Rallis: Seeds + Crop Protection, Tightly Integrated

Rallis operates in both seeds (via Metahelix) and crop protection, with plants at Dahej, Ankleshwar, and Lote. It runs Rallis Kisan Kutumb, a field-validation network—a capability shared with UPL and Coromandel.

India is tightening registrations and formalizing drone-spray labels. These shifts require robust data packages and protocols. Firms with strong R&D and field validation respond faster.

FPOs and platform buyers seek integrated offers: seed, practices, and care bundled. Rallis designs crop-specific solutions from genetics to validation to distribution. This integration at scale remains uncommon in India.

Track where integration becomes competitive advantage → https://t.co/esOSqEw42j

@1shankarsharma

DISA India: Installed Base + Digital = Durable Aftermarket Revenue

DISA India (part of Norican Group) sells foundry machinery with a substantial installed base across India. Its Monitizer platform retrofits onto machines to capture process data and optimize quality control. Norican case studies show 15–40% scrap reduction, unlocking recurring revenue through software subscriptions, spare parts, and OEM-specific upgrades that lock in customer dependence.

Aftermarket solutions buffer capex cycles when new equipment spending pauses, while aligning with regulatory pressure for emissions traceability and lower resource consumption. Parts specificity ensures customers remain reliant on DISA's ecosystem for critical wear items and control upgrades.

Scaling this model across the installed base could meaningfully upgrade revenue quality, increase earnings resilience, and deepen customer stickiness over time.

Track foundry sector insights with GQ FinXray → https://t.co/1MLMsn9uSe

@1shankarsharma

Non-GMO at Scale: How Gujarat Ambuja Exports Plays China+1 Demand

Gujarat Ambuja Exports Limited is among India's largest corn wet millers, supplying maize starches, glucose, and derivatives. India's ban on commercial GM corn makes these products inherently non-GMO — a traceable, identity-preserved input commanding price premiums in select markets. The company holds Food Safety System Certification 22000 and International Organization for Standardization certifications, serving kosher, halal, and Indian, British, and United States Pharmacopoeia-compliant buyers.

As buyers pursue China+1 diversification, GAEL's multi-plant footprint adds sourcing redundancy. Non-GMO labeling rules vary by market, and any pricing uplift depends on certification standing and end-market demand.

GAEL is expanding value-added starch derivatives. Its non-GMO origin and multi-state footprint offer positioning advantages.

Track where compliance becomes competitive advantage → https://t.co/XYmfqbvsSa

@1shankarsharma

Ever thought of per Capita GDP as a nation "s EPS?! Well, read this piece by Shankar Sharma & Amit Bhartia, and your perspective on population decline will change forever!

Do let us know what you think!

https://t.co/dPJMalIzHB

@1shankarsharma

India's wind build is shifting to 3–3.6 MW turbines at 140–160m hub heights, requiring 600–1,000-ton cranes with 12–18 month global delivery lags. Supply is structurally scarce, and Sanghvi Movers holds a meaningful share of this high-capacity fleet.

Day-rates have risen as lifts get heavier. Developers facing liquidated damages show willingness to pay premiums — pricing power that accrues to whoever controls the iron.

Fleet bought at older INR costs now earns rentals priced against euro/dollar replacement values — a quiet margin tailwind. A largely paid-down fleet converts this upcycle into structural rental economics.

Track where scarcity meets operating leverage → https://t.co/57LokoCtiN

@1shankarsharma

We knew Legal Insighter Trading was going to be as good, if not better than Illegal Insider Trading!!

And here's the proof!!

Find out for yourself -> https://t.co/m0wG3y0qVm

@1shankarsharma

R Systems' Hidden 5G Core Edge in Eastern Europe

In 2011, R Systems acquired Computaris—a telecom engineering firm with delivery hubs in Romania, Poland, and Moldova. The unit does protocol-level work: real-time charging, policy control, and BSS software for mobile networks.

As 5G standalone rollouts expand, operators need scarce protocol-heavy engineering for network slicing and advanced charging. Many European telcos prefer EU-nearshore teams for data compliance and collaboration—exactly where Computaris sits.

This embedded, spec-level work tends toward longer engagements and higher switching costs. A niche positioning worth tracking as 5G core spend scales.

Track telecom shifts with GQ FinXray → https://t.co/9chzogWwKn

@1shankarsharma

My piece in @livemint today.

India faces 2 choices: Indian households blow up their savings, giving F2s minimal cost exits.

RBI blows up reserves, defending the Rupee, swapping SIP Rs into USD, giving F2s low cost exits.

Our projected import ( merch+ services) cover is just 6 months. Deep red zone.

Our projected BOP deficit is ~13% ( that's optimistic IMO) of current reserves. Even in 2008, it was just 8%.

So get the magnitude of the problem.

We can't fight this 2 front war. It's a ticket to the IMF.

Sensible choice: sacrifice the Stock Market. It never busts a nation.

FX crises always do.

Remember the 80s multiple Latam Tequila crises?

My reco:

RAISE taxation on MF investing.

Lower F2 new investment taxes.

( We used to have 0 tax on F2s and 20% on locals, in the 90s. We needed dollars then. We need dollars now. )

So:

Stock market crashes.

That's fine. F2s try selling but there are few willing buyers on the other side.

Selling into illiquidity always crashes prices.

But we don't lose USDs because quantum of selling absorbed will a fraction of today.

And at 30-40% lower prices, after a crash, the same selling F2s will become buyers.

I have seen this multiple times in my sell side life. " Market is cheap now": becomes the chatter in Manhattan after some champagne. " Let's go back in"

We saw $20 billion flow in 09-10.$ 10 billion in 13-14.

Each after a massive crash.

Crashes almost always trigger massive F2 inflows.

We must make this happen.

We simply can't give easy exits.

Exits must be made costly.

Even unviable.

That's the way it used to happen before.

I am prepared to endure the pain on my India holdings for a while.

Stock markets always come back in a year or two.

No currency ever regains the glory of its pre-crisis levels. Almost none.

Absorb this fact slowly.

Since March this year, I have put ~ Rs.200 cr into India.

I am fine to take pain on my holdings if it saves the country.

Are you, the Jain, the Gupta, the Patel, and millions others, prepared to do the same?

MF distributors? Asset Managers?

Are you prepared to let go your swarth for the country?

Because else, 12 months from now, we will be teetering at abyss' edge.

Steel Strips Wheels: Turning a Basic Product Into an Export Edge

Europe's anti-dumping duties on Chinese steel wheels raise landed costs, prompting OEMs to diversify sourcing. SSWL holds the required OEM approvals to compete for these orders. Management positions the company as globally cost-competitive, though this claim is not independently verified.

The entry point is steel winter wheels. Once on-platform, SSWL can present its cast-aluminium range too — a one-stop portfolio broader than most Indian peers. Rising alloy penetration and larger rim sizes lift value per vehicle over time.

With European approvals, a full steel-and-alloy range, and supportive trade measures, SSWL has credible export positioning today. Track policy-driven commodity shifts with GQ FinXray → https://t.co/sbEdnie4W2

@1shankarsharma

Shankara Turns Commodity Steel Into a Service

India's renovation and light-industrial segment is shifting from raw material to ready-to-use packages. Shankara's BuildPro outlets offer cut-to-length, slitting, shearing, and bundled roofing accessories—delivered doorstep with custom sizes. Small contractors order solutions, not raw tonnage.

Pricing reflects both steel input costs and value-added service charges. Final prices still track spot steel, but processing and logistics layers create barriers most small dealers can't match.

The company is pushing a higher value-added retail mix, which can support ROCE—though it doesn't report service revenue separately. A retail-plus-processing engine built for India's shift to compliant, ready-to-install steel.

Track commodity-to-service plays on GQ FinXray → https://t.co/uOOu6CH7bl

@1shankarsharma

Mold-Tek Packaging: Hidden Edge in In-House Robots, Labels & Molds

Mold-Tek designs its own IML robots, prints labels, and builds molds internally. In-mold labeling fuses label and container during injection molding. Its in-house robots cost ~⅓ of imports, and plants near or inside customer sites enable rapid SKU launches and just-in-time supply.

This matters as brands chase recyclable packaging. Using the same plastic for both container and label creates a single-material pack—easier to recycle. Mold-Tek is among the few Indian players building robots and printing labels in-house; most peers buy both from vendors.

Disciplined vertical integration aligned with brand needs for speed and recyclability—a playbook peers won't replicate quickly. Track packaging plays on GQ FinXray → https://t.co/SVVwnaQDTQ

@1shankarsharma

Keltech's Hidden Perlite Play in India's Cryogenic Boom

Keltech Energies' perlite unit supplies cryogenic-grade expanded perlite for LNG terminals and industrial gas storage — a niche with approved vendor lists, strict QA/QC, and high entry barriers.

India is adding LNG capacity and industrial-gas infrastructure. Each project needs a once-off perlite fill plus periodic top-ups — demand that has earned higher margins than Keltech's explosives segment.

Often labeled an explosives company, Keltech's perlite division is underweighted. Watch India's LNG project pipeline — each award is a concrete perlite revenue opportunity. Track → https://t.co/dHWx09OOGI

@1shankarsharma

Nothing beats genuine trader feedback 😊

Thank you @amoljain9604 for the kind words.

As Shankar Sir said —

“It is getting better!” 📈

See what traders are loving about GQ FinXray → https://t.co/PhTZoCfZQk

@1shankarsharma

TAAL Sits on a Rare Asset: A Private Airfield With MRO Infrastructure

TAAL (Taneja Aerospace) owns the Hosur aerodrome near Bengaluru—a DGCA-licensed, 7,000-ft runway. It hosts Air Works’ base-maintenance facility for heavy aircraft MRO (maintenance, repair & overhaul), now under Adani Defence. Private airfields with this capability outside commercial airports are scarce in India.

India's commercial fleet could roughly double this decade, and policy now favors domestic MRO. Hosur can service base checks and lease redeliveries without competing for airline slots at busy airports.

The aerodrome also supports aerostructures manufacturing, with potential relevance to drones, eVTOL, and defence programs. Replicating this setup near a top aerospace cluster faces land and regulatory barriers

Track aerospace infra with GQ FinXray → https://t.co/UDgk1IaaRV

@1shankarsharma

Why Nitta Gelatin India Limited (NGIL)'s Ossein Step Matters in a Gelatin Supply Chain

Most gelatin makers import ossein. Nitta Gelatin India makes it in-house from bovine bone in India, where raw material availability is among the highest globally. Part is exported to its Japanese parent; the rest feeds its own pharma-grade gelatin plant.

Halal and Kosher certifications on bovine-only inputs let Nitta Gelatin India Limited (NGIL) access regulated pharma and food segments that reject porcine alternatives—a structural filter that narrows competition.

India kept gelatin capsules as the industry standard, shelving proposals for mandatory cellulose substitutes. For the world's generic-drug hub, that decision extends long-duration demand. Track listed companies with GQ FinXray → https://t.co/Zn6AG1jjWb

@1shankarsharma

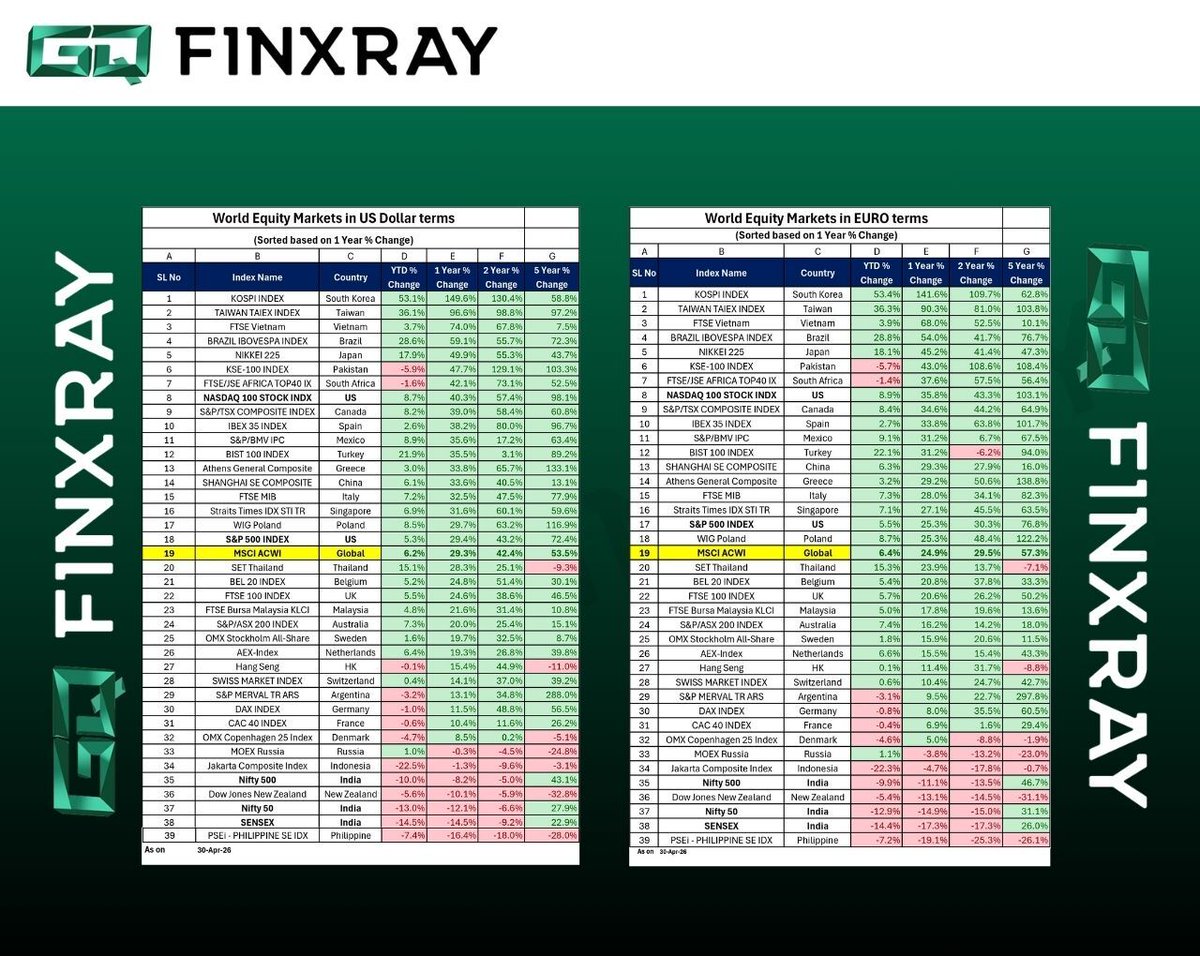

Another illuminating update from our Monthly Global Markets Scoreboard.

Don't look at India please 🥺!

Stop investing in the dark -> https://t.co/3AVY5FXu1q

@1shankarsharma

Shankar Sharma has survived five market collapses by being ruthlessly fearful and data-obsessed. He doesn't want you to be "optimistic"—he wants you to stay alive.

Witness the autopsy of the Bull Market here: https://t.co/5rDWCpSCQC

GQ FinXray is the only antidote. Stop betting on hope. See the data-matrix the "experts" are hiding from you.

Get the antidote for free: https://t.co/xxVc5aNfWS

@1shankarsharma

JKumar: The ₹3,900 Cr Company Building India’s Metros Underground

Underground metro construction has one of the highest technical barriers in Indian infrastructure—tunnelling, diaphragm walls, and IEC compliance mean only ~5 EPC firms in India qualify. JKumar is among them, and one of even fewer executing both elevated and underground metro projects.

In recent months, the company secured ₹2,360 Cr (Vadhavan Port expressway) + ₹1,184 Cr (Lucknow exhibition centre) + ₹616 Cr (NBCC Delhi redevelopment)—taking recent order inflows to over ₹4,100 Cr.

With ~70% revenue from Maharashtra and metro contributing ~40% of the mix, the recent highway and NCR wins signal a deliberate geographic and segment diversification—reducing single-state concentration risk.

Track the next move → https://t.co/lFndzSk5Jr

@1shankarsharma