In SCF, the anchor corporate is the real credit signal, not just the borrower.

But most LMS platforms only track borrower-lender relationships, pushing anchor-level limits into spreadsheets.

Check out, 4 gaps NBFCs often overlook:

https://t.co/FeHcoE7pxY

#Finezza#SCF#NBFC

B2B BNPL needs real-time limit updates.

Most LMS platforms still process repayments in overnight batches.

So available credit lags behind actual repayments, creating friction for buyers, suppliers, and ops teams.

https://t.co/Vj1u9UlHbT

#Finezza#B2BBNPL#NBFC

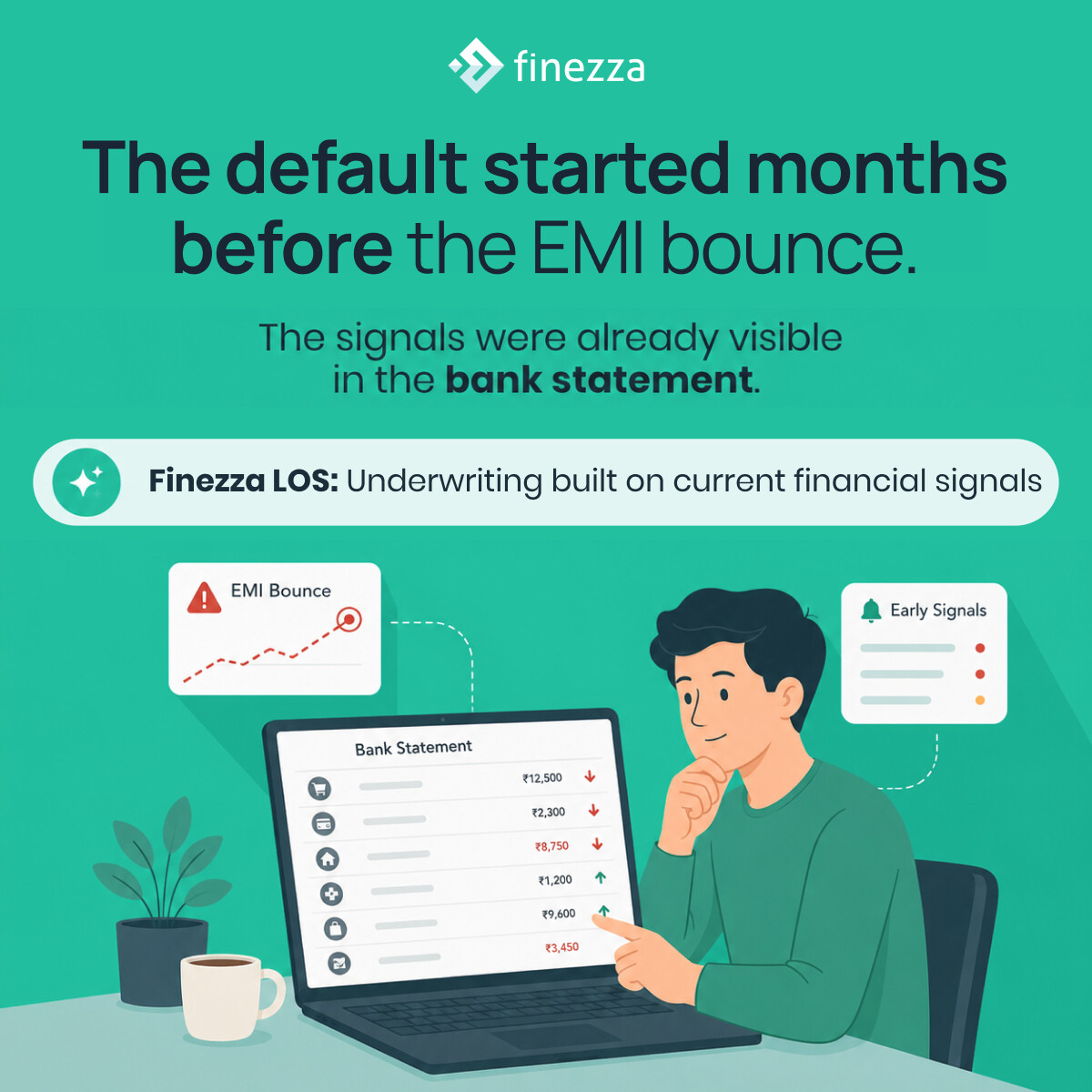

Most MSME defaults don’t start with missed EMIs.

The warning signs usually appear much earlier in cash flow and bank statement patterns.

Traditional underwriting often misses them.

Read more: https://t.co/naGnpa9YDC

#Finezza#CreditUnderwriting#MSMELending

Fixing a batch file mismatch by editing the file before upload leaves no audit trail.

The mapping error stays and recurs on every file after it.

Read our latest article to know how the LOS-to-LMS handoff quietly corrupts loan data:

https://t.co/hzGr0aqwo0

#Finezza#Loan

Most lending fraud is discovered in the collection queue.

The application data that flagged it was there at origination.

Read our latest article to know five LOS features that catch fraud before disbursement:

https://t.co/8CNMuRo1nh

#Finezza#LoanOrigination#FraudPrevention

OD and revolving credit on a term-loan LMS works at 20 accounts.

At 200, it produces DPD misreporting and bureau inaccuracies.

Read our latest article to know what a working capital-ready LMS actually needs:

https://t.co/XczodYlLlx

#Finezza#WorkingCapital#LoanManagement

Most lenders measure digital lending by speed. The real value is what data continuity makes possible across the loan lifecycle.

Read our latest article to know what lenders actually build when they invest in infrastructure:

https://t.co/XPSTyYjSjf

#Finezza#DigitalLending

The LOS-to-LMS handoff is where most lenders quietly lose data integrity.

Field mapping built at implementation can't handle products added later.

Read our latest article to know where loan data gets corrupted and what the fix looks like: https://t.co/hzGr0aqwo0

#Finezza

Credit team approves restructuring in 45 minutes.

Borrower gets the revised agreement 4 days later.

The decision isn't the bottleneck. Disconnected systems are.

Read our latest article to know where each day goes:

https://t.co/3Nkjl1B28A

#Finezza#LoanManagement

Bureau scores reflect past repayment.

Audited financials are 12-18 months old by appraisal time.

Neither tells you what is happening in the business today.

Read our latest article to know how credit underwriting closes this gap: https://t.co/naGnpa9YDC

#Finezza#MSMELending

Payment timing drift predicts defaults months before DPD buckets flag anything.

A borrower paying 5 days late, then 15, then 25 is deteriorating, even while staying "current."

Read our article to know which five credit bureau signals lenders miss: https://t.co/bq0B4z8kK7

Running BNPL on term loan LMS infrastructure?

Your credit limits update overnight. Your borrowers transact in real time.

Read our latest article to know why that gap breaks more than most lenders expect:

https://t.co/OWhQ1JLBiG

#Finezza#BNPL#LoanManagement#DigitalLending

400 invoices. 30 buyers.

Month-end, and LMS + CBS don’t match.

Partial payments, disputed invoices, manual reconciliations.

Bill discounting breaks when systems aren’t built for 3-party repayments.

Read more: https://t.co/FU6gRqbVna

#Finezza#BillDiscounting

Your co-lending partnership may go live next quarter.

But is your LOS ready?

If dual schedules, blended pricing, or NPA sync still need manual work, risk starts early.

Read our article comparing 8 LOS platforms for Indian lenders:

https://t.co/HhtDbQraLv

#Finezza#CoLending

A clean P&L means the business files its taxes correctly.

It doesn't mean the borrower will have cash when your EMI is due.

MSME underwriting built on financial statements alone has a structural blind spot.

Read our latest article to know more:

https://t.co/HvAUsGkeLJ

Loan officers don't see screen navigation as a cost.

But 7 clicks per query across 40 queries a day adds up to a massive operational bottleneck.

The fix isn’t faster clicking.

Read our latest article to know more:

https://t.co/vLbVkRxNAc

#Finezza#LMS#FinezzaCoPilot

Rule-based fraud detection was built for salaried borrowers.

MSME profiles look nothing like that.

Legitimate borrowers and fraudulent ones often look identical to a rule engine.

Read our article to know what AI catches instead:

https://t.co/C5buH8ou2o

#Finezza#MSMELending

NBFCs don't lose co-lending mandates over pricing.

They lose them over reconciliation delays, DPD mismatches, and bureau submissions that contradict what the bank reports on the same loan.

Read our article to know more:

https://t.co/JEJSXxFGch

#Finezza#CoLending#NBFC

At 2,000 loans, you manage around the gaps. At 20,000, the same gaps cost you.

Collections, DPD tracking, field attrition, compliance reporting. Five operational challenges that scale faster than your portfolio does.

Read our latest article to know more:

https://t.co/0vErmeSgnk

Most LMS failures aren't vendor failures. They're evaluation failures.

You tested the demo. You didn't test a failed eNACH + partial prepayment + bureau pull happening simultaneously.

4 mistakes lenders make when selecting an LMS: https://t.co/fL3zheREhK

#Finezza#LMS