Without supplying a Verification Report, GST Registration can't be cancelled. Punjab and Haryana High Court

Where GST registration cancellation was proposed alleging non-existence, fake ITC and paper operations based on verification and portal scrutiny without supplying verification reports or material particulars to the firm, such omission denied a real opportunity to respond, violated natural justice, and rendered the show cause notice invalid, hence cancellation proceedings could not be sustained.

North Steel India vs Union of India

CWP No. 8881 of 2026 (O & M) | 30-Apr-2026 | (2026) 42 CENTAX 215 (P&H)

Haryana Government Extends Time Limit for Filing Appeals before the GST Appellate Tribunal under Section 112(1) of the HGST Act, 2017

Read More at: https://t.co/vlhvJZmnuG

Govt soon disable manual editing in GSTR 3B once returns are auto populated from GSTR 1 and GSTR 2B.

The move aims to reduce GST mismatches, tighten checks on defaulting suppliers, and improve automated compliance.

Experts say it can reduce litigation, but genuine taxpayers may face reconciliation challenges due to supplier errors.

TAX AMOUNT AS PER NEW (DEFAULT) TAX REGIME FOR F.Y.2025-26 FOR RESIDENT INDIVIDUAL

(FOR NORMAL TAXABLE INCOME UP TO RS.1 CRORE)

#TaxationUpdates

Website https://t.co/Vlx3AlG5MF

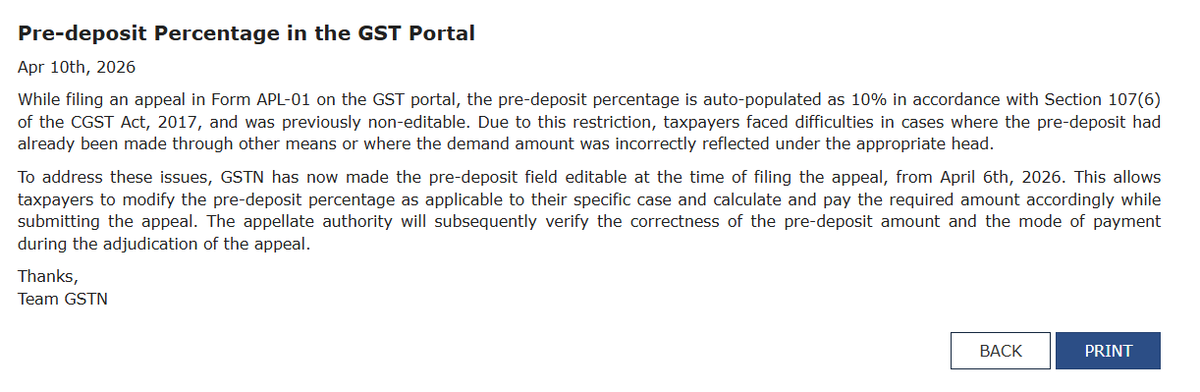

🚨GST UPDATE – Appeal Filing Relief!

Pre-deposit in Form APL-01 is now editable on GST portal (w.e.f. 6 April 2026).

Earlier:

➡️Auto-set at 10% u/s 107(6)

➡️Not editable ❌

Now:

➡️Taxpayers can modify % as per actual case ✅

➡️Helps where payment already made or demand mismatch

Final verification will be done by Appellate Authority.

🚨 GSTN IMS Enhancement!!

A new separate tab has now been provided in Outward IMS to display Rejected Credit Notes etc. - where liability is required to be added back in GSTR-3B

👉 Earlier, we had to manually check all IMS entries to identify such cases.

@Infosys_GSTN 👍👍

A new chapter in tax adjudication. First Paperless Judgement under GSTAT.

𝗢𝗻𝗹𝗶𝗻𝗲 𝗵𝗲𝗮𝗿𝗶𝗻𝗴 𝗼𝗻 𝟭𝟭.𝟬𝟮.𝟮𝟬𝟮𝟲. 𝗝𝘂𝗱𝗴𝗺𝗲𝗻𝘁 𝘂𝗽𝗹𝗼𝗮𝗱𝗲𝗱 𝗼𝗻 𝟭𝟮.𝟬𝟮.𝟮𝟬𝟮𝟲.

Speed, transparency, and technology in action.

#GSTAT#PaperlessCourts#JudicialReforms #eGovernance #GSTLaw #Tribunal #DigitalTransformation #TechInLaw

#FutureOfCourts #NIC #GSTN #DigitalIndia

🔥📛 HC: Grants bail to Accountant on ground of no criminal-antecedents and prolonged incarceration

➡️ Regular bail granted by the Madhya Pradesh High Court (Jabalpur Bench) to an assessee providing GST return-filing and accounting services, who was arrested by DGGI under Sections 132(1)(a)–(d) read with Section 69 of the CGST Act.

➡️ The Court emphasized that the assessee had been in custody since 14 October 2025, the investigation was complete, and charge-sheet filed, with no prior criminal history, making continued detention unnecessary.

➡️ It noted that Section 132(1) of the CGST Act prescribes a maximum imprisonment of five years, indicating that the alleged offence is not of the gravest category warranting prolonged judicial custody.

➡️ The Court relied on the Supreme Court’s decision in Ratnambar Kaushik, observing that prolonged incarceration and likely delay in trial are valid grounds for granting bail in GST-related prosecutions.

➡️ Bail was granted on conditions: personal bond of ₹5 lakh with two solvent sureties, mandatory appearances before the trial court, and compliance with Section 480(3) of the Bharatiya Nagarik Suraksha Sanhita, 2023, including non-tampering with evidence, surrender of passport, and location sharing, with authorities free to act on any breach.

✔️ Madhya Pradesh HC - Shivam Sadhwani vs Union of India and Others [MISC. CRIMINAL CASE No. 58256 of 2025]

#GST #GSTUpdate #GSTCaseUpdate #AdvBimalJain #GSTwithBimalJain #a2ztaxcorpllp #GSTUpdate #GSTcaseLaw

The GST amendments in the Union Budget 2026 have been limited but they signal meaningful progress for businesses and trade facilitation.

Details here 👇

🟡 Amendments in Section 15 and Section 34

Section 15(3)(b) has been proposed to be amended to omit the requirement of establishing the post-sale discount in terms of an agreement entered into before or at the time of supply and specifically linking of the same with relevant invoices.

Credit notes are now recognised as a valid route for post-sales discount, thereby bridging the gap between valuation provisions and issuance of credit notes.

Major announcements benefiting industry and trade in the #ViksitBharatBudget:

✅₹12.2 lakh crore Capex allocation

✅India Semiconductor Mission 2.0 to design Indian IPR & fortify supply chains

✅Electronics Components Manufacturing Scheme outlay up to ₹40,000 Cr

✅₹10,000 crore SME Growth Fund, ₹2,000 crore top-up to Self-Reliant India Fund

✅Allocation of ₹10,000 crore for container manufacturing

✅SHE-Marts for rural women-led enterprises

✅City Economic Regions: ₹5000 Cr per CER over 5 years

✅Scheme to revive 200 legacy industrial clusters

✅Tax holiday till 2047 to any foreign company providing cloud services globally by using data centre services from India

✅Biopharma SHAKTI scheme: ₹10,000 Cr over next 5 years

✅₹20,000 Cr over 5 years for Carbon Capture Utilisation and Storage

✅Integrated program for labour-intensive Textile Sector

✅Support to states for 3 dedicated Chemical Parks

✅7 high-speed rail corridors as growth collectors

✅5 University townships near major industrial & logistic corridors

✅AVGC content creator labs in 15000 secondary schools & 500 colleges

✅Scheme to establish 5 regional hubs for medical tourism

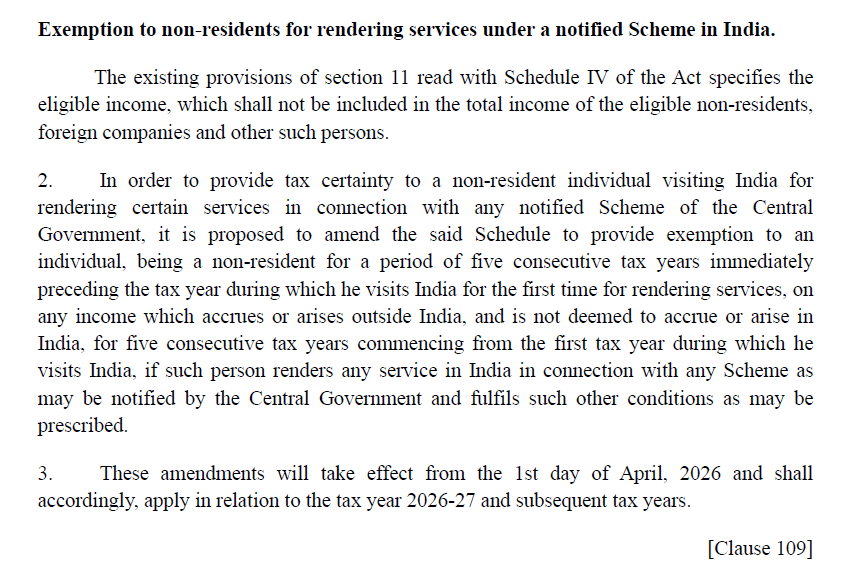

Exemption to attract Global Talent. Good Move.

To attract global experts, the government has proposed that non resident individuals visiting India under a notified Central Government scheme will be taxed only on Indian sourced income. Their foreign income will remain exempt for five consecutive years, even if they stay in India.

This applies if the individual was a non resident in the preceding five years and will be effective from 1 April 2026, applicable from tax year 2026 27 onwards.