Then : Cheque Clears within 3 days

Now : - Cheque Clearing taking more than 7 days

W rule of 1 day Cheque Clearing System. Bank Staffs are not trained. Entire Banking system failed.

Clause 23 of #taxaudit - Payment made to Person specified u/s 40A(2)(b) !

📌Relatives as per S.2(41) husband, wife, brother, sister, lineal ascendant or descendant -to be considered for reporting

📌Don’t confuse it with the much wider “Relative” definition of Sec 56.

📌Eg.-Payments to brother-in-law, uncle, etc. are outside S. 2(41) → not reportable.

📌Additional reporting = incorrect reporting!

[Follow for more such trivia/updates on #TaxAudits]

⚠️ Missed the ITR Filing Deadline? What’s next? 🧵

⏳ Deadline gone? Don’t panic. Options still exist. Let’s decode 👇

1.📝 Belated Return = Your Second Chance: -

You can file till 31 Dec 2025 (unless CBDT extends).

2. ❌ Consequences of Filing of Belated Return: -

➡️Late Fee u/s 234F (₹1,000 if income ≤ ₹5 lakh, else ₹5,000)

➡️Interest on tax dues (u/s 234A/B/C)

➡️Losses (except house property) cannot be carried forward

3. Refund Still Possible?

✅ Possible - but with delayed processing & reduced interest.

4. 🚨 Miss 31 Dec Too? : -

Only option left 👉 Updated Return (ITR-U) within 2 years, with extra tax (25%–50%).

File ASAP. Delay = More cost + Less benefit.

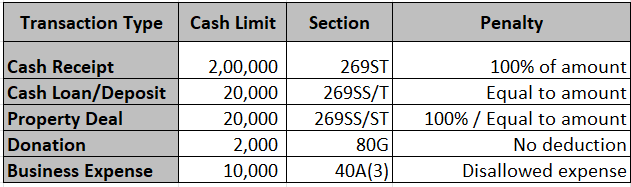

🧾 Cash Transaction Limits under Income Tax Act

Not all cash transactions are allowed — cross certain limits and you may face penalty up to 100% of the amount!

Here’s a quick guide 🧵

1. 💰Cash Receipt Limit – ₹2,00,000 (Sec 269ST)

You cannot receive ₹2 lakh or more in cash:

🚫 From one person in a day

🚫 For a single transaction

🚫 For transactions relating to one event/occasion

✅ Must be through cheque, draft, or digital mode.

2. ⚠️ Penalty (Sec 271DA):

If you receive ₹2 lakh or more in cash in violation of Sec 269ST →

💥 Penalty = 100% of the cash received

3. 🏦 Cash Loan/Deposit Limit – ₹20,000 (Sec 269SS & 269T)

You can’t:

🚫 Take or accept a loan/deposit in cash > ₹20,000

🚫 Repay loan/deposit in cash > ₹20,000

✅ Must be via account payee cheque, draft, or electronic mode.

4. ⚖️ Penalty (Sec 271D & 271E):

Violation = Penalty equal to the loan/deposit amount

e.g. Accept ₹50,000 in cash → Penalty ₹50,000

5. 🏘️Property Transactions – ₹20,000 Limit

No person can accept ₹20,000 or more in cash for:

➡️Sale of immovable property

➡️Advance or consideration

Always use banking channels.

6.🎁Donations & Expenses in Cash:

🚫 80G donations above ₹2,000 not eligible for deduction.

🚫 Business expense in cash > ₹10,000 per day (per person) not allowed as deduction (Sec 40A(3)).

7.🚨 Takeaway:

Avoid large cash dealings.

Use banking channels — safe, traceable & tax-compliant.

Cash may look easy, but penalties are costly! 💸

𝐁𝐢𝐠 𝐬𝐚𝐯𝐢𝐧𝐠𝐬 𝐨𝐧 𝐞𝐯𝐞𝐫𝐲𝐝𝐚𝐲 𝐞𝐬𝐬𝐞𝐧𝐭𝐢𝐚𝐥𝐬 𝐰𝐢𝐭𝐡 #𝐍𝐞𝐱𝐭𝐆𝐞𝐧𝐆𝐒𝐓! With GST 2.0, taxes on common food items and household products have been reduced, making them more affordable. From milk and butter to biscuits, noodles, and even packed juices—families can now enjoy quality essentials without the extra burden of high tax rates. #GSTBachatUtsav #BachatUtsav #NextGenGST #GSTReforms #JagoGrahakJago #ConsumerAwareness

![AbhasHalakhandi's tweet photo. Clause 23 of #taxaudit - Payment made to Person specified u/s 40A(2)(b) !

📌Relatives as per S.2(41) husband, wife, brother, sister, lineal ascendant or descendant -to be considered for reporting

📌Don’t confuse it with the much wider “Relative” definition of Sec 56.

📌Eg.-Payments to brother-in-law, uncle, etc. are outside S. 2(41) → not reportable.

📌Additional reporting = incorrect reporting!

[Follow for more such trivia/updates on #TaxAudits]](https://pbs.twimg.com/media/G2lePR8XYAAo9P2.jpg)

![AbhasHalakhandi's tweet photo. Clause 23 of #taxaudit - Payment made to Person specified u/s 40A(2)(b) !

📌Relatives as per S.2(41) husband, wife, brother, sister, lineal ascendant or descendant -to be considered for reporting

📌Don’t confuse it with the much wider “Relative” definition of Sec 56.

📌Eg.-Payments to brother-in-law, uncle, etc. are outside S. 2(41) → not reportable.

📌Additional reporting = incorrect reporting!

[Follow for more such trivia/updates on #TaxAudits]](https://pbs.twimg.com/media/G2lfODsWIAAG2gx.png)