The SFR and BTR data space just lost another independent option.

It was already thin, a handful of providers, most locked behind enterprise contracts and five-figure commitments. Zonda joining CoStar doesn't make that cheaper. Acquisitions like this never do.

This is the exact frustration we built FrontFoot to fix. Tired of the pricing. Tired of the limited options.

Quality SFR + BTR data, actually accessible: daily-refreshed rents, comps, and ownership. No contract. No card. No sales call.

Underwrite your first deal free: https://t.co/4xgFUKNXxX

The rumor over the past year+ was that homebuilding data giant Zonda was looking for a buyer

Given the ambitions of CoStar—a CRE data giant—them being the buyer isn’t too surprising

On the listings side (https://t.co/Xn1gdEwei8), CoStar has been pushing further into housing

The build-to-rent wave isn’t just a trend. It’s institutions finally accepting what a lot of operators already knew: single-family rentals can be run at scale with better consistency than scattered-site portfolios.

The piece from Construction Physics walks through the data. Why BTR is growing faster than most people expected, where the capital is coming from, and what it means for supply in the 2025–2030 window.

Worth reading if you’re trying to understand where the next wave of professional housing is actually being built.

https://t.co/SxlCCncpjp

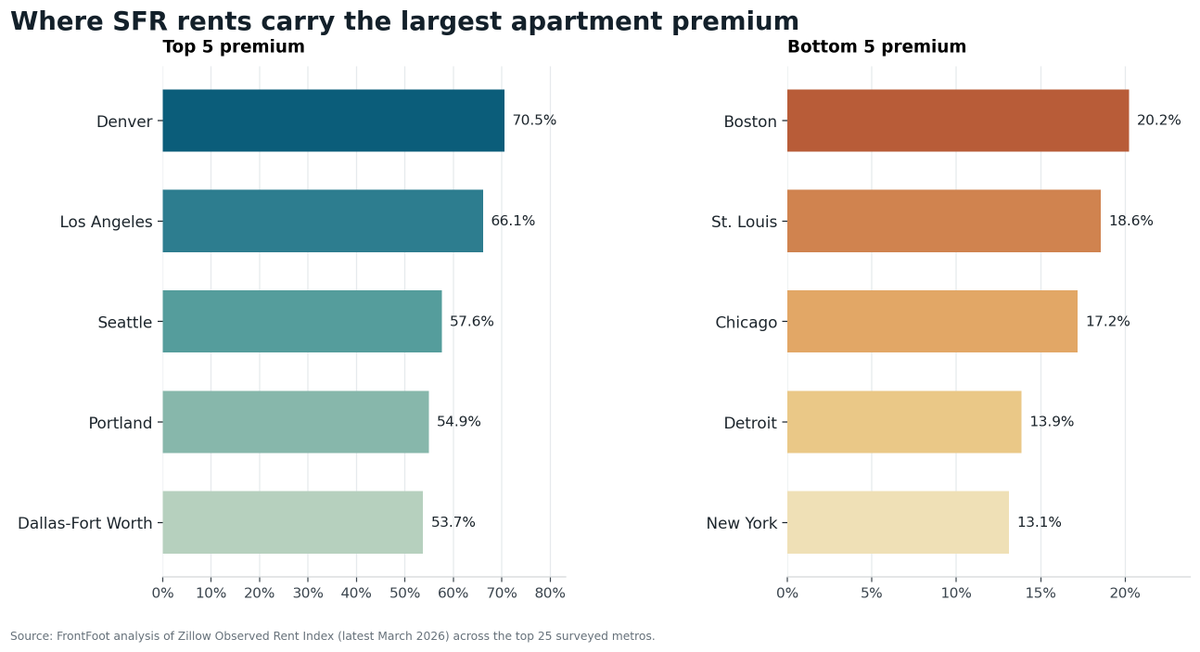

The apartment-to-house rent spread is not one market story. It is a metro-by-metro map of how expensive it is to move from a unit to a yard.

Across the top 25 metros we surveyed, the SFR premium to multifamily rents runs from roughly 13% in New York to roughly 70% in Denver.

That range matters more than the national average.

A wide premium says the detached rental product is scarce or structurally different from the apartment stock. A narrow premium says apartments and houses are competing more directly for the same renter wallet.

Huge win last night.

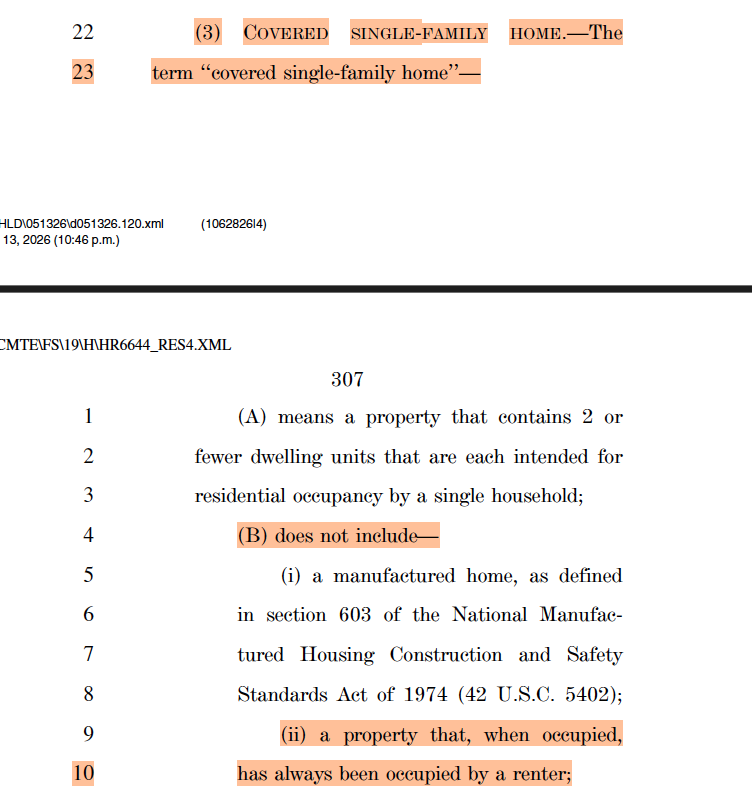

Did you also see the language on Covered Single Family Homes - does NOT include "a property that, when occupied, has always been occupied by a renter;"

Very vague but maybe allows for transfers of rental homes that have been rentals for years or since ownership.

🚨 Late last night, House GOP leadership dropped its amended ROAD to Housing Act.

Big update for BTR:

✅ 7-year forced selloff appears removed

✅ clean BTR exemption added

✅ renovate-to-rent carved out

✅ LIHTC / restricted-rent housing carved out

✅ unified rental communities + 5 contiguous rental units carved out

That is excellent news for the BTR world.

One sleeper clause stood out too:

The definition of “covered single-family home” does not include a property that, when occupied, “has always been occupied by a renter.”

That language will be very interesting to watch.

How the market interprets it could matter a lot for renter-occupied SFR, portfolio trades, and purpose-built rental stock.

@ScottChoppin Saw some townhouse deals get done recently and some that are about to be taken to market.

Do detached start pricing like the failed rent to own platforms (Home Partners of America)?

@KevinDureiko@realEstateTrent This was the area we were looking after leaving Marin County. Only place that has the beauty and access to a gateway city. But yeah just add Fairfield County in there too.

Ended up back in FL due to some other things.

Let’s hope this is accurate. Would be huge for the industry. While a few deals have still been pushing forward, mostly townhome deals. Investors have pulled pack substantially on deals not in progress already.

Woah! Big scoop. If true, I would assume this kills the ROAD to [Less] Housing Act in current form -- giving the House coverage to scuttle the Senate's language that would effectively kill build-to-rent housing construction.

Notably: The White House previously supported ROAD.

The housing market is not short or oversupplied. Specific markets are.

If you’re still using one national take to underwrite local housing decisions, you’re already behind.

The edge now is knowing where inventory is loosening, where leasing is slowing, and where demand is still real.

A home sitting 175 days and re-leasing lower tells you more than a national rent-growth chart.

Housing decisions are getting more local, not less.

The useful question isn’t “what is the market doing?”

It’s “what is this submarket doing right now?”

A 10% incentive load is a footnote that changes the whole market read.

If the sale happens only because the builder bought the rate down, covered closing costs, and sweetened upgrades, that is demand support—not clean strength.

Mechanics matter.

When unsold homes fall because incentives rise and starts slow, that’s not the same signal as organic demand strength.

Builder inventory can clear while the underlying read gets weaker.

Incentives, pace, and margin tradeoffs matter more than the headline.

Consumers using AI company Anthropic’s popular chat tool, Claude, can now hire home service contractors without leaving the platform.

What’s happening: Home services marketplace Thumbtack on Thursday announced a new integration with Claude, enabling users to receive tailored recommendations for local contractors following inquiries about home maintenance, repairs, or upgrades.

Thumbtack counts more than 300,000 service businesses in its network, the company says, including HVAC, plumbing, and electrical contractors across the U.S.

Full story: https://t.co/760lFadsgv

FrontFoot gives lenders, acquisitions and asset management teams on-demand SFR intelligence using the same data institutional operators use. We track 500K+ properties daily so you can analyze markets, find comps, and export underwriting-ready reports in seconds instead of spending hours stitching data together.

Need intros to SFR operators, acquisitions teams, asset managers, and investors who live in this workflow.

This week’s housing signal stack:

• policy risk up

• builder incentives still elevated

• local supply diverging faster than national commentary admits

The job now is not more data.

It’s cleaner separation between signal and story.

Just when rental decreases started to happen. Supply was already tightening. This is going to be bad for the consumer.

Additionally the 7-year sell off is a horrible idea. Rentals will need to be structured more like rent to own. This means rents need to be meaningfully higher.

Home Partners of America rents are significantly higher than other operators.

If you track only price and rates, you’re missing the real decision signals.

Track:

• incentive load

• days to lease / days on market

• permit / starts direction

• local vacancy pressure

• policy risk by market

That’s where the read gets sharper.

Going into next week, the smartest housing operators are watching three things first:

1. where policy risk starts changing capital behavior

2. where incentives stay elevated despite “strong” headlines

3. which local markets keep separating from the national story

![jayparsons's tweet photo. Woah! Big scoop. If true, I would assume this kills the ROAD to [Less] Housing Act in current form -- giving the House coverage to scuttle the Senate's language that would effectively kill build-to-rent housing construction.

Notably: The White House previously supported ROAD. https://t.co/F7UJJEGFjW](https://pbs.twimg.com/media/HHgSuchXUAIwQf3.jpg)