Seeking asymmetric edges in quality growth & tech. Thoughts on markets, compounding, and rational investing amid noise.

NFA 👇 Follow for clarity, not hype.

Why AmpliTech $AMPG is More Than Just a Loud Earnings Report

Most retail investors look for growth on the top floors of the technology skyscraper.

It’s easy to miss what’s happening in the basement, where the actual infrastructure is built, without which those top floors would simply collapse.

Lately, I’ve spent a lot of time digging through SEC filings and conference call transcripts for AmpliTech Group ($AMPG).

Huge shoutout to my buddy @EhrmantrautCap_ putting this company on my radar and pointing out the fundamentals that the market is only just beginning to notice.

Instead of chasing the next overhyped trend, I prefer businesses with hard numbers and tangible technology.

Here is why I see a clear path to a deep rerating of the company.

1⃣A Core Business Driving the Engine

For years, AmpliTech was primarily known as a niche manufacturer of Low Noise Amplifiers (LNAs) and radio frequency (RF) components.

And that is their starting point.

This business isn't just doing well - it’s growing.

Look no further than the latest Q1 2026 report: gross margin roared back to a spectacular 48% (compared to 33% the previous year).

This proves that their traditional engineering products are highly sought after and high-margin assets.

⬇️But the real financial leverage lies in their order book, which is starting to burst at the seams:

🟢Operational Backlog: The company entered this period with contracted orders exceeding $20 million.

🟢Pipeline of Letters of Intent (LOIs): Management has framework declarations from Tier 1 operators sitting in their drawer totaling $118 million.

2⃣The CEO's Crucial Message: Patience Before the Rerating

This brings us to the most important takeaway from the recent Q1 2026 earnings call, which many investors interpreted too superficially.

CEO Fawad Maqbool explicitly communicated that the largest revenues from giant contracts will be heavily weighted toward the later quarters.

Logistics and deployments with Tier 1 telecom giants take time.

Before equipment is mounted on cell towers and revenue recognition occurs in the books, a significant gap exists.

What does this mean for us? The next report (Q2) might still show steady, quiet base-building, while the real financial fireworks will only show up in the Q3 and Q4 results.

This creates an ideal window of opportunity for patient investors - the real, fundamental rerating of the company will most likely occur in the second half of the year, when tens of millions from these LOIs and the projected guidance (management is targeting at least $50 million in revenue for the full year 2026) physically hit the company's accounts as paid invoices.

3⃣New Segments and a Massive Leap in SOM

What excites me most about AmpliTech is that their technology allows them to organically enter entirely new, massive target markets (SOM – Serviceable Obtainable Market).

🟢5G Open RAN (ORAN) with AI Integration:

Their Massive MIMO radio systems recently received official FCC certification in the US and ISED certification in Canada.

Moving from an expensive R&D phase to commercial distribution opens the wallets of enterprise clients, schools, and hospitals.

🟢Quantum Computing and Satellites (Cryogenic LNAs):

This is the hidden ace.

AmpliTech’s cryogenic amplifiers are critical for stabilizing signals in quantum processors, satellite communications, and defense applications.

As these industries scale globally, AMPG stands ready as a proven "picks and shovels" supplier.

4⃣A Word on Risk, Valuation, and My Approach

Let’s be clear - this is not a safe haven for retirement capital.

At its current market valuation (the market cap hovers around $110–$130 million), AmpliTech remains a classic micro-cap.

Stocks with such low capitalization come with massive volatility.

They are prone to huge swings - skyrocketing tens of percent on a single piece of news one day, only to give back a chunk of that move the following week due to a delayed delivery schedule.

The chart over the past few months (up over 140% in a 30-day window) illustrates this perfectly.

When it comes to official valuations, the Wall Street consensus (including Maxim Group) maintains a strong "Buy" recommendation with a price target of $7.00. Meanwhile, independent Discounted Cash Flow (DCF) mathematical models (such as those on Simply Wall St) peg the intrinsic value (Fair Value) around $5,99 (against a current price of ~$5.02), which still represents a double-digit discount.

To be honest?

My trust in analytical models and rigid DCF valuations in today’s market is highly limited.

In the bull market world driven by disruptive tech, Excel spreadsheets rarely keep pace with real-world dynamics.

Looking at the massive wave of revenue scaling up for H2, my personal expectations go beyond conservative investment bank reports.

Given proper execution and full conversion of their LOIs, I want to see a 2x on this stock price by the end of the year. The potential for such a powerful capital squeeze is absolutely there.

I am tuning out the noise and short-term trading around this stock.

My approach is strictly long-term. Following its recent capital raises, the company secured over $18.4 million in cash and is completely debt-free.

Liquidity risk has evaporated, and the operational fundamentals are the healthiest they have ever been.

For me, the path to the levels suggested by analysts is wide open, provided management executes on its pipeline.

I’m sitting tight, ignoring the temporary micro-cap swings, and waiting for the second half of the year to fundamentally reset AMPG's market valuation.

My dear $IREN 👊👊👊

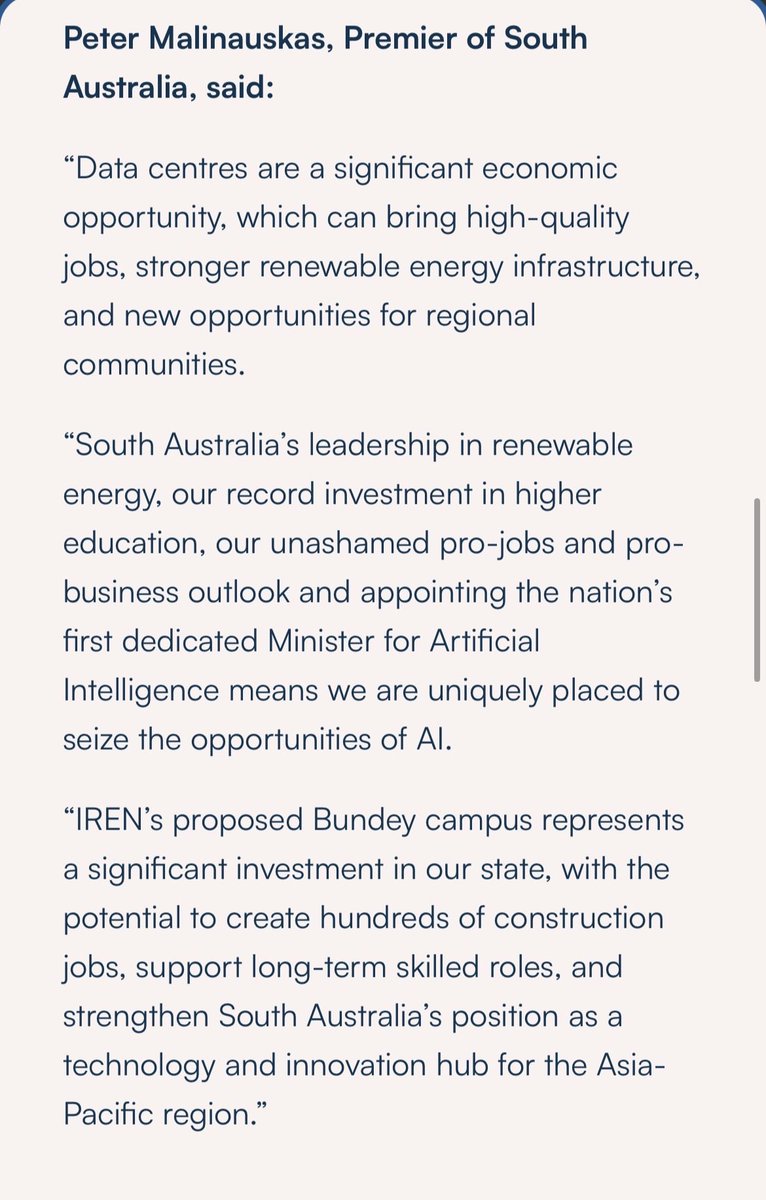

IREN has signed a transmission connection agreement for a planned 800MW data center campus in Bundey, South Australia. The project secures high-voltage capacity directly into the utility's substation, with energization expected to begin in 2028.

It begins, let’s go $IREN !

IREN has announced a planned 800MW data center campus in Bundey, South Australia.

This marks IREN’s first announced Australian data center project and one of the largest in the Asia-Pacific region announced to date.

Learn more: https://t.co/3bOYCUG3pk

@scopeintime Great that you’re still holding and in profit - I sold that a long time ago, and it’s one of my worst decisions. I just don’t like how the management operates.

This is why I post my research here.

Knowing that it actually helps people makes it all worth it.

Did anyone here actually pick up some shares of the companies I covered because of my analysis?

Would love to know! 🚀

@daccache85 Great to hear that. I do have some reservations about XFAB in terms of management and execution. The company does look undervalued relative to the current market, but I’m not sure whether it will actually deliver on its promises.

@mouou74541@TheBigBerbowski Thanks for kind words and your support! That’s my strategy for the next few months - just doing my own thing and focusing on solid, high-quality research.