t.co/yxDZpA7O1e

#SettlementNetting #MultilateralNetting #InstitutionalClearing #PFMI #Compliance #SettlementCompression #ISO20022

Set-off is not settlement netting.

One operates under private obligation law. The other operates under financial regulation — with settlement finality, supervisory observability, and Basel-relevant capital treatment.

Both involve reducing what participants owe each other. Both can use the same family of graph-based mathematics. Both produce a smaller set of residual positions than the original gross obligations.

They are not the same thing.

Set-off under the UNIDROIT Principles discharges mutual obligations by notice. No regulatory licence. No supervisory engagement. No settlement finality in the PFMI sense. No enforceability in insolvency beyond what general obligation law provides.

That works for trade credit. It works for invoice clearing among SMEs. It has worked in Slovenia since 1991.

It does not work for banks.

When a regulated institution evaluates netting infrastructure, the first question is not "what algorithm do you use." It is: "under what legal framework does this netting operate — and can my compliance team approve it?"

Settlement finality. Supervisory observability. Regulatory engagement. ISO 20022 native output. Enforceability in insolvency.

If your netting protocol doesn't address these, you're building something useful — but you're not building institutional settlement infrastructure.

I wrote about this in detail: the legal distinction, the five questions every bank should ask, and why the framework matters more than the algorithm.

https://t.co/yxDZpA8lQM

#SettlementNetting #MultiateralNetting #FinancialInfrastructure #PFMI #ISO20022 #SettlementCompression #InstitutionalClearing

StableNet is live on testnet.

24/7 against a permanent soak of 14 participants spanning the institutional topology of regulated stablecoin issuers, Tier-1 banks, payment network operators, qualified custody, and compliance infrastructure — submitting obligations across the live tri-corridor (USDC by @circle , XSGD, RLUSD on chain).

Most recent window close: 3.99:1 multilateral compression. 75% capital reduction. Gross 624,013 USDC compressed to net 156,386 USDC, with chain Merkle roots, RFC 6962 IVMS Travel Rule Merkle roots, and per-partner ISO 20022 pacs.008 messages all auditable end-to-end.

Peak compression observed across closed windows: 10.23:1 — ~90% capital reduction.

24-hour rolling stats: 2,662 obligations processed. 521 net settlements. 565 compliance checks — zero denies.

Five live products on one @avax L1: Settlement · PayNet · AssetNet · RiskNet · StableNet.

What's different about FiatRails — architecturally:

→ Multilateral netting across stablecoin issuers (USDC, EURC, USDT, PYUSD, XSGD, RLUSD, USDPT) in one corridor — no other wholesale settlement network addresses the stablecoin-issuer landscape this way.

→ Configurable netting windows (10-min cadence on testnet today) — explicit capital-efficiency optimisation, not real-time per-transaction settlement.

→ Compliance-gated jurisdictional issuer selection — OFAC SDN and multi-framework rules live.

→ Travel Rule (IVMS101 + RFC 6962 Merkle) + ISO 20022 pacs.008 end-to-end.

→ Non-custodial — settlement assets stay with the issuer or custodian; FiatRails coordinates the netting.

Active institutional engagement across multiple jurisdictions and sandboxes. Operational evidence available for verified institutional review on request.

Multilateral netting built for regulated rails. Live. Verifiable.

https://t.co/yQrdRAU0Wh

#Stablecoins #SettlementInfrastructure #DLT #MultilateralNetting #Avalanche

CLS monitors member positions. DTCC scores member portfolios. Every CCP in the world calculates margin from clearing data.

None of them score risk at the netting cycle level.

That's the gap.

Settlement systems manage risk at the member level — position limits, pay-in schedules, margin requirements. They answer "is this member risky?" They don't answer "is this counterparty, in this corridor, in this netting cycle, risky?"

That data only exists inside the protocol that processes the obligations.

FiatRails RiskNet is a protocol-native risk layer that scores per counterparty, per corridor, per netting window. Risk metrics generated from the settlement engine's own data, not imported from agencies or vendors.

Counterparty showing elevated risk across multiple corridors? Flagged before their next obligation enters the netting cycle.

Corridor showing concentration risk relative to its historical pattern? Flagged in real time.

Participant's net exposure diverging from their pre-netting gross? That spread is a scored risk signal that feeds admission control.

The netting engine sees something no external risk vendor can: the difference between what participants owe gross and what they owe net. That spread — per counterparty, per corridor, per cycle — is a risk signal that doesn't exist anywhere else.

Live on testnet.

https://t.co/NqPFIDNsCy

#SettlementInfrastructure #RiskManagement

Six weeks ago, FiatRails had zero regulatory engagement.

Today we've engaged 9 regulators across 4 continents:

Singapore. UAE. Bahrain. Luxembourg. Brazil. UK (FCA + Bank of England). Netherlands. Lithuania.

One of them reviewed our model and confirmed we don't require a financial licence — our technology layer sits beneath the regulated perimeter, not inside it. That's not a workaround. That's architecture.

We didn't wait for product-market fit to start regulatory conversations. We went early, because in settlement infrastructure, the regulator IS the customer's gatekeeper.

Every engagement followed the same pattern:

— Here's what we do (multilateral netting for cross-border settlement and tokenized asset markets)

— Here's what we don't do (we don't hold funds, transmit money, or custody assets)

— Here's what we'd like to explore (sandbox programmes, innovation hubs, pilot regimes)

The responses have ranged from "come talk to us" to "this has significant implications for RTGS and CBDC."

If you're building financial infrastructure and NOT talking to regulators, you're building a demo, not a company.

#CrossBorderPayments #FinancialInfrastructure #Regulation

Every major settlement system in the world does bilateral netting.

CLS. Partior. CHIPS (until the final step). SWIFT gpi.

Bilateral means two banks net their positions against each other. If Bank A owes Bank B $10M and Bank B owes Bank A $8M, they settle the $2M difference. Simple. Obvious. And it leaves enormous amounts of money on the table.

Here's why.

Imagine Bank A owes Bank B $10M. Bank B owes Bank C $10M. Bank C owes Bank A $10M. Bilaterally, each pair still settles $10M in each direction. Zero compression.

Multilaterally? The circle cancels completely. $30M gross becomes $0 net. 100% compression. Nobody moves a dollar.

This isn't theoretical. On our testnet, multilateral netting across 11 corridors compresses $2.9B gross to 95% reduction. CLS publishes 92% on their best days, and they serve exactly 75 members.

The reason bilateral dominates isn't that it's better. It's that multilateral netting is computationally hard to do in real time, across jurisdictions, with privacy, with regulatory compliance, at the speed institutions require.

That's the engineering problem we solved. Consensus-layer netting with cryptographic privacy, running deterministically inside the block validation pipeline. Not a smart contract. Not an off-chain engine. A virtual machine built for this.

Bilateral is the floor. Multilateral is the ceiling. The gap between them is where trillions sit idle every day.

Introducing PayNet — 577,884 obligations settled. Privacy mode: COMMITTED.

The FiatRails Settlement Computer is built as six interlocking products on a single sovereign Avalanche L1. Today I'm sharing one of them: PayNet.

PayNet is the micro-transaction aggregation layer. High-frequency payment flows — remittances, merchant settlements, mobile money — generate

thousands of small obligations that would overwhelm traditional netting windows. PayNet aggregates these into settlement-ready positions before they reach the multilateral netting engine.

No system globally performs multilateral netting on micro-transaction flows. Deployed netting infrastructure (CLS, Partior, Fnality) is exclusively wholesale. Remittance and mobile money providers settle gross or simple bilateral. PayNet bridges this gap — on encrypted values. Patent pending.

Every obligation is committed using Pedersen cryptographic commitments with Bulletproof range proofs. The netting engine never sees plaintext

amounts.

What you're looking at:

- 6 corridors processing West and East Africa flows

- 577,884 obligations settled on-chain

- 837,982 AI-powered format translations (legacy MT → ISO 20022 CBPR+)

- 503 post-quantum verifications (ML-DSA, FIPS 204)

- Compression: 85–95.5% per corridor

- Running 24/7 in committed mode

Learn more: https://t.co/vs5CvVKRRe

PayNet sits alongside Settlement, RiskNet, Trade, Grid, and Nexus — all sharing one chain, one compliance layer, one privacy stack.

This isn't a demo. It's a perpetual soak test running for weeks. Settlement infrastructure should prove itself before it asks for trust.

#Settlement #CrossBorder #Avalanche #Blockchain #Fintech

95% netting compression. Proven on testnet. Not a projection.

We just closed our largest test cycle on Lagrange (our Avalanche L1 testnet):

- $12.13B gross obligations processed

- 95% compression — meaning 95 cents of every dollar netted out before settlement

- 11 live corridors across USD, AED, NGN, GBP, EUR, KES

- 434 cross-corridor netting rounds

- 23,000+ obligations through PayNet alone

For context, CLS — the $7T/day settlement utility used by the world's largest banks — publishes 92% compression. They serve 75 direct members. We're building for the other 38,000.

What does 95% compression actually mean for a bank?

A corridor processing $100M/day in gross obligations settles just $5M. The other $95M never moves. No nostro funding required. No trapped capital. No correspondent chain.

This isn't theoretical. Every number above comes from our live testnet — real netting windows, real multilateral offset calculations, real settlement instructions generated.

The settlement layer works. Next step: institutional pilots under regulatory supervision.

Here's the next question every institution asks: "If I put my settlement data into a shared netting engine, who else can see it?"

It's the right question. In a multilateral netting system, the engine needs to see all obligations to compute optimal nets. But your volumes, your counterparties, your growth rate, your corridor mix — that's competitive intelligence. No bank or PSP will put that on a chain where competitors or validators can observe it.

CLS solves this by being a trusted black box. You trust CLS because it's regulated and systemically important. That's privacy by policy.

We solved it with cryptography.

The FiatRails privacy layer — deployed and verified on all 11 testnet corridors:

- Pedersen commitments (BN254) for obligation amounts — homomorphic, so the netting engine computes on encrypted values without ever seeing them

- Bulletproofs for zero-knowledge range proofs — 70ms proving, no trusted setup

- AES-256-SIV for metadata encryption — counterparty addresses, transaction IDs, all encrypted at rest

- Shamir's Secret Sharing for master key distribution — no single validator can access the data

- Tiered view keys: governance sees everything, central banks see their corridor, participants see only their own data

- Participant-sovereign delegation: you control who sees your data, with granular scoping, time limits, and instant on-chain revocation

This is not "privacy by policy." It's privacy by mathematics.

The first netting system globally where institutions can trust the engine without trusting each other.

Built on a sovereign Avalanche L1. Post-quantum authentication (ML-DSA, FIPS 204) already deployed — because settlement records have 20-year retention requirements.

Monday: the compression numbers.

#CrossBorderPayments #Privacy #ZeroKnowledge #Avalanche #Settlement #Fintech

Here's the problem nobody's solving for 99% of financial institutions.

Every day, $4.7 trillion sits trapped in nostro and vostro accounts around the world. That's capital banks park overseas just so they can settle cross-border payments. Not earning. Not deployed. Just sitting there, waiting.

CLS — the closest thing to a solution — serves 75 member banks. Seventy-five. There are 38,000+ banks globally, thousands of PSPs, hundreds of fintechs processing cross-border flows. They all settle bilaterally. Slowly. Expensively. With trapped capital on both sides.

It gets worse. 83% of African currencies have zero payment-versus-payment settlement coverage. No netting. No compression. Every transaction settles gross. A $10M corridor between two PSPs requires $10M in pre-funded capital — on each side.

Multilateral netting changes this. Instead of every party settling every obligation individually, a netting engine calculates the minimum set of payments needed to settle everyone's positions simultaneously. $100M gross becomes $9M net. Capital freed. Risk reduced. Settlement in minutes, not days.

This is what CLS does for 75 banks. This is what FiatRails does for everyone else.

The Settlement Computer is not a better rail. It's the first netting infrastructure built for the institutions that have been excluded from the existing one.

Yesterday I shared what we've built. Tomorrow I'll share how we protect it — cryptographic privacy that lets institutions trust a shared netting engine without exposing their data to

competitors.

#CrossBorderPayments #Settlement #Fintech #Africa #Blockchain #Avalanche

For the past 10 months, I've been building something that doesn't exist in global finance.

FiatRails is a Settlement Computer — a sovereign Avalanche L1 blockchain purpose-built for multilateral netting in cross-border settlement. Not a payments app. Not a stablecoin wrapper.

Not a routing layer.

The L1 is the application. Settlement logic executes as native precompiles at the consensus layer — not as smart contracts deployed on a general-purpose chain. 1,601 TPS on commodity

hardware.

Why it matters: $4.7 trillion sits trapped in nostro/vostro accounts every day. CLS — the world's largest settlement system — serves 75 members. The other 38,000+ banks, PSPs, and

fintechs settle bilaterally, slowly, expensively. 83% of African currencies have zero payment-versus-payment coverage.

What we've built and verified on testnet:

- 11 settlement corridors across Africa, Middle East, and Asia

- 91.2% netting compression on $12.13B simulated gross volume — $11.10B eliminated (CLS publishes 92%)

- 11 consensus-layer precompiles in native Go (10,800+ lines)

- Cryptographic privacy: Pedersen commitments, Bulletproofs, zero-knowledge range proofs — the first netting system globally to operate on committed values

- Post-quantum authentication deployed (ML-DSA, FIPS 204)

- PayNet: micro-transaction aggregation with AI-powered ISO 20022 translation, 23,000+ obligations processed

- 5 U.S. patent applications filed (~287 claims)

Six products. One chain. Built for the institutions that have been locked out of infrastructure that should have existed a decade ago.

We've been heads-down building. Time to share what exists.

More this week.

#CrossBorderPayments #Avalanche #Settlement #Blockchain #Fintech #Africa