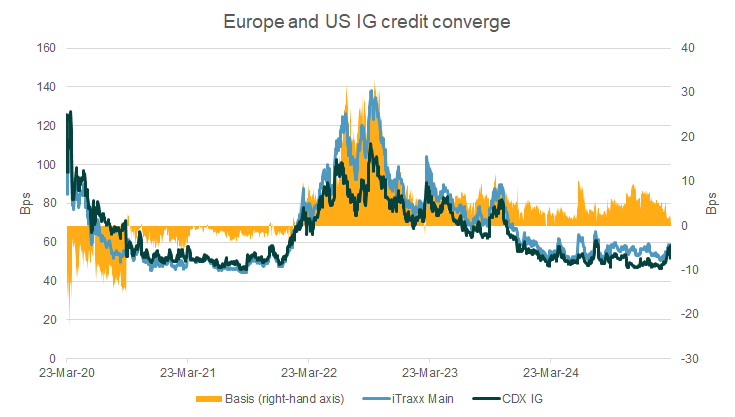

European and US IG credit spreads have converged, a stark difference from the post US election euphoria. Join our webinar on March 27 to find out more https://t.co/ohoOruKwbW

US sovereign CDS has rallied following weekend news of a debt ceiling deal (which still has to be passed by Congress). The 5-year spreads tightened by 15bps to 42bs, while the 1-year- which has borne the brunt of perceived credit deterioration - rallied by 80bps to trade at 54bps

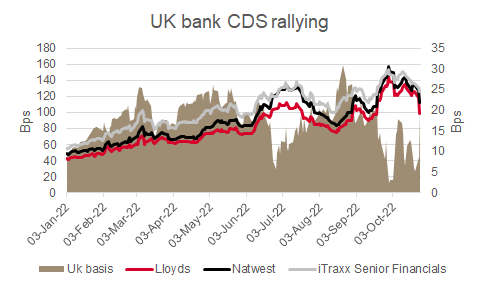

Positive day for European financials but UK bank CDS in particular outperformed as a semblance of stability returned to the country's government. They typically trade tighter than the iTraxx Senior Financials but started to converge on the index in recent weeks amid the turmoil

UK 5-year CDS 5bps tighter at 30bps following Sunak victory. Now at same level as before mini budget, though still 20bps wider than at start of the year

The iTraxx Europe traded 23bps wider than its counterpart in North America (CDX IG) today. This is the largest basis since the aftermath of the eurozone debt crisis in Q3 2013.

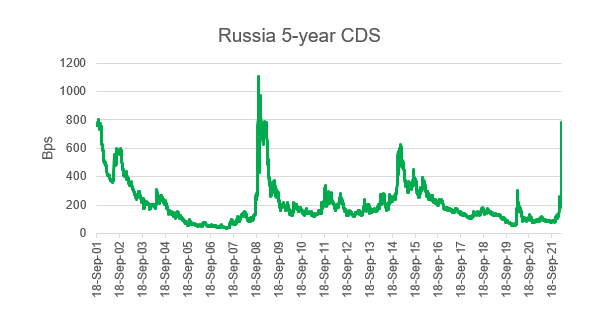

Russia 5-year CDS is 350bps wider at 780bps, well in excess of the levels seen after the Crimea annexation but not quite reaching spreads seen at the height of the GFC. Credit curve has inverted.

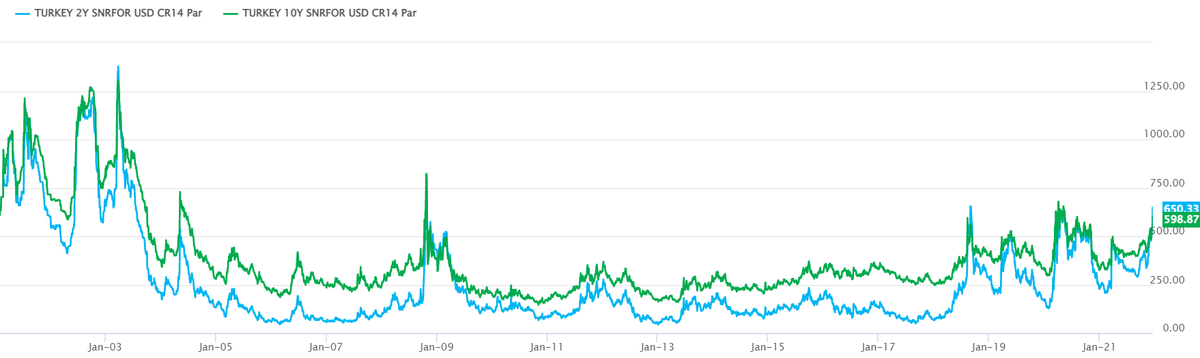

Turkey's CDS curve has inverted due to the latest in a series of interest rate cuts leading to another currency crisis. Last year saw three EM sovereign credit events - the first time this has happened. Will 2022 be another year where EM credits come under pressure?

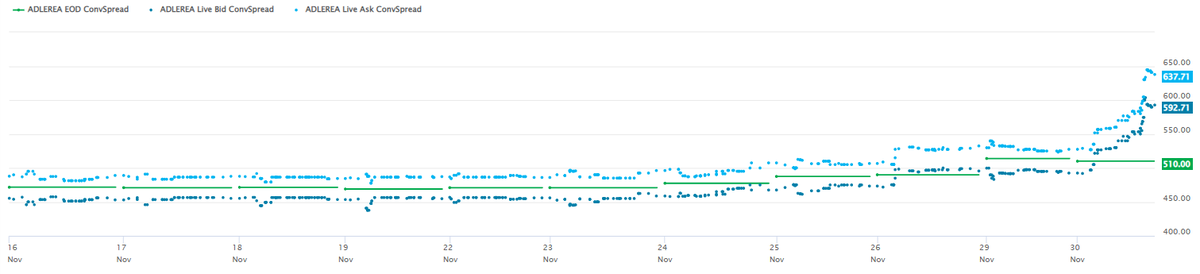

Omicron continues to drive credit spread direction but idiosyncratic risk can't be ignored - German real estate firm Adler 5-year CDS over 100bps wider today at 615bps following its refusal to answer questions on an investor call

US sov CDS curve flattening at short-end ahead of debt ceiling deadline. Liquidity is relatively weak, likely a handful of large trades by asset managers moving the market. 6-month spreads at 13bps, still some way off the 77bps hit in 2013, the last debt ceiling standoff

Turkey's 5-year CDS widening by another 5bps to 417bps after the unorthodox rate cut yesterday. Still some way off the 600bps levels seen last year but its a glaring anomaly given Brazil and others are raising rates. Turkey' notable underperformer since 2018 when gov intervened

China's sovereign debt has proved resilient to contagion talk emanating from Evergrande default risk. But today that started to change today - China's 5-year CDS widened by 9bps to 45bps, its widest level in nearly a year.

Russia 5-year CDS opened 15bps wider at 120bs following news on new US sanctions targeting Russian sovereign debt. But spreads have since recovered to 110bp. This would make it a relatively insignificant move, perhaps a reflection of Russia's ability to withstand exogenous shocks

Foreign investors have been pulling as much money out of Turkish stocks and bonds as at the height of COVID-19 in March 2020. So while everyone in EM is struggling with the fall-out from higher US long-term interest rates, only Turkey is in the midst of a terrible sudden stop...