Deep|Glasswing/Mythos: AI-Native Cyber Capability Drives a Reshaping of the Cybersecurity Value Chain and Sector Divergence

On June 2, Anthropic expanded Project Glasswing to nearly 200 partners. We do not view this as a simple expansion of a frontier-model pilot. Rather, we see it as an important signal that AI-native cyber capability is beginning to enter real-world enterprise and critical-infrastructure security workflows.

In industry terms, models such as Claude Mythos Preview are likely to push the marginal cost of vulnerability discovery another step lower, while shifting the center of gravity in cybersecurity from “finding vulnerabilities” toward later-stage, more closed-loop workflows such as validation, prioritization, remediation, response, and governance.

We expect this to drive more pronounced dispersion within the cybersecurity group. Vendors with platform breadth, cross-domain telemetry, enterprise workflows, remediation loops, and security-operations control points should be better positioned to capture the incremental value created by this technology shift. By contrast, companies whose business models still depend on traditional vulnerability scanning, low-end SAST, point AppSec scanners, or commoditized SOAR automation could face the dual pressure of functional commoditization and multiple compression.

At the public company level, we are more constructive on platform vendors capable of supporting an end-to-end security loop, including $PANW , $MSFT , $CRWD , GOOGL, and $CYBR . Conversely, $QLYS , $TENB , $RPD , and parts of the lower-end AppSec / SAST tooling market should be viewed with caution, as their medium-term narratives could come under pressure.

Detailed Report

https://t.co/eYcYEQj3Xk

Most research stops at "what happened." The edge comes from understanding why — which drivers are repeatable, where concentration risk hides, how tone shifts quarter over quarter.

27 new SKILLs are now live on FUNDA reseaech platform — revenue decomposition, margin attribution, supply chain mapping, management credibility trends. Research infrastructure designed to go deeper than surface reporting.

Feedbacks are more than welcome.

Capex/FCF -> Debt/Leverage

Most ROI analysis on AI has focused on Big Tech capex and FCF.

But as more companies approach zero or negative FCF, I think the focus needs to shift toward net debt and leverage.

Given the ROI we are seeing from AI investments, I suspect companies will not pause spending simply because FCF hits zero - which is already happening for some names. The real constraint is more likely to come when companies (first) move into net debt, and (then) when leverage reaches a level that is no longer sustainable.

The complication is that many Big Tech companies now have meaningful off-balance-sheet obligations - finance leases, operating leases, JVs, purchase commitments, and cloud/infrastructure commitments. These may not show up as debt today, but they will likely become a drag on FCF over time.

-------------------

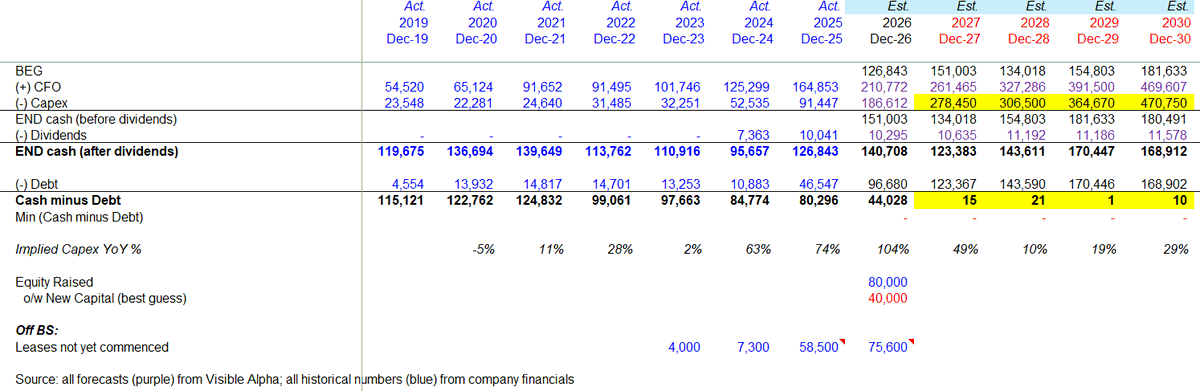

$GOOGL

$GOOGL is relatively clean from an off-balance-sheet perspective, other than approximately $76B of leases not yet commenced.

Management has also said $Googl does not intend to move into a net debt position. Using consensus estimates from Visible Alpha and assuming $Google is willing to run down to roughly zero net cash, the implied maximum capex for FY27 would be approximately $280B, or roughly 50% YoY growth.

$GOOGL also has some buffers:

- ~$40B from the $80B equity raise (a $15B convert, $15B common equity, $10B private placement, and $40B ATM offering) (source: https://t.co/wAEEfPLeoo)

- ~$10B per year of dividends that could theoretically be adjusted.

-------------------

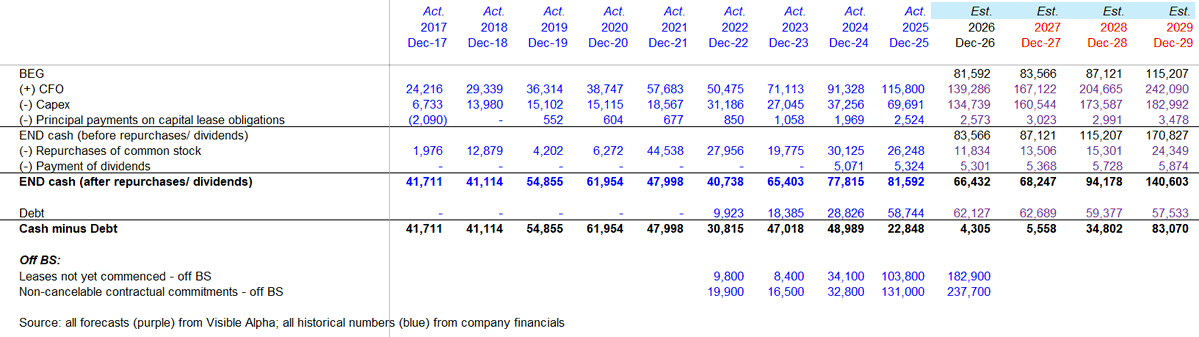

$META

$META has much larger off-balance-sheet commitments.

The two biggest buckets are:

1. Leases not yet commenced - $183B off balance sheet as of 1Q26

2. Non-cancelable contractual commitments - $238B as of 1Q26

Importantly, $42.25B is due in 2026 and $47.65B is due in 2027.

$Meta also disclosed several additional items that are worth tracking separately:

- A contingent obligation to purchase up to $14.72B of cloud capacity over five years

- April 2026 infrastructure contracts that increased non-cancelable commitments by another ~$24B

- Unconsolidated VIE exposure of $46.0B maximum exposure to loss tied to venture economics

It is impossible to know the exact future FCF, cash, and debt impact from these off-balance-sheet items. But directionally, $Meta looks much more likely to move into a net debt position once we account for these obligations - especially given the $42.25B due in 2026 and $47.65B due in 2027.

-------------------

Bottom line

The AI capex debate should not stop at reported capex and FCF. For companies with large off-balance-sheet commitments, the better question is: what does the balance sheet look like once these obligations start flowing through cash? On that basis:

$GOOGL still looks relatively clean and has the most balance-sheet flexibility.

$META has the most meaningful off-balance-sheet risk and is likely to move into a net debt position.

$AMZN has large commitments and seems certain to move into net debt.

Net-net, I actually (weirdly) feel better after going through this exercise.

1/ These companies still have some cash buffers. Even after adjusting for off-balance-sheet commitments, most are not getting to an unsustainable leverage position in the near term.

2/ This analysis is based on consensus cash flow from operations. Actual CFO could come in higher if AI ROI starts showing up more meaningfully.

3/ Companies still have some flexibility - not a ton, but some - if they decide to slow or pause share repurchases and dividends.

So the conclusion is not that Big Tech is immediately constrained. The better question is: how far can they push AI infrastructure spending before the balance sheet, not the income statement, becomes the constraint?

+++

Full analysis: https://t.co/2ZzO8YJ9xy

Deep|Coherent Lite Reshapes AI Optical Interconnects

The industry’s prevailing narrative of Coherent Lite still largely centers on DCI/LR/campus interconnect: the 2–20 km reach segment, where a lower-cost, lower-power coherent solution replaces the conventional IMDD, which is increasingly strained in mid-reach transmission beyond 400G/lane. This narrative is not wrong, but it captures only Coherent Lite’s “reach dimension” and misses the “system-architecture dimension,” where the real volume will come from. From an AI infrastructure standpoint, Coherent Lite’s most important use case — and the one most likely to scale — is not 2–20 km DCI or LR, but rather pairing with OCS in Google TPU / AI clusters.

OCS improves network-topology reconfigurability and expands the Scale-Up and Scale-Out interconnect scale; however, the cost is that each OCS node the optical link passes through adds insertion loss. OCS is fundamentally a passive device, introducing roughly 1.5–3 dB of additional loss. For conventional IMDD FR/DR links, the link budget is typically only a few dB; after subtracting OCS’s ~3 dB of loss and additional fiber/ connector losses, IMDD has almost no remaining link margin in the 2.4T/3.2T generations. In other words, the more OCS becomes the core component of AI cluster network expansion, the more exposed IMDD’s link budget bottleneck becomes.

Coherent Lite’s strategic significance is therefore not merely “pushing coherent down to 2–20 km,” but providing the next-generation optical transport solution for OCS-paired interconnect. Through a simplified coherent detection scheme, Coherent Lite can recover the link budget margin consumed by OCS, allowing the OCS architecture to continue scaling into the 2.4T/3.2T module era. In short, DCI/LR is the surface-level application the industry understands best, while OCS-paired links are Coherent Lite’s most central and scale-driven deployment scenario in AI infrastructure.

On the value-chain mapping: Nokia/Infinera, Lumentum, Coherent Corp, and Sumitomo Electric are the core InP beneficiaries; Marvell is the core DSP beneficiary; Semtech is the TIA beneficiary; TeraHop/InnoLight, Lumentum, and Coherent Corp are the core transceiver beneficiaries; while TSEM, Soitec, and AXT correspond respectively to the underlying area-amplification logic of SiPh foundry, Photonics-SOI substrate, and InP substrate. In 2028, Coherent Lite may bring $15–20 billion of incremental industry value, and this figure will rise further in 2029.

$LITE $COHR $AXTI $NOK $MRVL

Detailed Report

https://t.co/rwc043pfEg

The semiconductor memory cycle has a timing problem. Sell-side consensus models for the DRAM supply-demand inflection largely ignore yield ramp realities, HBM wafer diversion, and the structural lag between capacity announcements and actual bit output. The gap between when the street expects the turn and when it actually arrives is where the trade lives.

That timing gap is precisely what this Play quantifies. It models five supply-demand variables across SK Hynix, Samsung, and Micron — producing a probability distribution for when DRAM transitions from shortage to oversupply, not a single date.

Here's what the Play covers:

Inflection Probability Timeline

The model produces a quarter-by-quarter cumulative probability curve for when supply-demand balance tips. Rather than anchoring on one date, it shows the full distribution — helping investors identify where consensus positioning diverges from modeled likelihood.

Supplier Capacity Tracker

Each of the three major DRAM producers carries different expansion timelines, yield curves, and long-term agreement lock ratios. SK Hynix leads on yield and speed; Samsung carries the largest absolute capacity delta but with slower ramp; Micron's Idaho fab represents a significant future supply addition. The Play tracks each supplier's effective supply contribution quarter by quarter.

Scenario Analysis

Four distinct scenarios — ranging from aggressive capacity ramp to prolonged supply tightness — allow investors to stress-test positioning under materially different industry conditions. Each scenario adjusts multiple variables simultaneously to capture how correlated shifts in demand and supply interact.

Sensitivity Tornado

Ten independent variables are ranked by their impact on inflection timing. Initial days-of-inventory dominates the total swing. HBM bit demand growth and wafer diversion ratio follow. The tornado chart makes clear which assumptions to monitor — and which are noise.

DRAM Memory Inflection is now live on FUNDA for all subscribers.

These past few days, I've been playing with our new Play every day. I keep scanning the strength and stage changes of different Narratives, and analyzing whether each one is in the ignition phase, spreading phase, crowded phase, or some other stage... Clearly seeing how each Narrative develops, and scanning all Narratives across the whole market.

Markets don't move on data alone — they move on stories. The question is not just whether a narrative is right, but where it is in its lifecycle: just beginning to spread, already fully priced in, or somewhere in between. Most investors sense this intuitively, but lack a systematic way to track it.

That timing is the core problem. A compelling thesis can generate alpha at the right stage and destroy it at the wrong one. The same trade that delivers triple-digit returns during its diffusion phase can become a crowded exit trap once consensus forms. Today we're launching Narrative Tracker on our full-stack research platform to tell the difference.

Here's what the Play covers:

Alpha Opportunities

The Play identifies narratives that have reached institutional confirmation and are still generating excess returns relative to broader markets. Each opportunity is ranked by realized alpha since confirmation, with lifecycle staging that indicates how much room remains before the trade becomes consensus.

Emerging Narratives

Before a narrative reaches confirmation, the Play tracks it in its earliest stages — initial institutional attention and cross-channel diffusion. Each emerging narrative carries a probability score reflecting confidence that alpha will materialize, giving investors a watchlist of themes before they become crowded.

Exit Watch

Not every confirmed narrative stays productive. The Play monitors exit urgency across multiple risk dimensions — retail frenzy, trade crowding, price absorption, heat decay, and counter-narrative strength. When conditions deteriorate, the system flags exit priority levels so investors can reduce exposure before the reversal.

News-to-Narrative Mapping

Fresh catalysts are mapped to their parent narratives in real time, with signal strength ratings. Rather than scanning headlines individually, investors see which news events reinforce or challenge existing theses — and which tickers are directly impacted.

Narrative Tracker is now live on FUNDA for institutional clients. For a limited time, all paid Substack subscribers can access the full set through June 5, 2026. Feedback is more than welcome.

Weekly|Welcome Fabian Onboard, $SNOW Cortex Code Inflection, $MRVL Optical Raise, $SMTC Beat, $MDB , $PANW , Next LLM Upgrades

At FundaAI, our biggest event this past week was having Fabian onboard. Fabian is one of the respected voices covering data center interconnect, test and measurement, and AI infrastructure names on Substack and X today, with a decade of hands-on industry experience that very few writers in this space can match.

His work on the optical testing industry earlier this year was the first time we came across his work, and since then, we have been exchanging views on transceiver roadmaps and the broader photonics value chain. The technical depth he brings from inside the industry, combined with a strong instinct for how it flows through to public market names, made the decision to work together feel natural and easy.

Fabian will be covering data center interconnect, test and measurement vendors, and networking hardware, among others, at FundaAI, while continuing to run his own Substack. If you haven’t subscribed to him, you can do so here. You can also find him on X Fabian (@iamfabian) / X.

This week of earnings belonged to data and SaaS. The standout was Snowflake — the Cortex Code ramp we had been flagging for three straight quarters finally showed up in the numbers. We had dedicated almost our entire preview to it, built into our model that Cortex Code alone could add roughly 2% of incremental revenue, and called it the fastest-ramping product in Snowflake’s history; management then spent nearly the whole call on it. On the other hand, in our MDB preview, we highlighted that investors may be too optimistic about the consumption tailwind from Anthropic, as well as about Enterprise Advanced becoming increasingly important, which the market might not appreciate. Both were validated in the earnings and caused significant volatility post-earnings.

On the hardware side, Marvell printed an inline quarter, with the raises landing about where we expected — interconnect at +70% and data center at +50%. We are still ahead of management on growth and view the FY28 data center guide as conservative; optical pays the bills today, and Marvell’s Google content compounds faster than the lazy TPU-unit math implies. We also captured the upside from SMTC in our Institutional publication, which was the clear standout performer in the recent optics pullback. As a reminder, if you are interested in our full research coverage, please reach out to [email protected] for more information.

This Week’s Reports

SNOW 1Q26 — the Cortex Code call lands. Product revenue grew 34% YoY, the largest beat in recent memory, and the full-year guide was lifted from 27% to 31%; the print validated the Cortex Code thesis we had been building for three quarters. We continue to see Snowflake, alongside Datadog, as one of our two favorite AI SaaS names.

https://t.co/UfHg4VwANu

https://t.co/FebDE5cqkV

MRVL FY1Q27 — in-line print, but the optical raise is the story. We went in expecting a modest beat with the guide as the real swing factor; management raised interconnect to +70% and data center to +50%, yet our growth assumptions remain ahead and we think the FY28 data center outlook is too conservative. Optical demand is real and supply-constrained — the laser bottleneck, not demand, is the limiter.

https://t.co/dKMgOWf0BZ

https://t.co/gW40cNqMIX

Premium Report Snapshot

...

Detailed Report

https://t.co/pxPiBv4Ipn

Fabian has deep experience in interconnect and testing and we’re looking forward to bringing that to bear on everything going in Taipei the next couple of days. The team is growing and we’re still hiring!

Markets don't move on data alone — they move on stories. The question is not just whether a narrative is right, but where it is in its lifecycle: just beginning to spread, already fully priced in, or somewhere in between. Most investors sense this intuitively, but lack a systematic way to track it.

That timing is the core problem. A compelling thesis can generate alpha at the right stage and destroy it at the wrong one. The same trade that delivers triple-digit returns during its diffusion phase can become a crowded exit trap once consensus forms. Today we're launching Narrative Tracker on our full-stack research platform to tell the difference.

Here's what the Play covers:

Alpha Opportunities

The Play identifies narratives that have reached institutional confirmation and are still generating excess returns relative to broader markets. Each opportunity is ranked by realized alpha since confirmation, with lifecycle staging that indicates how much room remains before the trade becomes consensus.

Emerging Narratives

Before a narrative reaches confirmation, the Play tracks it in its earliest stages — initial institutional attention and cross-channel diffusion. Each emerging narrative carries a probability score reflecting confidence that alpha will materialize, giving investors a watchlist of themes before they become crowded.

Exit Watch

Not every confirmed narrative stays productive. The Play monitors exit urgency across multiple risk dimensions — retail frenzy, trade crowding, price absorption, heat decay, and counter-narrative strength. When conditions deteriorate, the system flags exit priority levels so investors can reduce exposure before the reversal.

News-to-Narrative Mapping

Fresh catalysts are mapped to their parent narratives in real time, with signal strength ratings. Rather than scanning headlines individually, investors see which news events reinforce or challenge existing theses — and which tickers are directly impacted.

Narrative Tracker is now live on FUNDA for institutional clients. For a limited time, all paid Substack subscribers can access the full set through June 5, 2026. Feedback is more than welcome.

We are thrilled to welcome @iamfabian Fabian to FundaAI. Fabian is one of the respected voices covering data center interconnect, test and measurement, and AI infrastructure names on Substack and X today, with a decade of hands-on industry experience that very few writers in this space can match.

His work on optical testing industry earlier this year was the first time we came across his work, and since then we have been exchanging views on transceiver roadmaps and the broader photonics value chain. The technical depth he brings from inside the industry, combined with a strong instinct for how it flows through to public market names, made the decision to work together feel natural and easy.

Fabian will be covering data center interconnect, test and measurement vendors, and networking hardware among others at FundaAI, while continuing to run his own Substack.

Keeping a little mystery here, his first report since joining digs into a new area, and we are both very excited about it. Looking forward to the next leg of this journey together!

Happy to share that I am joining @FundaAI.

For more than a year, the team has been publishing rigorous, differentiated research on photonics, memory, software, and the rest of the AI infrastructure stack. I have spoken to them several times over the past few months and have been impressed by the depth of their expertise, their culture, and their determination to build a respected and trusted research firm. On top of that, they are building an ambitious AI powered research OS that I think will change how the buy side consumes fundamental work.

I will continue running my own newsletter on Substack alongside the FundaAI role, and the two should complement each other well.

A note on prior content: any posts, tweets, or newsletter pieces published before my start date at FundaAI reflect my personal views at the time of writing and were produced entirely independently of FundaAI. They do not represent the views of FundaAI, were not reviewed or endorsed by FundaAI, and should not be interpreted as the firm's research, recommendations, or investment advice. Any positive or negative commentary on specific companies, securities, or individuals in that prior content predates my affiliation with FundaAI.

Going forward, all tweets and posts on my newsletter represent my personal views only and do not constitute investment advice or the views of FundaAI. There will be some restrictions on what I can comment on. FundaAI takes its regulatory obligations seriously and expects the same from its team.

It has been an incredible six months on Substack, life changing to say the least, and I am looking forward to the next leg of this journey.

Review| $SNOW 1Q26: Cortex Code Driving Acceleration, Reconfirmed

This was a Snowflake quarter that genuinely excited me. We’re also thrilled that in our Preview we boldly articulated the Snowflake upside we’d seen in our research, and built into our model that Cortex Code alone could contribute 2% of incremental revenue to Snowflake.

Following Datadog’s earnings, everyone has been asking which company most resembles Datadog in terms of earnings performance. The conclusion we provided in our Preview is Snowflake.

Looking back at our views on Snowflake over the past several quarters:

We first turned constructive on Snowflake’s inflection in 3Q24, arguing that Iceberg was incremental rather than a headwind, and boldly predicted that Snowflake would slow hiring and focus on OPM.

https://t.co/d3k4TU3qKC

In our 3Q25 Preview, we believed Snowflake would face headwinds from Gen2 optimization and Snowpark Connect. At the same time, frontier labs were also optimizing on Snowflake, putting Snowflake’s revenue at risk.

https://t.co/Z3Wf7Pnps9

In our 4Q25 Preview, we argued that Gen2 optimization was complete, Snowpark Connect had flipped from a negative to a positive, and frontier labs had finished optimization and were beginning to ramp consumption.

https://t.co/FebDE5cqkV

In our 1Q26 Preview, we interviewed 6 experts to understand Cortex Code’s progress. We boldly called Cortex Code the fastest-growing product in Snowflake’s history—far faster than Snowpark. We highlighted that Cortex Code is not just the data version of a coding agent, but also directly absorbs non-data workloads, which is why Cortex Code’s growth is far outpacing products like Text-to-SQL. We also argued that Cortex Code’s gross margin could come in higher than the market expects, because Cortex Code is priced 40% higher than Claude Code.

Our calls over the past three quarters have been validated one by one across three quarters of Snowflake’s results. This quarter, Snowflake devoted nearly the entire earnings call to discussing Cortex Code.

Detailed Report

https://t.co/UfHg4VwANu

Every day there will be 100 people going long and 100 people going short. So understanding one's track record and the reasoning behind the analysis becomes very important. FundaAI has always been working to improve accuracy by doing a lot of research. And FundaAI's track record on $SNOW is:

We are very bullish in 1Q26, and we think Cortex Code is taking in the spillover demand from Claude Code. Because Cortex Code hosts the Anthropic model by itself, it is faster than Claude Code. This is the fastest-growing new product in Snowflake's history.

We were bullish in 4Q25, because the Gen2 optimization was close to finishing, and Snowpark Connect also turned from a negative impact to a positive one.

We were bearish in 3Q25, because we saw that Gen2 optimization and Snowpark Connect were both having a negative impact on Snowflake at the same time, and Frontier Labs were optimizing their Snowflake budget

...

We have been bullish on Snowflake since 3Q24, and we believed that the new CEO was making the right and aggressive organizational changes to Snowflake.

@girish_i_am This is an institutional report. I also believe we've delivered a great deal of alpha to Substack over the past two weeks, with names like $QCOM and $SNOW .

Since we published our $SMTC report on the institutional side on May 7th, SMTC has risen 40%. Over the past month, we have highlighted SMTC as one of the stocks set to benefit most at this stage from the TPU and Optics industry trends, and we successfully called the earnings ahead of the results.

Review| $MRVL FY1Q27: Long term outlook remains strong; FY28 DC guidance appears conservative

Marvell delivered relatively in-line earnings, supported by the strength of its AI interconnect business. While FY27 and FY28 outlooks were raised, our growth assumptions remain ahead of management’s guidance. In particular, we see upside in the interconnect business in FY27 and in the XPU attach business in FY28.

Detailed Report

https://t.co/dKMgOWesMr

Preview| $MRVL 1QFY27: Positioned For A Raise

Marvell reports F1Q27 results after market close on 27 May 2026.

Having doubled since the last print, Marvell has a tougher set-up for the upcoming print. Given the strong commentary from optical peers, we believe Marvell will meet the buyside expectations of a modest beat vs guide of $2.4b.

Marvell previously guided FY27 data center revenue to grow 40% YoY and the interconnect business to grow 50% YoY. As we model these numbers at approximately 60% and 90%, we expect management to also raise their guidance. Our growth assumptions support our FY27 and FY28 EPS of $4.36 and $7.70.

Detailed Report

https://t.co/GSvgW3UWhT

Preview| $MRVL 1QFY27: Positioned For A Raise

Marvell reports F1Q27 results after market close on 27 May 2026.

Having doubled since the last print, Marvell has a tougher set-up for the upcoming print. Given the strong commentary from optical peers, we believe Marvell will meet the buyside expectations of a modest beat vs guide of $2.4b.

Marvell previously guided FY27 data center revenue to grow 40% YoY and the interconnect business to grow 50% YoY. As we model these numbers at approximately 60% and 90%, we expect management to also raise their guidance. Our growth assumptions support our FY27 and FY28 EPS of $4.36 and $7.70.

Detailed Report

https://t.co/GSvgW3UWhT