Zaki Abbas Nasser 🔥

Low Profile Micro-Cap Allocator

Very underrated amongst other investors

Focuses on niche engineering and turnaround pharma companies poised for structural value migration.

Net Worth Growth Over time

Mar 2022: ₹10 Crore across 3 stocks

Jun 2023: ₹67 Crore across 9 stocks

Mar 2024: ₹120 Crore across 16 stocks

Now His Portfolio Stands At A Record ₹256 Cr Across 17 High-Conviction Holdings. 🔥

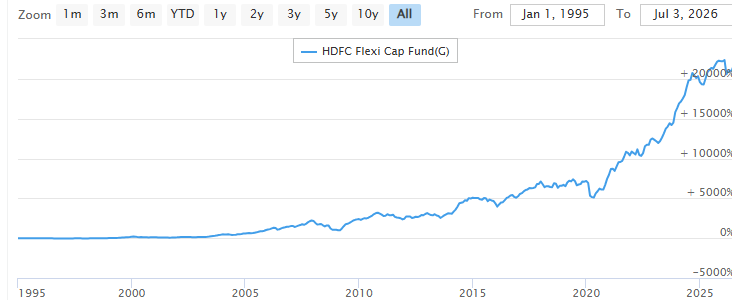

🎯🎯 HDFC Flexi Cap 🎯🎯

⚡️10 - 2000 NAV Journey ⚡️

📈1-Jan-1995 : 10 NAV

📈11-Oct-1999: 20 NAV

📈22-Dec-2003 : 50 NAV

📈28-Nov-2005 : 100 NAV

📈26-Oct-2007 : 200 NAV

📈23-May-2014: 400 NAV

📈4-Feb-2021 : 800 NAV

📈11-Oct-2021 :1000 NAV

📈27-Dec-2023 : 1500 NAV

📈05-July-2026 : 2034 NAV (Today )

It took 4.9 Years for HDFC Flexi Cap NAV to move from 10 to 20 ( 100% jump)

NAV Jump from 1000 to 2000 in 4 year past 4 year

This Journey is your mutual fund Journey if you stay invested in any scheme for 25-30 year.

Mutual fund investments are subject to market risks. Please read the scheme information and other related documents carefully before investing. Past performance of the schemes is neither an indicator nor a guarantee of future performance.

#SIP

Multi-baggers and the ₹100–1,000 Cr PAT Transition

if you run below query on Screener, you will get 250+ names.

Profit after tax > 100 AND

Profit after tax < 350 AND

Sales growth 5years median > 15

Some of your next 5x opportunities are sitting in that list!

Here is the backdrop:

Amit Jeswani (@Amit_Jeswani1) famously mentioned at an @ias_summit event a few years ago that most multi-baggers are created during the journey from ₹100 Cr to ₹1,000 Cr in PAT.

By the way, the next IAS Event is just about a month away! Keep a close eye on it - it's an annual ritual!

Coming back to our topic, a recent textbook example of this phenomenon was MCX.

MCX reported a PAT of ₹149 Cr in FY23, which dropped to ₹83 Cr in FY24, largely due to the technology contract issues that played villain during that phase.

Post those setbacks, the turnaround has been phenomenal: PAT jumped to ₹560 Cr in FY25, and in FY26, MCX has delivered ₹1332 Cr.

Unsurprisingly, the stock has delivered > ~10x returns over the last three years.

Another powerful example is Laurus Labs. Laurus already delivered disproportionate returns once during the 2019–2022 cycle, when PAT surged from ₹94 Cr to ₹984 Cr. That was followed by a downcycle, but the next upcycle clearly started from FY24 onwards.

PAT in FY24 stood at ₹162 Cr, and it reached ₹890 Cr by FY26. The stock has already turned into a multi-bagger again during this phase, and arguably, the journey is still far from over.

The real exercise, therefore, is simple but not easy: Identify companies currently in the ₹100–300 Cr PAT range and assess which among them have the management quality, scalability, balance sheet strength, and sectoral tailwinds to compound into a four-digit PAT business.

The hard truth is that nearly 80% of such companies may never get there, which is why this game is never easy. But the formula remains valid, and repeatedly proven.

But your real work begins with filtering those 250+ companies.

Good luck, India!

Letter to our investors (June 2026)

1) Dark clouds over Indian economy are clearing

2) Next 12 months could see a good rally

3) Macros, stocks, gold - how are you positioned?

https://t.co/r40fwH3QGa

Very good summery of Marksans Pharma . With new acquisition and overall outlook it is expected to give good growth with geographical diversification across developed markets which may give good margins

Marksans Pharma Ltd.📞 Q4 & FY26 Concall Summary #MARKSANS

🟡 MANAGEMENT PROJECTION :

Management remains highly confident about sustaining long-term growth and reiterated its target of reaching 4,000 crores revenue within the next 2 years while maintaining a broader roadmap to double revenues over the next 3-5 years. FY27 revenue growth guidance remains conservatively at 15-20% with EBITDA margins expected to sustain around 20-21% despite near-term raw-material inflation. North America continues to remain the biggest growth engine with around 50 new product launches planned during FY27, while the UK pipeline remains extremely strong with over 200 product filings planned over the next 4 years. Europe and Canada are expected to become important incremental growth contributors from H2 FY27 onward. The Teva facility still operates at only around 50% utilization, leaving meaningful room for 40-50% additional growth from existing infrastructure itself. Australia is also expected to scale toward the management’s long-term target of 100 million dollars revenue within the next 3 years.

🔴 Red Alert :

Management acknowledged rising pressure from geopolitical tensions, petroleum-linked raw-material inflation, and logistics costs. APIs, solvents, intermediates, freight, and fuel-related inputs have already seen 20-25% price increases due to the ongoing Middle East conflict and supply-chain disruptions. Although the company currently has sufficient inventory coverage for Q1 and partially Q2, prolonged geopolitical disruptions could eventually pressure margins and require customer renegotiations. The US market also continues facing structural pricing pressure due to intense generic competition. Working capital increased meaningfully because the company deliberately built higher inventory during tariff and geopolitical uncertainty, increasing cash absorption temporarily. Additionally, Europe and Canada expansion remains at an early stage with product approvals still pending, meaning execution timelines remain uncertain.

🟢 Green Alert :

Marksans delivered another record-breaking year with FY26 revenue crossing 3,000 crores for the first time while EBITDA reached 601 crores and PAT touched 420 crores. Q4 FY26 was exceptionally strong with revenue growing 20.8% YoY to 856 crores while EBITDA surged 54% to 195 crores and PAT rose 64% to 149 crores. EBITDA margins expanded sharply to 22.8% in Q4 driven by better product mix, operating leverage, and improved execution. The biggest operational strength remains the rapid scaling of the North America business, which has grown from 635 crores to 1,533 crores over the last 4 years. Australia also emerged as a major growth driver with Q4 revenue surging 61% YoY supported by expansion into branded prescription generics through Nova Pharma. Importantly, the company continues operating debt-free with nearly 990 crores cash and free cash flow generation of 328 crores during FY26.

🔵 Blue Alert :

Marksans is steadily transforming from a largely OTC-focused generics company into a diversified global regulated-market pharmaceutical platform spanning OTC, prescription generics, branded generics, multiple dosage forms, Europe expansion, Canada entry, Australia prescription business, and strategic international acquisitions. Management is aggressively diversifying geographically to reduce dependence on any single market while simultaneously broadening the product portfolio beyond traditional OTC categories. Europe and Canada are becoming the next major strategic expansion zones while Australia is evolving into a deeper branded generics platform. The company is also continuously strengthening R&D capabilities with annual R&D spending maintained near 3% of revenue and large product filing pipelines across geographies.

🧠 Deep Insight :

The most important structural strength at Marksans is the company’s disciplined and diversified global growth model. Unlike many pharma companies that remain heavily concentrated in one geography or therapy area, Marksans has steadily built multiple regulated-market growth engines simultaneously across the US, UK, Europe, Australia, and now Canada. This diversification significantly improves business resilience and reduces dependence on any single pricing cycle or regulatory environment. More importantly, the Teva facility acquisition appears increasingly strategic because the company still has massive unused capacity while already seeing strong operating leverage benefits from integration and new product launches. The combination of 50-55% overall utilization, debt-free balance sheet, 990 crore cash reserves, and strong free cash flow generation gives Marksans unusually high optionality for both organic expansion and acquisitions. Europe could become especially important over the next 3-5 years because management repeatedly emphasized better pricing environments compared to the highly competitive US market. If Marksans successfully scales Europe and Canada while continuing strong US execution and disciplined capital allocation, the company could potentially evolve into a significantly larger multi-geography regulated-market pharma platform over the next decade.

@SahilDigwa73522 They have EPC business and also they have some businesses wherein they act like an IPP where in after the business matures they sell to the investors as such they have to maintain subsidiaries

Oriana Power: Results take

1. Strong Growth, But Not Quite as Explosive at the Bottom Line

The company delivered a solid FY26: revenue jumped ~84% YoY to ₹1,813.67 cr, while PAT grew a healthy (but slower) ~59% to ₹252.34 cr. Top-line momentum looks impressive, but the PAT growth lag hints at some cost or margin headwinds kicking in.

2. Margins Stayed Healthy Despite a Small Dip

PAT margin cooled from 16.1% in FY25 to ~13.9% in FY26, and PBT margin slipped from ~21.5% to ~19.1%.

Nothing alarming for an EPC-heavy renewables play the levels are still respectable—but it’s worth keeping an eye on whether input costs or execution pressures keep nibbling away.

3. Business Still Very Much EPC-Driven Almost the entire revenue pie (₹1,780.61 cr) came from EPC work. The RESCO segment (rooftop/own-asset solar) was a tiny ₹33.07 cr and remained loss-making. Diversification beyond pure EPC is clearly still in early days.

4. Cash Conversion Is a Real Highlight Operating cash flow reportedly hit ~₹337 cr, giving a CFO/PAT ratio above 1.3x. That’s strong working-capital management and a big comfort factor—cash is actually flowing in faster than accounting profits, which is always investor-friendly.

5. Two Sides of the Same Coin: Complexity Risk + BESS Optionality

On the risk side, the group’s structure is quite complex—74 subsidiaries, SPV investments, and corporate guarantees—so balance-sheet hygiene and hidden liabilities need ongoing monitoring.

On the upside, BESS (battery energy storage) is the big growth lever: they’ve already secured 403 MWh in FY25 and are targeting 1+ GWh by FY26. Success here hinges on execution speed, battery sourcing, warranty reliability, and whether project IRRs actually stack up. Get this right and it could be a game-changer.

Google which is cash surplus, just announced an additional capital raise of $80 bn.

Google annual profit is $160 bn, last quarter $62 bn, and market cap $4.5 trillion. That is close to total profits and market cap of all Indian listed companies put together.

It’s a wake up call to all companies to invest into the future, whatever the present maybe.

Now that IPL is done and dusted, time for India to focus on business of business.

Oriana Power: Results take

1. Strong Growth, But Not Quite as Explosive at the Bottom Line

The company delivered a solid FY26: revenue jumped ~84% YoY to ₹1,813.67 cr, while PAT grew a healthy (but slower) ~59% to ₹252.34 cr. Top-line momentum looks impressive, but the PAT growth lag hints at some cost or margin headwinds kicking in.

2. Margins Stayed Healthy Despite a Small Dip

PAT margin cooled from 16.1% in FY25 to ~13.9% in FY26, and PBT margin slipped from ~21.5% to ~19.1%.

Nothing alarming for an EPC-heavy renewables play the levels are still respectable—but it’s worth keeping an eye on whether input costs or execution pressures keep nibbling away.

3. Business Still Very Much EPC-Driven Almost the entire revenue pie (₹1,780.61 cr) came from EPC work. The RESCO segment (rooftop/own-asset solar) was a tiny ₹33.07 cr and remained loss-making. Diversification beyond pure EPC is clearly still in early days.

4. Cash Conversion Is a Real Highlight Operating cash flow reportedly hit ~₹337 cr, giving a CFO/PAT ratio above 1.3x. That’s strong working-capital management and a big comfort factor—cash is actually flowing in faster than accounting profits, which is always investor-friendly.

5. Two Sides of the Same Coin: Complexity Risk + BESS Optionality

On the risk side, the group’s structure is quite complex—74 subsidiaries, SPV investments, and corporate guarantees—so balance-sheet hygiene and hidden liabilities need ongoing monitoring.

On the upside, BESS (battery energy storage) is the big growth lever: they’ve already secured 403 MWh in FY25 and are targeting 1+ GWh by FY26. Success here hinges on execution speed, battery sourcing, warranty reliability, and whether project IRRs actually stack up. Get this right and it could be a game-changer.

Timepass talk on Sunday

1. OBSC Perfection – Precision with a diversification kicker

OBSC is a ~9-year-old precision metal component manufacturer with a diversified portfolio of high-quality products. Its key offerings include piston rods, sensor bosses, water injectors, and nut fasteners, catering to applications across exhaust systems, steering & suspension, ammunition, fuses, mechanical cables, and telecom towers.

The company operates six manufacturing facilities across Maharashtra, Tamil Nadu, and Haryana, with capabilities spanning machining, turning, investment casting, fabrication, stamping, and forging.

Revenue mix: ~80% domestic, ~20% exports

Order Book: ₹1,200+ crore, with a portion of these orders scheduled for execution over the next 4–5 years.

Fund Raise: The company raised ₹53 crore through a preferential issue at ₹311 per share, aimed at supporting its growth and expansion plans.

Despite being an SME, OBSCP has been consistent with disclosures, reporting strong Q3 performance with record-high total income, EBITDA, and PAT.

FY25 total income: ₹145 crore

9M FY26 total income: ₹151 crore (already surpassing FY25)

Segment mix (9M FY26):

Automotive – 84% (vs ~91% in FY25)

Marine – 6.7%

Defence – 5.7%

What’s changing?

The key thesis lies in gradual diversification away from automotive toward marine and defence, which are structurally higher-margin segments.

Automotive gross margins: ~20–25%

Defence gross margins: ~40–45%

Marine gross margins: can exceed 70%

Moving up the value chain

Some of the recently secured orders require the company to set up dedicated facilities in close proximity to customers. While it may take a few quarters for these nomination letters to translate into revenue, they provide strong visibility into FY28 and beyond.

Bottom line

While the valuations aren't necessarily cheap and business remains auto-heavy and hence cyclical, increasing exposure to defence and marine could meaningfully improve the margin profile and earnings quality over time. If this mix shift sustains, the business could transition from a cyclical auto supplier to a more diversified, higher-margin play.

2. The triple digit threat

Greg Sharenow, a commodities expert from PIMCO, suggests that even if the Strait reopens in early May, crude prices are likely to stay in the triple digits for a considerable time. A return to the $70/bbl range is likely more than a year away.

He says, reopening isn't just about ending the blockade; it involves complex transit mechanisms, clearing trapped tankers, and managing a "virtual pipeline" that has been disrupted for nearly two months.

If full normalization occurs by the end of May, prices could return to the $80s, however, if flows are restricted to 80% of normal, global demand (which would be short 3–4 million barrels per day) would keep prices much higher.

Refined products (jet fuel, diesel) are trading at historic premiums to crude. Asia has been the most acutely impacted region due to damaged refinery infrastructure in Kuwait, Bahrain, and ongoing attacks on Russian assets.

In some markets, while Brent Crude is trading at $105.00 per barrel, the market is seeing massive spreads with Jet Fuel priced at $157.10 (a $52.10 premium) and Diesel at $164.60 (a $59.60 premium).

3. Price Hikes and Early Signs of Demand Softening

These elevated refining spreads and fuel costs are beginning to translate into airfare increases, with early signs of demand softening in price-sensitive segments.

Airlines are responding through a mix of fuel surcharges, fare hikes, and selective capacity adjustments. According to aviation analytics firm Cirium, capacity discipline is increasing, though this is not a uniform, industry-wide reduction.

Some supply-side concerns have also emerged. While localized tightness in jet fuel availability has been reported in parts of Europe, claims of critically low continent-wide reserves should be treated with caution, as inventories and logistics vary significantly by region and airport.

On the diesel front, demand destruction is more visible in weaker economies such as Pakistan, Bangladesh, and Nigeria, where limited fiscal capacity restricts fuel subsidies, leading to sharp consumption adjustments.

The Philippines did declare a temporary energy emergency amid global supply disruptions. Retail diesel prices reportedly spiked significantly (in some cases from ~₱60/litre to peak levels near ₱170 before easing to ~₱100–105), still materially higher than historical norms, highlighting the stress on consumers.

Airlines have already started passing on costs:

Air India has added fuel surcharges on select international routes

Cathay Pacific has increased surcharges across its network

Global carriers like Emirates, Lufthansa, and KLM have also adjusted fares and fees

From a cost perspective, Scott Kirby of United Airlines has indicated that sustained high fuel prices could add billions of dollars annually to airline cost structures.

This additional cost is more than profits of some of the airlines!

On the demand side, premium and business travel remains relatively resilient, but leisure travel is beginning to show elasticity, with some routes witnessing sharp fare increases leading to deferred or downsized travel plans.

4. Vedanta - Value unlocking or trap?

The long-awaited demerger is finally here. Vedanta Ltd has announced May 1, 2026 as the record date for its restructuring, which will lead to the creation and eventual independent listing of five separate entities.

For every 1 share of Vedanta Ltd held on the record date, shareholders will receive 1 share in each of the four newly created entities.

The five resulting companies:

Vedanta Ltd (retains stake in Hindustan Zinc)

Vedanta Aluminium (includes ~51% stake in Bharat Aluminium Company)

Vedanta Power

Vedanta Oil & Gas

Vedanta Steel & Iron Ore

Key highlights

Vedanta Aluminium stands out as the most compelling play, supported by tight global aluminium supply, firm metal prices, and ongoing capacity expansions.

Vedanta Oil & Gas will house Cairn Oil & Gas, India’s largest private crude oil producer, contributing ~25% of domestic output. With crude hovering around $90/bbl, the business offers strong near-term margin potential.

Indicative valuation (as per Nuvama):

Vedanta Aluminium – ₹449

Vedanta Ltd – ₹291

Vedanta Power – ₹45

Vedanta Oil & Gas – ₹40

Vedanta Steel & Iron Ore – ₹22

Post-demerger, once the new entities are listed, there could be meaningful selling pressure in select businesses (some of that selling happened last week).

5. Himadri Speciality Chemical – Something meaningful is unfolding

Himadri Speciality Chemical Ltd (HSCL) has delivered a 20%+ margin year after a six-year gap, potentially signaling the start of a structurally stronger earnings phase.

Management has guided for net profit exceeding ₹1,100 crore by FY28, driven by a decisive shift toward value-added products. These currently contribute ~25–30% of revenue, with a target to scale this to ~50% over the next few years.

While the financial trajectory is important, the bigger story lies in how effectively the company is scaling multiple high-potential verticals simultaneously.

Key Growth Drivers

Anode Materials: HSCL has commissioned a ~200 MTPA vertically integrated anode capacity, positioning itself in a high-growth EV ecosystem segment. Management has indicated that this is just the starting point, with significant capex planned over the next 4–5 years.

Cathode Materials: The company is setting up India’s first commercial-scale LFP (Lithium Iron Phosphate) cathode active material plant in Odisha, expected to be operational by Q3 FY27, a strategic forward integration into battery materials.

Carbon Black Expansion: A new carbon black line is being added, strengthening both core and specialty segments, supporting margin improvement.

Birla Tyres Integration: With Birla Tyres, the company is ramping up capacity and introducing new products. From a revenue base of ~₹187 crore in FY26, management is targeting ₹3,000+ crore over the next 3–4 years!

Anthraquinone & Carbazole: They are setting up a facility (target completion by Q2 FY27) to manufacture these specialty chemicals. These are high-margin derivatives used in dyes, pigments, and high-performance plastics. By producing these in-house, they capture the margin that was previously going to their downstream customers

Strategic Investment: Equity stake in International Battery Company (IBC) could evolve into a meaningful long-term optionality. Instead of just making cathode/anode powders and hoping they work, HSCL uses IBC’s South Korean facility to validate and scale their materials in real-world battery cells.

Bottom line

Margins have expanded from ~10% in FY23 to ~21% in FY26, while value-added products (VAP) have scaled from near-zero a few years ago to ~25% today, with a target of ~50% over the next few years.

HSCL is not just improving earnings, it is strategically repositioning itself across the EV materials and specialty chemicals value chain. That said, some of these verticals remain inherently cyclical, and valuations should be assessed with that cyclicality in mind.

That's all for this edition. Have a great Sunday!

Disclaimer: None or buy or sell recommendations. This publicly available information is shared for learning and education purposes.

@LearningEleven It is really a good read on every sunday morning. Thanks for sharing wonderful thoughts and sharing with fellow investors . All the best and keep sharing

Timepass talk on Sunday

1. OBSC Perfection – Precision with a diversification kicker

OBSC is a ~9-year-old precision metal component manufacturer with a diversified portfolio of high-quality products. Its key offerings include piston rods, sensor bosses, water injectors, and nut fasteners, catering to applications across exhaust systems, steering & suspension, ammunition, fuses, mechanical cables, and telecom towers.

The company operates six manufacturing facilities across Maharashtra, Tamil Nadu, and Haryana, with capabilities spanning machining, turning, investment casting, fabrication, stamping, and forging.

Revenue mix: ~80% domestic, ~20% exports

Order Book: ₹1,200+ crore, with a portion of these orders scheduled for execution over the next 4–5 years.

Fund Raise: The company raised ₹53 crore through a preferential issue at ₹311 per share, aimed at supporting its growth and expansion plans.

Despite being an SME, OBSCP has been consistent with disclosures, reporting strong Q3 performance with record-high total income, EBITDA, and PAT.

FY25 total income: ₹145 crore

9M FY26 total income: ₹151 crore (already surpassing FY25)

Segment mix (9M FY26):

Automotive – 84% (vs ~91% in FY25)

Marine – 6.7%

Defence – 5.7%

What’s changing?

The key thesis lies in gradual diversification away from automotive toward marine and defence, which are structurally higher-margin segments.

Automotive gross margins: ~20–25%

Defence gross margins: ~40–45%

Marine gross margins: can exceed 70%

Moving up the value chain

Some of the recently secured orders require the company to set up dedicated facilities in close proximity to customers. While it may take a few quarters for these nomination letters to translate into revenue, they provide strong visibility into FY28 and beyond.

Bottom line

While the valuations aren't necessarily cheap and business remains auto-heavy and hence cyclical, increasing exposure to defence and marine could meaningfully improve the margin profile and earnings quality over time. If this mix shift sustains, the business could transition from a cyclical auto supplier to a more diversified, higher-margin play.

2. The triple digit threat

Greg Sharenow, a commodities expert from PIMCO, suggests that even if the Strait reopens in early May, crude prices are likely to stay in the triple digits for a considerable time. A return to the $70/bbl range is likely more than a year away.

He says, reopening isn't just about ending the blockade; it involves complex transit mechanisms, clearing trapped tankers, and managing a "virtual pipeline" that has been disrupted for nearly two months.

If full normalization occurs by the end of May, prices could return to the $80s, however, if flows are restricted to 80% of normal, global demand (which would be short 3–4 million barrels per day) would keep prices much higher.

Refined products (jet fuel, diesel) are trading at historic premiums to crude. Asia has been the most acutely impacted region due to damaged refinery infrastructure in Kuwait, Bahrain, and ongoing attacks on Russian assets.

In some markets, while Brent Crude is trading at $105.00 per barrel, the market is seeing massive spreads with Jet Fuel priced at $157.10 (a $52.10 premium) and Diesel at $164.60 (a $59.60 premium).

3. Price Hikes and Early Signs of Demand Softening

These elevated refining spreads and fuel costs are beginning to translate into airfare increases, with early signs of demand softening in price-sensitive segments.

Airlines are responding through a mix of fuel surcharges, fare hikes, and selective capacity adjustments. According to aviation analytics firm Cirium, capacity discipline is increasing, though this is not a uniform, industry-wide reduction.

Some supply-side concerns have also emerged. While localized tightness in jet fuel availability has been reported in parts of Europe, claims of critically low continent-wide reserves should be treated with caution, as inventories and logistics vary significantly by region and airport.

On the diesel front, demand destruction is more visible in weaker economies such as Pakistan, Bangladesh, and Nigeria, where limited fiscal capacity restricts fuel subsidies, leading to sharp consumption adjustments.

The Philippines did declare a temporary energy emergency amid global supply disruptions. Retail diesel prices reportedly spiked significantly (in some cases from ~₱60/litre to peak levels near ₱170 before easing to ~₱100–105), still materially higher than historical norms, highlighting the stress on consumers.

Airlines have already started passing on costs:

Air India has added fuel surcharges on select international routes

Cathay Pacific has increased surcharges across its network

Global carriers like Emirates, Lufthansa, and KLM have also adjusted fares and fees

From a cost perspective, Scott Kirby of United Airlines has indicated that sustained high fuel prices could add billions of dollars annually to airline cost structures.

This additional cost is more than profits of some of the airlines!

On the demand side, premium and business travel remains relatively resilient, but leisure travel is beginning to show elasticity, with some routes witnessing sharp fare increases leading to deferred or downsized travel plans.

4. Vedanta - Value unlocking or trap?

The long-awaited demerger is finally here. Vedanta Ltd has announced May 1, 2026 as the record date for its restructuring, which will lead to the creation and eventual independent listing of five separate entities.

For every 1 share of Vedanta Ltd held on the record date, shareholders will receive 1 share in each of the four newly created entities.

The five resulting companies:

Vedanta Ltd (retains stake in Hindustan Zinc)

Vedanta Aluminium (includes ~51% stake in Bharat Aluminium Company)

Vedanta Power

Vedanta Oil & Gas

Vedanta Steel & Iron Ore

Key highlights

Vedanta Aluminium stands out as the most compelling play, supported by tight global aluminium supply, firm metal prices, and ongoing capacity expansions.

Vedanta Oil & Gas will house Cairn Oil & Gas, India’s largest private crude oil producer, contributing ~25% of domestic output. With crude hovering around $90/bbl, the business offers strong near-term margin potential.

Indicative valuation (as per Nuvama):

Vedanta Aluminium – ₹449

Vedanta Ltd – ₹291

Vedanta Power – ₹45

Vedanta Oil & Gas – ₹40

Vedanta Steel & Iron Ore – ₹22

Post-demerger, once the new entities are listed, there could be meaningful selling pressure in select businesses (some of that selling happened last week).

5. Himadri Speciality Chemical – Something meaningful is unfolding

Himadri Speciality Chemical Ltd (HSCL) has delivered a 20%+ margin year after a six-year gap, potentially signaling the start of a structurally stronger earnings phase.

Management has guided for net profit exceeding ₹1,100 crore by FY28, driven by a decisive shift toward value-added products. These currently contribute ~25–30% of revenue, with a target to scale this to ~50% over the next few years.

While the financial trajectory is important, the bigger story lies in how effectively the company is scaling multiple high-potential verticals simultaneously.

Key Growth Drivers

Anode Materials: HSCL has commissioned a ~200 MTPA vertically integrated anode capacity, positioning itself in a high-growth EV ecosystem segment. Management has indicated that this is just the starting point, with significant capex planned over the next 4–5 years.

Cathode Materials: The company is setting up India’s first commercial-scale LFP (Lithium Iron Phosphate) cathode active material plant in Odisha, expected to be operational by Q3 FY27, a strategic forward integration into battery materials.

Carbon Black Expansion: A new carbon black line is being added, strengthening both core and specialty segments, supporting margin improvement.

Birla Tyres Integration: With Birla Tyres, the company is ramping up capacity and introducing new products. From a revenue base of ~₹187 crore in FY26, management is targeting ₹3,000+ crore over the next 3–4 years!

Anthraquinone & Carbazole: They are setting up a facility (target completion by Q2 FY27) to manufacture these specialty chemicals. These are high-margin derivatives used in dyes, pigments, and high-performance plastics. By producing these in-house, they capture the margin that was previously going to their downstream customers

Strategic Investment: Equity stake in International Battery Company (IBC) could evolve into a meaningful long-term optionality. Instead of just making cathode/anode powders and hoping they work, HSCL uses IBC’s South Korean facility to validate and scale their materials in real-world battery cells.

Bottom line

Margins have expanded from ~10% in FY23 to ~21% in FY26, while value-added products (VAP) have scaled from near-zero a few years ago to ~25% today, with a target of ~50% over the next few years.

HSCL is not just improving earnings, it is strategically repositioning itself across the EV materials and specialty chemicals value chain. That said, some of these verticals remain inherently cyclical, and valuations should be assessed with that cyclicality in mind.

That's all for this edition. Have a great Sunday!

Disclaimer: None or buy or sell recommendations. This publicly available information is shared for learning and education purposes.

Some of the recent under appreciated milestones in India

1. Digital payments : UPI in march - 22 billion transactions with $310 Billion value.

2. Changing Energy landscape :Solar rooftop installations per month in March crossed 2 lac (13x in 2 years)

10 GW and 33 lakh households

3. Semiconductor : from zero to 4 commecial plants in 2 years.. semicon 2.0 coming.

4. Datacentre- capacity to quadruple to 10GW in 4 years with $200 Bn + investment.

5. Ultratech crossed 200 MT capacity ( highest in world outside China).

6. Nuclear energy : India's nuclear energy sector reached a landmark milestone on April 6, 2026, when the 500 MWe Prototype Fast Breeder Reactor (PFBR) attained criticality.

Dont let short term noise impact you !!

Timepass talk on Sunday

1. Marine Electricals (India) Limited

From Jan’26 till date, the company has secured ~₹595 Cr of orders (ex-tax). While the bulk continues to come from its core power distribution systems business, it is encouraging to see incremental orders from data centres and semiconductor facilities, indicating early diversification. Most of these orders are to be executed within ~12 months, providing near-term revenue visibility.

Already a silent proxy to naval spending, Marine is also building optional growth drivers such as EV charging solutions, though these are still at a nascent stage.

On the defence side, the company already has capabilities in shock-graded motors and electrical systems, designed to withstand extreme naval conditions (including underwater shocks), creating high entry barriers and sticky relationships. That said, naval revenues have historically been lumpy, given long project cycles and execution timelines.

Importantly, the Indian Navy plans to scale its fleet to 150–160 ships by 2030, 200+ by 2035, and ~230 by 2037, reflecting a clear long-term expansion roadmap. With multiple vessels under parallel construction, this could translate into a more consistent order pipeline for established players like Marine Electricals over the coming years.

Only drawback: Marine Electricals Limited doesn’t conduct concalls, making it relatively difficult for investors to track developments and management commentary.

2. The $58 Billion Reconstruction: Mapping India’s Role in the Gulf’s Recovery

While the Iran war keeps playing hide-and-seek with ceasefire, at some stage in the next few months, the focus would shift from defense to repairing and reconstructing a shattered energy map in gulf nations.

According to Rystad Energy, the region is saddled with up to $58 billion in repair costs, with a staggering $50 billion concentrated in the oil and gas vertical alone.

The damage is both deep and wide:

Energy Hubs: Major outages at Saudi and Kuwaiti refineries, Qatar’s LNG terminals, and the UAE’s petrochemical complexes.

Civil Lifeblood: Widespread damage to desalination units in Kuwait and UAE, alongside grid failure in Bahrain.

This isn't just a "repair job"; it’s a multi-year technical overhaul. As the initial assessments conclude, do expect a wave of Order Book announcements. Here is the Indian contingent positioned for the "First Responder" phase:

i. The Grid & Structural Giants

L&T, KEC International, and Kalpataru Projects could be the front-runners for HVDC line restoration and substation rebuilding. With Kalpataru now owning 100% of its Saudi subsidiary, their "local" status is a significant margin moat.

ii. The Fluid Dynamics & Pipe Specialists

Welspun Corp (via East Pipes) and Jindal Saw will likely dominate the bulk pipeline replacement. However, for the high-end, corrosive-resistant alloy pipes inside the refineries, keep an eye on Ratnamani Metals. And Omnitech Engineering would have a role to play as well thru their customers.

iii. Water & Specialized Engineering

VA Tech Wabag is the natural beneficiary for the desalination crisis, but don't overlook DEE Development Engineers. Their modular piping systems are the "fast-track" solution for replacing damaged refinery sections without the lead time of traditional on-site fabrication.

Disclaimer: This are my assumptions and there is no guarantee that these players will get the orders.

3. Garware Hi Tech Films

With India resuming trade deal discussions with US, sentiment for Garware Hi-Tech Films could turn positive. Just last week, the company introduced three new product lines, Graphic Films, Cloaking Films, and PDLC Smart Films.

The strategic shift is quite evident: Garware is moving beyond automotive sun control films toward architectural, smart materials, and specialty films, signaling a clear evolution in its product portfolio.

Graphic films → volume game, lower moat (Use cases: vehicle wraps, signage, retail branding)

Cloaking films → niche, steady (Use cases: defence, corporate offices, banks, data centres)

PDLC → high-growth, premium, future driver (Use cases: smart glass, offices, hospitals, luxury homes, automotive sunroofs)

Combined India opportunity could be ~₹4,000–6,000 Cr across segments, with the global market being significantly larger.

Among these, PDLC (Polymer Dispersed Liquid Crystal) stands out as the most promising segment. It is growing at ~15–20% CAGR globally, is rapidly gaining traction in India, and remains heavily import-dependent (China, Korea). In many ways, this is shaping up to be a premium consumption + import substitution play.

4. The Non-Linear Reality - Nuclear, Defence and Aerospace

There’s been a lot of excitement lately around the Nuclear and Defence themes, Apollo Micro Systems getting a lifetime license, MTAR Technologies management highlighting nuclear opportunities in multiple interviews, Zen Technologies securing an arms manufacturing licence, and KSB Limited building a massive nuclear order book.

And it’s not just Nuclear and Defence, Aerospace component manufacturing is also a multi-year theme that could reward investors well over the next 5–10 years.

But here’s the catch: investing in these sectors requires a fundamental shift in mindset.

Unlike consumer businesses or banks, where growth shows up in quarterly or annual increments, these industries operate on “deep-tech timelines.” The journey from order win to meaningful revenue is rarely linear. What feels like a “long wait” in retail (2–3 years) can easily stretch to 10–15 years in Aerospace or Nuclear.

That’s why chasing these stocks at any price can backfire.

Take Sansera Engineering, yes Aerospace-Defence-Space (ADS) segment is growing fast, but the stock is already trading at ~30x FY28 earnings.

Or look at Dynamatic Technologies, the stock nearly doubled on Airbus-related orders couple of years ago, then spent ~18 months consolidating before the next leg up. MTAR Technologies spent almost 22 months consolidating before finally crossing its Sep ’23 highs.

The takeaway is simple: if you want to play these themes, align your expectations. You will see lot of valleys and long consolidation periods

Treat them differently. Ideally, allocate them to a separate bucket, or even a separate demat account, so they don’t compete with your core portfolio on near-term returns.

These are long-duration bets. They reward patience, not urgency.

5. Sigma Advanced System - The new kid on block

The first “Initiating Coverage” report on any stock is always a meaningful milestone. It signals rising institutional interest and often improves liquidity.

For instance, JM Financial recently saw its first initiating coverage in many years from DAM Capital.

On similar lines, yesterday, Midas Equities and Research has initiated coverage on Sigma Advanced Systems, a relatively new entrant in the Defence and Aerospace ancillary space.

We recently saw the kind of attention Belrise Industries received after acquiring Chester Hall (UK) and SDM (Europe) in the Aerospace segment. That said, Belrise is a far more established and proven player, so this is not a like-to-like comparison.

Here’s a quick snapshot (shared with my Subscribers on April 11):

If we set aside the legacy overhang of erstwhile Megasoft, Sigma Advanced, at its core, started as a Defence Electronics & Avionics company, before embarking on an aggressive acquisition-led expansion:

Acquired a significant stake in Indrajaal, an Autonomous Systems & Counter-Drone specialist (notably deployed at Western Command during Operation Sindoor).

Acquired 100% of UK-based Nasmyth Group, a global precision engineering company focused on Aerospace (~₹750 Cr annual revenue)

Further added a 51% stake in AS Strategic Pvt. Ltd., which claims partnerships and JVs with global OEMs as well as domestic defence players

Clearly, Sigma Advanced Systems is attempting to scale rapidly, and perhaps biting off a lot in the process. But if execution holds, this could evolve into a meaningful winner over time.

Think about the positioning: Defence electronics, Autonomous Systems & Counter-drone, and Aerospace precision engineering, all sunrise themes converging into one platform.

Execution will be the key. The opportunity is evident, but as always, time will be the ultimate judge.

That's all for this edition. Have a great Sunday!

Disclaimer: None or buy or sell recommendations. This publicly available information is shared for learning and education purposes.

#PNGSGargiFashion : IPO at ₹30 → ₹1,517 Peak: The PNGS Gargi Story Nobody Is Talking About | SME Outlier Series

https://t.co/H9H4s1e7QK

In this deep-dive from Minerva Capital Research Solutions, our equity research team member @LawofInvesting breaks down the story of a tiny consultancy to a ₹126 Cr fashion jewellery powerhouse

What's Inside:

✅ How Gargi leveraged 193 years of P.N. Gadgil & Sons brand trust — at ZERO royalty cost

✅ The asset-light franchise model generating 30%+ EBITDA margins

✅ The diamond jewellery launch that changed everything

✅ The FOCO → FOFO model shift & its impact on revenue and margins

✅ Why RPT sales hit 88% of revenue in FY25 — and what it means

✅ Management guidance: ₹200 Cr revenue target by FY28

✅ Key risks every investor must know before investing

⚠️ This video is for educational purposes only. Please consult your financial advisor before making any investment decisions. Research by: Minerva Capital Research Solutions | SEBI Registered RA: INH000018896

#PNGSGargi #GargiJewellery #SMEStocks #BSESMEIPOs #SmallCapStocks #JewelleryStocks #StockMarketIndia #MultibaggerStocks #minervacapitalresearchsolutions