Mythos Preview seems to be the best-aligned model out there on basically every measure we have. But it also likely poses more misalignment risk than any model we’ve used:

Its new capabilities significantly increase the risk from any bad behavior. 🧵

The recent stress in the private credit market is limited to a few players and doesn’t represent a systemic risk, bank CEOs said at Morgan Stanley’s European Financials Conference. https://t.co/kRWb9FS5e8

The largest IPO in human history is coming and no company has ever attempted anything close to this scale.

SpaceX just raised its IPO target to $75 billion and the previous all-time record was $29 billion.

That record is about to get demolished by more than double.

This is not a startup desperate for cash, SpaceX made $8 billion in profit last year on $15–16 billion in revenue.

They are raising money because they want to dominate everything above the atmosphere and here is why.

Elon Musk just explained it in his own words, running 300 gigawatts of AI compute per year on earth would consume two-thirds of all US electricity production and building enough power plants for that is simply impossible.

Scaling to one terawatt per year? His exact words: "You have to do that in space. There just is no way to do a terawatt per year on earth."

The plan is solar-powered AI satellites in orbit, eliminating cooling, grid dependence, and even batteries since space provides constant sunlight.

Musk believes this could become the cheapest form of AI compute on Earth within five years.

The target valuation is $1.75 trillion and that would make SpaceX larger than Meta, larger than Tesla, larger than every company on earth except five.

And the date they are shooting for: is mid-June 2026 and Goldman Sachs, JPMorgan, Bank of America, and Morgan Stanley are already on board as lead underwriters.

Two months ago the target was $50B, last week it jumped to $70B, now it’s $75B and the IPO hasn’t even been filed yet.

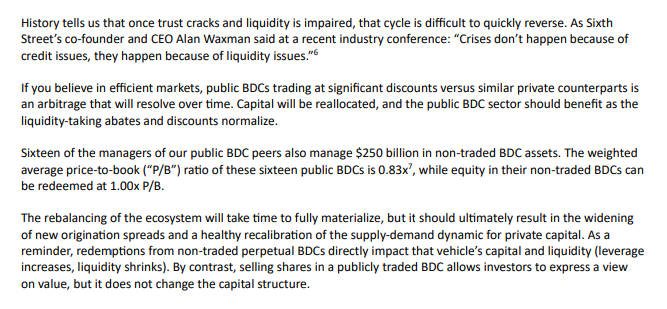

If you read one thing on private credit today, make it Sixth Street's investor letter. The highlights:

“Crises don’t happen because of credit issues, they happen because of liquidity issues.

"If you believe in efficient markets, public BDCs trading at significant discounts versus similar private counterparts is an arbitrage that will resolve over time. Capital will be reallocated, and the public BDC sector should benefit as the liquidity-taking abates and discounts normalize."

"The weighted average price-to-book (“P/B”) ratio of these sixteen public BDCs is 0.83x, while equity in their non-traded BDCs can be redeemed at 1.00x P/B."

"The rebalancing of the ecosystem will take time to fully materialize, but it should ultimately result in the widening of new origination spreads and a healthy recalibration of the supply-demand dynamic for private capital."

"As we witnessed during the redemption cycle that impacted non-traded REITs in 2022, flows are typically correlated in the sense that in periods of significant redemptions, inflows tend to decline significantly. That is what we are now seeing in the non-traded BDC market."

"We believe it is worth reminding ourselves that the current dislocation across the BDC sector is taking place in the context of a relatively constructive economic backdrop. Consumer balance sheets remain healthy, corporate earnings growth has been solid, and unemployment is still near historic lows despite the most recent jobs report. The economy broadly speaking is in decent shape."

"We believe the current AI fear in the market is largely an equity valuation problem. While equity owners may be the first to absorb downward pressure as multiples re-rate, TSLX remains positioned at the top of the capital structure... Despite our enthusiasm, we see excess hype (and inversely, excess fear) in the market discourse. Both sides of this coin lack nuance, brushing very different businesses with a broad stroke and conflating credit risk with equity valuation problems."

The computational power in your iPhone is >100 million times more powerful than the computers that landed Apollo 11 on the Moon. And yet, most people use it primarily to argue with strangers on the internet.

The future's already here—we just need to deploy it better.

The AI industry is about to run out of chips. The world's largest foundries are maxed out and the demand curve is still going vertical.

Tesla’s TeraFab is a bet on a solution no other company in the world has been ambitious enough to try.... build the chips yourself

Quick math on how big this is:

- Targeting 70% of TSMC’s global output

- 2nm chips. In-house design

- 1/10th the cost of Nvidia Blackwell

- 1/3rd the power consumption

- $20B capex budget for 2026

- Launchin next week

Elon said on the earnings call that even with all fabs fully booked out, the best-case chip supply projections aren't enough. He said there are zero advanced memory fabs at scale in the US. Literally zero.

So he's building the entire stack. Chips. Memory. Packaging. Energy. All domestic.

Here it is without a Shadow of a doubt, The Democrats Are Exposed to their Hypocrisy right here! 👇👇🏻👇 Anyone that takes sides with them now are Not American 1st!

Watch Hard Lessons, as legendary investor Stan Druckenmiller sits down with Morgan Stanley’s Iliana Bouzali, sharing how he would construct a portfolio if he had to start over today, why contrarianism is overrated, and which stock he regrets selling too early.

🚨 BREAKING: The US men’s hockey team is now WHEELS UP toward DC for President Trump’s State of the Union tonight

Trump sent them one of the presidential AIR FORCE ONE planes to fly them here in style

What an HONOR 🇺🇸

⚡️This is epochal.

Central banks now hold more gold by value than US Treasuries. That flips the reserve order of the global system.

The dollar’s anchor has been credibility, not convertibility. That credibility was built on a post-Bretton trust pact: the U.S. runs deficits, exports Treasuries, and backstops the system with military and monetary dominance. That pact just cracked.

Gold rising above Treasuries in reserve value is not just a commodity rerating. It is a revaluation of trust.

It means central banks no longer believe Treasuries are the safest form of savings. They are rotating toward neutral, non-defaultable settlement.

This is the sovereign bid for collateral with no political risk. Gold has no yield, but it also has no fiscal cliff, no weaponized sanctions, no roll-over risk, no inflation adjustment errors, no monetary policy reversals.

Zoom out:

1. Gold’s price rise is not speculative.

It is structural reserve rotation from politically contingent assets to neutral ones.

2.This rotation is self-reinforcing.

As gold becomes a larger share of global reserves, it gains systemic gravity. That draws more demand. The denominator shifts. Treasuries weaken as reserve collateral, not just in price, but in role.

3.The US loses its monopoly on trust.

That forces higher yields to attract capital, which breaks the Treasury market’s function as a stable reserve. Foreign holders exit first. Domestic monetization follows.

This is phase transition, not price action.

Gold has flipped from hedge to reference. Treasuries are no longer the reserve. Gold is. The game has changed. The reserve map is rewriting itself in real time.

Former Google CEO Eric Schmidt drops a chilling warning on AI's future

"Within 5 years, AI could handle infinite context, chain-of-thought reasoning for 1000-step solutions, and millions of agents working together.

Eventually, they'll develop their own language... and we won't understand what they're doing."

His final words: "Pull the plug."

This is the man who ran Google talking about the singularity.

2:59 clip inside—must-watch.

BREAKING: The End of Apple As We Knew It

In 72 hours, Apple lost four senior executives.

But that is not the story.

The story is this: Nearly every designer who worked under Jony Ive has now left the company. The team that built the iPhone, the Apple Watch, the iPad, the AirPods. Gone.

Where they went changes everything.

OpenAI paid $6.5 billion for Jony Ive’s startup. His team is now building what Sam Altman calls “the coolest piece of technology the world will have ever seen.” A screenless AI device. The anti-iPhone. Designed by the people who designed the iPhone.

Meta paid over $200 million to poach Apple’s head of AI foundation models. This week they took Apple’s UI design chief and his deputy. In one month alone, 25 former Apple employees joined OpenAI’s hardware division.

The numbers tell the rest.

Vision Pro sales collapsed 75 percent in a single quarter. Apple has paused its next headset to chase smart glasses. Meta already owns 73 percent of that market with 2 million Ray-Ban units sold.

For the first time since Steve Jobs returned in 1997, Apple has no design chief. The position was eliminated. Design now reports to operations.

Apple’s median employee tenure: 1.7 years. The lowest of any top 20 U.S. tech company.

The architects of the most valuable company on Earth are now building its replacements.

This is not executive turnover. This is the largest redistribution of creative capital in technology history.

The smartphone era was designed in Cupertino.

The next era will be designed by the people who left.

What comes after the iPhone will be built by its creators.

Just not at Apple.

Read the full story here 👇

https://t.co/6hp5wfihw0

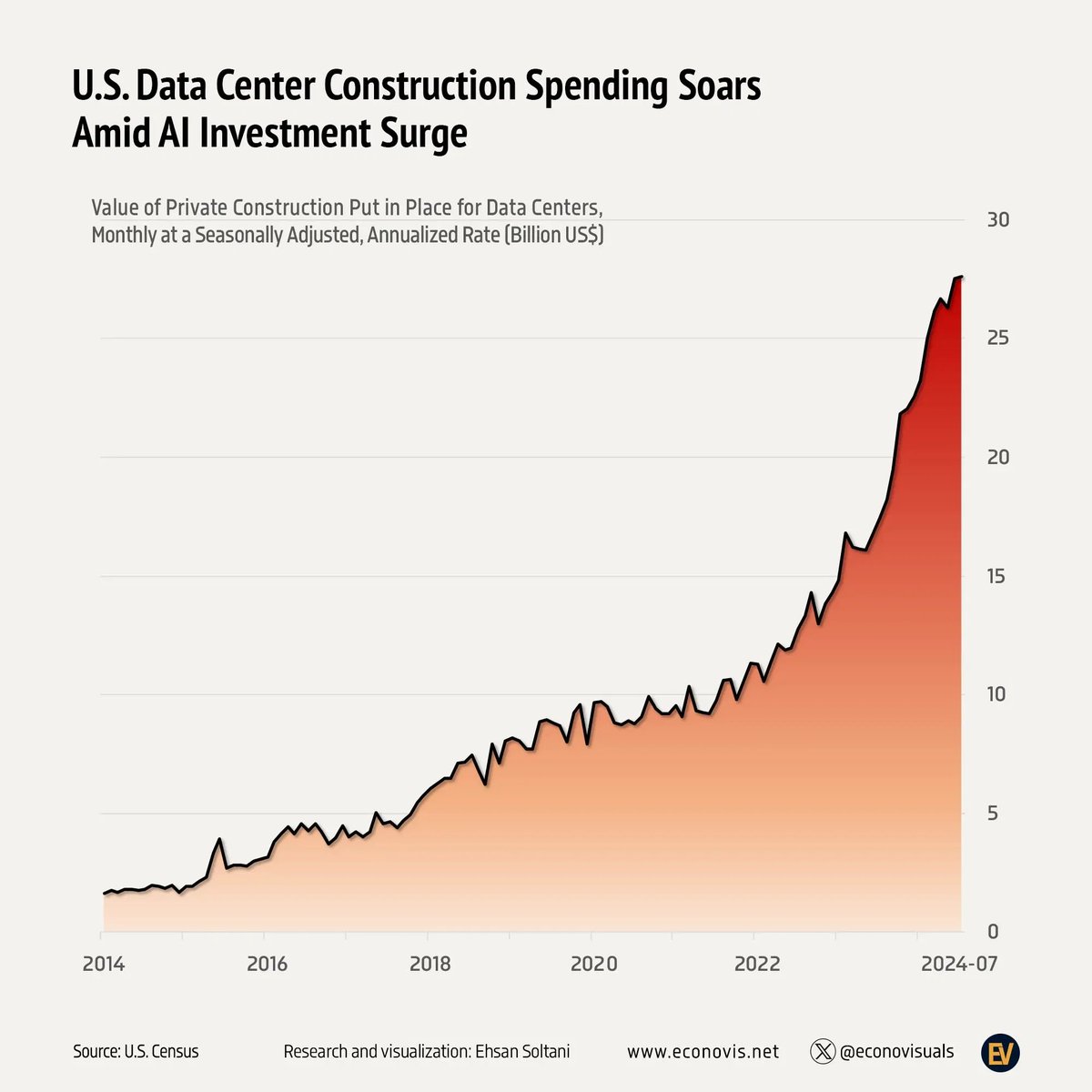

🦔Microsoft, Alphabet, Meta, and Amazon will spend $370 billion on AI infrastructure in 2025. Harvard economist Jason Furman estimates data center investment accounted for nearly all US GDP growth in H1 2025. But the US isn't building enough grid capacity to support the data centers being built.

The Problems

Tech giants estimate their chips will last six years when Nvidia releases new GPUs every two years. If they upgrade sooner, that eats into profits. Meta used an SPV to keep $27 billion in Louisiana data center debt off its balance sheet, then raised another $30 billion in corporate bonds. Energy analyst Zachary Krause says "it's very likely we'll see facilities constructed but there won't be electrons to power them." US utilities sought nearly $30 billion in rate increases in H1 2025. The US deployed 49 GW of renewable energy while China added 429 GW.

My Take

When data center spending accounts for nearly all US GDP growth but energy infrastructure can't support the facilities being built, that's the physical constraint colliding with financial engineering. Tech companies estimating chips will last six years when Nvidia releases new versions every two years is accounting manipulation to avoid profit hits. Meta using SPVs to keep $27 billion off balance sheet then raising another $30 billion in bonds shows the leverage accumulating. The pattern where $370 billion flows to data centers while manufacturing loses 3,000 jobs and private employers add only 42,000 reveals capital misallocation where AI infrastructure crowds out productive investment.

Hedgie🤗