Agree. Consensus issue seems to be revolved around memory price increases -> destroys already thin hardware margins -> thus Switch 2 price increase -> could hurt early adoption ~1 year in the new cycle -> later hurts software sales. Will dig in more and open to other viewpoints $NTDOY

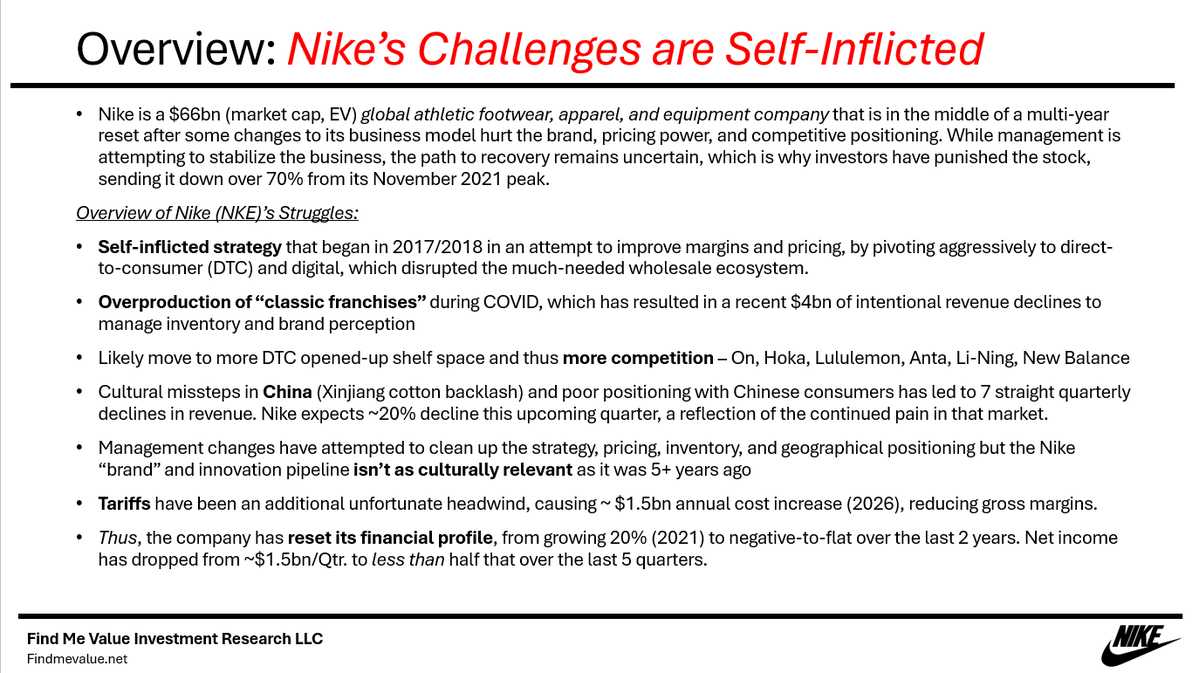

$NKE - Under Donahoe: pushed aggressively into DTC, hurt wholesale relationships, overproduction of classic franchises, less innovation. Brought in Elliott Hill (late 2024): rebuilding wholesale relationships, manage inventory (still working through Dunks), re-focus on running. Problem is - competitive landscape has changed, China is also a different market than it was 5 years ago. (Source: https://t.co/BqRnHjwjYq)

$NKE (Nike) - Despite their self-inflicted business struggles over the last decade, they have incinerated shareholder money, repurchasing over $32bn of stock at prices more than 2x current levels. (https://t.co/7yQEY1bjiG)

My $NKE deck will be out tomorrow. Long story short, and obviously reflected in their stock price - things have changed. A majority of Nike’s issues are self-inflicted, and there are many. They damaged the brand equity quite a bit over the last 5-7 years, allowing for more competition in all areas.

$LULU new 8-year lows

$NKE new 12-year lows

Retail research analysts built their entire persona pumping the “moat” of these two.

Here’s a lesson: Brands have no moat. They’re either getting hotter, or they’re cooling.

You win by observing at which stage the brand is at.

I'm saying it began almost 10 years ago with their strategy pivoting. The COVID-era spike in demand then subsequent freefall definitely added on to their issues, in a large way, as it made them believe their strategy was "working", although it was a spike in demand from a once-in-a-lifetime situation.

$CMCSA showing life. Resi broadband net loses improving by 117,000 y/y to 65,000 net loss, while domestic wireless net adds +435k (best quarterly result on record).

Some replies referencing Combs / $AAPL. Possible it was a "dual contribution" by Combs and Weschler, but there was discussion in 2016 in a German magazine "Manager Magazin" whereby Weschler discusses AAPL. At the time there was only a $1bn AAPL investment, Buffett said it wasn't his. Weschler goes into detail about how he has followed the company for "a long, long time." https://t.co/gWtoxxC5QQ

As of YE2013, Combs and Weschler each managed more than $7bn. By mid-2018, they each managed "$12bn to $13bn".

As of YE2025, Combs managed around $15bn, assuming similar to Weschler.

From YE2013 - now, S&P 500 +284% (ex-divs), which would put $7bn (ye'13) to $26.9bn.

Is this the reason there hasn't been more discussion around their performance, likely no added responsibilities from the $BRK portfolio, and why CEO Greg Abel will manage the other ~94% still. [Weschler will manage about 6% of holdings - WSJ]

Finishing up $NKE work; anyone have a better feel and understanding of NKE positioning and issues in China? All other luxury brands, performance wear, lifestyle brands are doing either “ok” to “great”. NKE an outlier to the downside. How has Anta / Li-Ning compete as well, as they are gaining market share? Any insight is appreciated