When you spend more than you earn, that gap doesn't vanish, it lands on a credit card.

FINRA found fewer people are clearing those cards in full than a few years ago. Steady incomes that just don't stretch like they used to.

Looking fine and feeling fine are two different budgets.

More than a quarter of Americans say they spend more than they earn, as rising costs continue to strain household budgets. FINRA finds 26% are outspending their income, while only 44% say it is “not at all difficult” to pay all their bills.

Asking for help with your debt is honestly a bigger flex than trying to budget your way out of a literal crisis.

The New York Fed just dropped the latest stats and spoiler alert... everyone is collectively hitting their limit and deciding to actually do something about it.

The best generational money lessons are not cute spreadsheet hacks. They are literally just knowing when your old plan is a total flop and it is time to pivot.

That is exactly where the real path out of credit card debt begins.

37% of Americans have less than $500 saved. 45% couldn't cover a single month without income.

So when the car breaks or the tooth cracks, the credit card steps in. That's not a budgeting problem.

That's a savings gap. And it's why so many households end up looking for credit card debt relief, not because they overspent, but because life cost more than the buffer could absorb.

Full breakdown on YouTube: https://t.co/3vhwVcjMsl

@robwilsontv walks through all four Maryland debt relief paths and which one fits which starting point.

There are four different debt relief options in Maryland, but only one actually reduces the total amount you owe.

For over 23 years, Freedom Debt Relief has helped over a million members navigate this exact choice with absolutely zero upfront fees.

Watch the video below to learn how to find the strategy that perfectly fits your financial goals today! 🎥👇

Debt relief programs are bound by a federal rule most people have never heard of: a company can't legally collect a fee until a debt is settled, you've approved it, and at least one payment has reached the creditor.

That order matters. It's the cleanest filter for telling a legit program from one to walk away from.

Freedom Debt Relief is built around that exact rule, no payment until you've signed off on a settlement.

The video above walks through how the rule works and how to use it as your own checklist before you enroll anywhere.

Quick one that affects your wallet more than you'd think: a new Yale Budget Lab analysis puts the tariff hit at $760 to $1,500 a year per household, depending on whether current tariffs expire or get extended, and it lands hardest on everyday basics like cars, clothes, and furniture.

If that pressure's showing up on your credit cards, you're not alone. We talk to people in exactly that spot every day. It's not a personal failure, and there's a way through it.

Worth adding here: "trouble paying it down" usually isn't an effort problem.

Minimum payments are built so most of each one goes to interest, the balance barely moves by design.

Once you see that, what it takes to get out of credit card debt looks completely different.

The Fed held interest rates steady today. Here's what that means for you:

The Fed's rate is sitting at 3.5–3.75%.

The average APR on credit cards carrying a balance is around 21.5%, a gap that's stayed historically wide even as the Fed has cut rates.

Translation: your APR isn't waiting on the Fed. The good news? You don't have to either.

Credit card debt settlement is a real, achievable path at today's APR levels.

After 23 years and 4,500+ creditor relationships, we've watched over a million people move from stuck to settled.

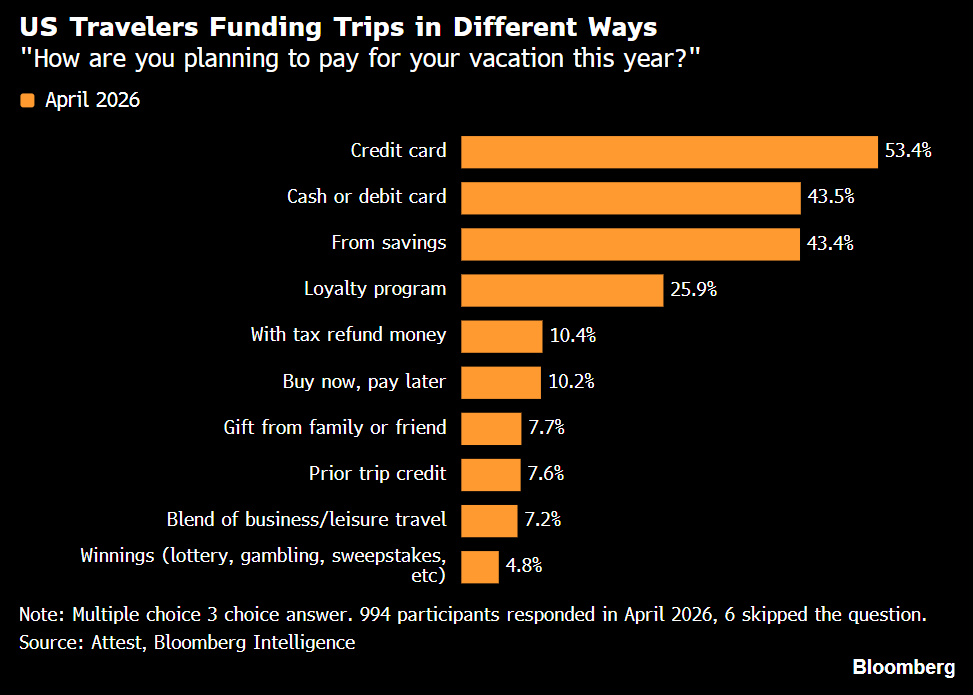

More than half of Americans are using credit cards to pay for vacations this year, which means the conversation about managing those balances afterward should be part of the discussion too.

Credit card interest is doing more work than most people realize. At today's 23.75% APR, paying $250 a month on a $7,000 balance takes 41 months and $3,305 in interest, per @LendingTree .

That's a striking number, most of it going toward interest, not the balance itself. The real conversation isn't about minimum payments.

It's about how today's rates have quietly changed what "paying down debt" actually means.

Stress makes financial decisions harder, which just creates more stress. It’s an exhausting cycle.

Breaking that loop with a customized plan frees up way more than just your cash flow.

Financial stress isn’t just a "feeling." It is a physical weight.

Clinical research shows that debt anxiety actually impacts your sleep, your focus, and your heart.

So when we talk about debt relief, we aren't just talking about money. We're talking about getting your peace of mind back.

Over 60% of the people we serve see their first settlement within 3 months.

And the best part isn't just watching the balance go down, it’s the measurable drop in stress that comes with finally having a plan.

You don't have to carry this alone. https://t.co/I8GyZrEKIc