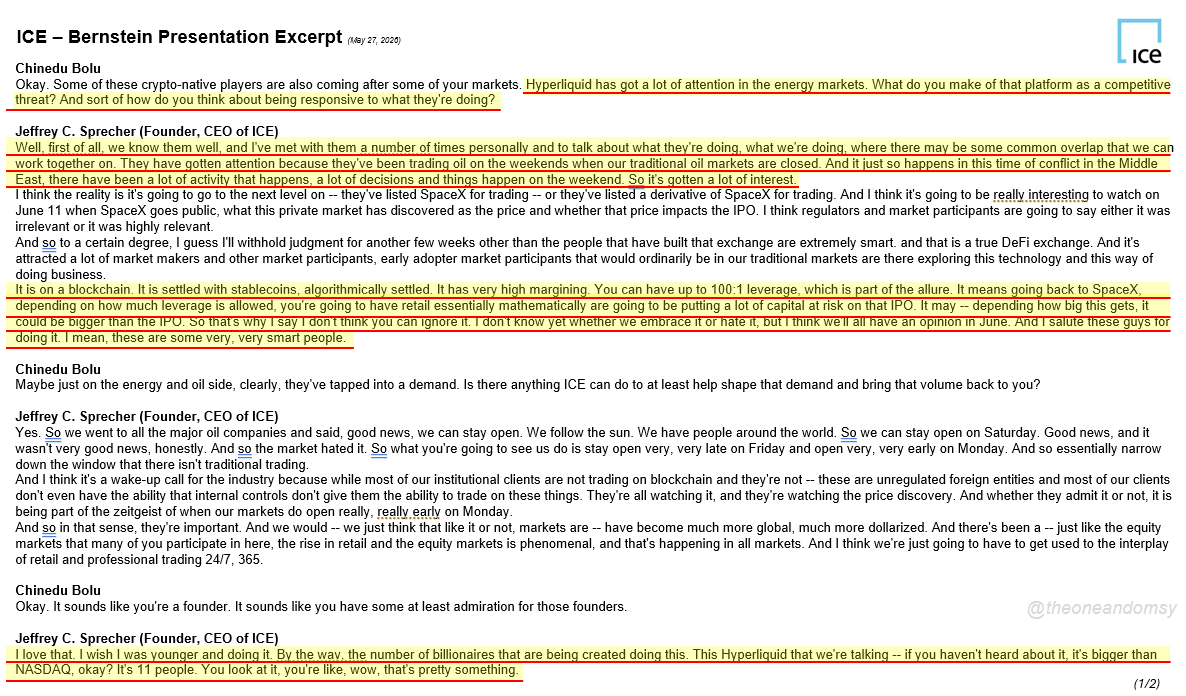

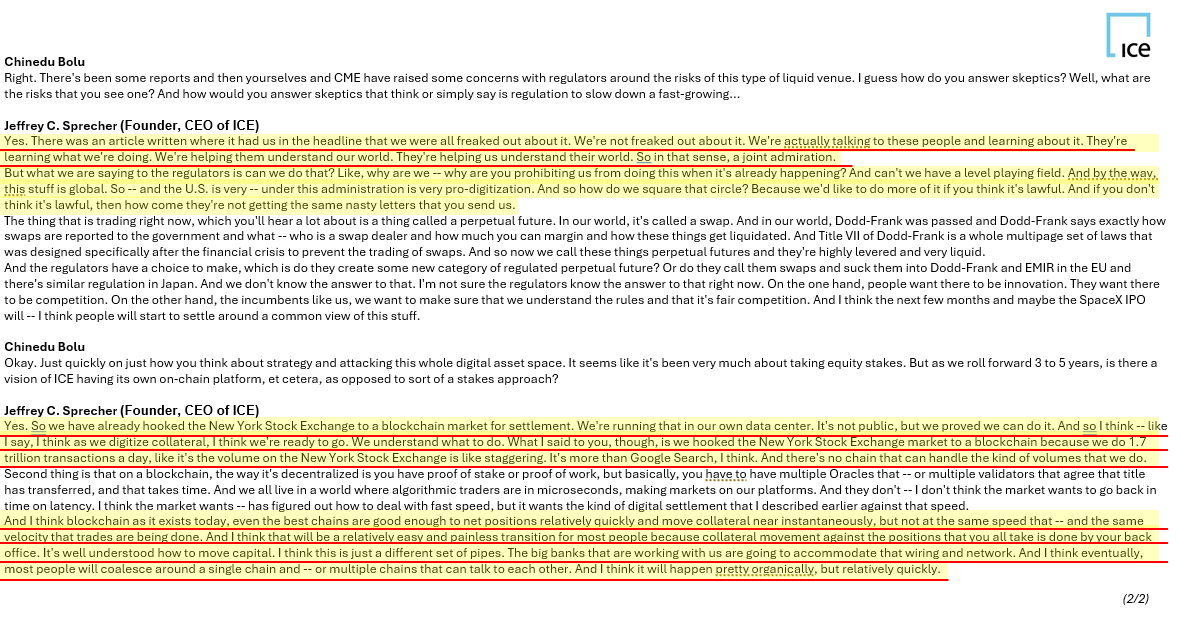

Jeff Sprecher, founder and CEO of $ICE (owns the NYSE) on Hyperliquid:

"This Hyperliquid that we're talking -- if you haven't heard about it, it's bigger than NASDAQ, okay? It's 11 people. You look at it, you're like, wow, that's pretty something."

If it wasn't clear before, hyperliquid:native has grown far beyond crypto. The incumbents have noticed, are paying close attention, and even spending time with the team

Bernstein excerpt below and worth the read imo:

Trader Mayne says HYPE is one of the only altcoins that could survive multiple bull runs

“It’s not like your other altcoins. There’s a real business here that makes real money, that has a real strategy, that buys back the token. I believe Hyperliquid is up over $1B on token buybacks”

“This is one of those coins that can have multiple bull runs where the all time high it made in this cycle is not its forever all time high”

“There’s a good chance that the vast majority of altcoins from this last cycle, the vast majority of memecoins that people on twitter tricked you into buying will never see all time highs again”

“HYPE is different”

Despite $HYPE trading at ATH price, OI is nowhere near ATH while still trading under market cap ATH.

The only true deflationary asset in all of crypto.

Hyperliquid.

Non-custodial DEX with full CEX feature parity ASAP should be the end goal.

There are CEX features (coin margin/UTA, privacy/prime brokers, earn tab, options, structured products/native aligned stablecoin) still lacking on HL right now.

It does not matter to me who builds them as long as we get these features used by as many users as possible ASAP.

Hence, my approach to the HyperEVM is to use it as if there were no points.

This mainly involves adding native staking yield to my HYPE collateral (LSTs) and borrowing against aforementioned yield generating collateral (Lending protocols) for leverage when needed.

Any additional points earned is just an added bonus and I’ll be using them without these points anyway.

Without complete information, I can only make guesses but I believe the BLP will result in an increase in nett new borrowing which should spillover into the rest of the ecosystem.

Hyperliquid will win long term.

TLDR: During recent volatility, Hyperliquid had 100% uptime with zero bad debt. This was Hyperliquid’s first cross-margin ADL in more than 2 years of operation. ADL does not change the outcome for any liquidated users. While some specific ADL providing trades were unfavorable, the aggregate effect of ADL was that traders realized significant pnl by closing positions at favorable prices that were only briefly available.

--

It’s sad to see some people attack Hyperliquid to deflect from their own platforms’ issues. Solvency and uptime are the two most important properties of a financial system. These are table stakes for any trading system, and gaslighting to convince users otherwise is unethical and irresponsible.

Below is more analysis on how Hyperliquid’s margining system handled the extreme volatility.

Background on liquidations

For a perps system to be solvent, every position must be backed by a minimum amount of collateral. This is called the “maintenance margin.” When positions do not meet the maintenance margin requirement, they are taken over by the system to be liquidated. Earlier today, many altcoins dropped by more than 50% in a short period of time. When this happens, long positions at 2x or higher leverage must be liquidated, or else the system accrues bad debt.

There were billions of dollars worth of positions liquidated on Hyperliquid in a matter of minutes. In a permissionless system, each user chooses their own position sizing and collateralization. Any system that does not liquidate the necessary users is irresponsibly gambling with other users’ funds. On Hyperliquid, every order, trade, and liquidation is transparently verifiable onchain. Many other venues significantly under-report liquidation data. This cannot be compared apples-to-apples against the fully onchain picture of Hyperliquid.

Background on HLP

HLP is a protocol vault with permissionless deposits that 1) provides order book liquidity and 2) performs backstop liquidations. The first role is negligible, with HLP trading less than 1% market share. The focus of this post is liquidations.

Liquidations are first attempted against the order book, and any user can provide liquidity to these market liquidations. Backstop liquidations occur when the order book does not have enough liquidity to absorb an undercollateralized position. In this case, HLP takes over the position along with its collateral. For improved risk management, HLP is split into several child vaults, and each liquidation is only sent to one child vault.

Background on ADL

Auto-deleveraging (ADL) is the liquidation mechanism of last resort, when market and backstop liquidations do not work. See Doug’s thread (link in reply) for a thorough explanation on the details of ADL.

Every ADL event has two sides: the “triggered” side is undercollateralized, while the “providing” side is decided as a function of profitability and leverage used.

Similar to backstop liquidations, even though providers to ADL are profitable on average, there are no guarantees for any specific event. Some ADL providing trades were unfavorable, such as when only some components of long/short portfolio were closed. The system is designed to minimize ADLs because they are unpredictable even if ADL providing trades are profitable on average. Because HLP is a non-toxic backstop liquidator, ADL is a rare settlement of last resort. As far as I know, this was the first cross-margin ADL event on Hyperliquid mainnet (ADL is more common for isolated-only assets such as hyperps, which are not backstop liquidated by HLP).

Summary of events

Over the course of 20 minutes, HLP backstop liquidated billions of dollars worth of positions.

HLP's philosophy has always been to provide liquidity of last resort. Contrary to misconceptions, HLP is a non-toxic liquidator that does not pick profitable liquidations. Instead HLP is a public good for maintaining system solvency. In particular, Hyperliquid has no liquidation fees. HLP’s design, including its multi-component child vault system, is the product of countless simulations, and allows HLP to maximally serve the benefit of the protocol while managing its own risk.

In fact, the liquidator child vaults of HLP themselves became undercollateralized in the course of backstop liquidating as many user positions as possible. This is by design, where child vaults are isolated from the other components of the overall strategy. HLP is treated no differently from other users when participating in ADL. In aggregate, HLP's child vaults were the largest addresses on the triggered side of ADL by more than an order of magnitude. The addresses on the providing side of ADL against HLP’s child vaults realized hundreds of millions of dollars in additional profit relative to the prices shortly before and after the dislocation.

On other venues, the liquidation engine is not transparent and therefore may not be subject to the same strict margin requirements as for normal users. On these venues, the exchange could have backstop liquidated more positions, bearing increased solvency risk to extract hundreds of millions in business revenue. This is not an acceptable tradeoff for Hyperliquid.

Finally, I know that this is a difficult time for many traders, and I hope the community can continue to support each other and grow together. As a contributor to Hyperliquid, I’ll continue to work my hardest to build the best possible platform that can house all of finance. Times like this highlight the importance of transparency and fairness in the financial system.

A common question I’ve heard in Seoul is: what makes Hyperliquid special? I haven't found a way to distill it all into a sentence, but one reason that stood out to me the past few days is the culture of dreaming big and executing, while staying true to the original ethos of defi: integrity, fairness, and transparency. The work is hard, and there are many crucial components to be built. But that’s the beauty of the Hyperliquid community. Builders rise to the challenge and push the frontier of what is possible. I’ve never been more excited to continue building alongside everyone.

Since beginning work on Hyperliquid a few years ago, this was my first time traveling to meet so many community members, and also my first time in Korea. Thank you to @hlh_build organizers @hyperpc_ and @B__Harvest for an incredible hackathon, to @christyhwchoi for the thoughtful fireside chat at KBW, and to @SKYGG_Official/@hypurrcorea, @hypurr_co, and @Hyperliquid_KR for tonight’s community event.

Most of all, thank you to the builders, traders, and community members who give Hyperliquid its soul. I’m blown away by the hospitality, energy, and talent growing every day. There’s a long journey ahead to house all of finance, but it’s good to appreciate how far we’ve come together.

What is special about building in Hyperliquid in the words of Jeff

“The culture, it really is the people”

“People don’t want to converge on something that is extractive”

“Real builders are here for the long run, and want to join to stick it out through thick and thin”

“Integrity, hard work and excellence”

“That is what makes us special”

“You guys are all the team”

Hyperliquid.

$HYPE

Never thought I’d be interviewing the former CEO of Barclays, let alone for it to be about Hyperliquid!

Hyperliquid

@rediamondjr@dschamis

https://t.co/FCjVjDGdmz

The labor-growth link is breaking, and that changes how we read payrolls, unemployment, and inflation risk.

In our latest ledger, we unpack the data, charts, and macro models behind this shift.

Read the full report here: https://t.co/yF0ohaR0wv

After a lot of thought, I've decided to put my support behind Native Markets

I was initially skeptical of going with a new small team vs Paxos (my first choice initially)

After all, why pass up the opportunity to bring a big player like Paxos (or Ethena) into the ecosystem

But the reality is, they're entering the eco regardless (& if they wouldn't, they'd be a bad partner anyway)

But after more reflection, I have a different question - why does a big issuer like Ethena/Paxos/Agora/Frax need to be gifted a front-row seat?

Will they fight for Hyperliquid the same way Hyperliquid is giving them a fighting chance with the USDH ticker?

Would they go to war for Jeff in 2028 when there's a blue sweep & AOC threatens to revoke every stablecoin issuer's banking license?

Will a non Hyperliquid-first team invest as heavily in HIP-3 markets & alternative frontends?

As we continue laying the foundation to house all of finance, it only makes sense to prioritize a maximally aligned team who has been all-in on Hyperliquid from the start.

And don't underestimate Native Markets' expertise! @Mclader started Blackrock's digital assets & blockchain strategy, @anishagnihotri brings experience from Ritual & Paradigm (& my smarter friends speak highly of him non-stop), and you all know @fiege_max, have never heard a bad word about him from anyone, probably singlehandedly responsible for getting the Hyperliquid ecosystem to where it is today.

I'm a big fan of the teams at Paxos, Ethena, & Sky - less familiar with Frax & Agora - & look forward to welcoming all of them to Hyperliquid

In fact, I hope they all buy tickers this week & begin the process of permissionlessly deploying their own Hyperliquid-native stablecoins (& eventually also getting added as spot quote assets, & then collateral for perps markets).

Because Hyperliquid is the home for ALL of finance & welcome to all issuers.

It needed a native protocol for spot asset issuance & it got Unit.

Now it needs a native stablecoin issuer & my bid is for Native Markets.