🚨 JMP alert

Worried about the exogeneity of a macro structural shock with respect to omitted variables?

⚠️Testing the correlation between past of omitted variables and present of shocks might mislead conclusions.

↪️ Add a correction term!

🧵 #EconTwitter#EconJobMarket

1/11

Amedeo Andriollo's (@amedandr) JMP proposes a test for exogeneity of macroeconomic structural shocks, robust to omitted variable dynamics. Do shocks to uncertainty about economic policy leads to higher/lower future inflation? To find out: https://t.co/wfwNUiu297

#EconJobMarket

What have been the underlying drivers of a potential "replication crisis" in corporate bond asset pricing research over the last decade?

Our updated working paper, https://t.co/t7nskM5U7C, documents some root causes:

(1) Not adjusting signals for potential microstructure noise (bonds trade OTC)

(2) Ex-post trimming/winsorization of t+1 (future) bond returns (i.e., kicking out data that destroys strategy profitability ex-post)

The entirety of our paper can be replicated with our open-source data on https://t.co/oL4uiT0ffz, the WRDS Bond database, and the accompanying portfolio/factor construction software package PyBondLab (https://t.co/eIlLzlMxbH).

The PyBondLab package also contains brand new functionality for:

- Computing portfolio turnover

- Implementing various cost mitigation methods: staggered holding periods and buy-hold spreads (see Novy-Marx & Velikov, 2016)

Check out our new Python package developed with @dickerson_phd -- great working with him! Have a look at https://t.co/Kc7adyWZ8N or see the GitHub repo https://t.co/J1upKmq90H. More info: https://t.co/zGRfz6hGqp. Any feedback is more than welcome!

Excited to announce PyBondLab, a new Python package co-developed with my talented co-author @Gi_R94 . Try it out directly in Python: https://t.co/eIlLzlMxbH

Detailed examples available on the GitHub repo here: https://t.co/Rh3pmYbRA4

The software (properly) handles corporate bond data uncertainty. It generates bond data samples with ex-ante filters to avoid look-ahead bias and subsequently generates potentially hundreds of bond factors/portfolios based on any underlying signal.

Additional information and an example applied to non-investment grade bond momentum can be found on the https://t.co/rPm0nFejot website.

Look-ahead bias from ex-post filtering has played havoc in the bond literature … hopefully this package addresses this.

Many more corporate bond code and data initiatives to be announced this week! 😊 All hosted on https://t.co/VLRgkC2Hta

👉🏼 CALL for papers!

The 4th SASCA PhD Conference in #Economics 2024 will take place in #Venice (Sept 23-24). Submissions in any field in Economics & Finance are welcome by June 15th. Check out the keynote speakers:

https://t.co/xkyZWodLOT

@CaFoscari@unissTweet@DipEcoUnive

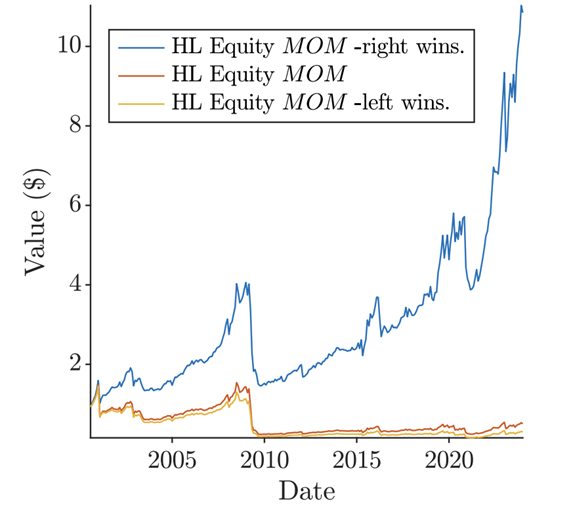

It is well-known that equity momentum has disappeared over the last 2-decades. Want to revive it? No problem. Just asymmetrically (ex post) winsorize/trim returns at the 99.50th percentile (right-tail) of the return distribution… (data mine) 😉, i.e., kick-out the "winners" that end up in the short-leg of the portfolio sort (works great for corporate bonds too).

(2) We have several follow-up papers including research on microstructure bias in corporate bond asset pricing (https://t.co/WNcacSd4fm with @Gi_R94) and where we estimate over 500 trillion possible models in a Bayesian framework (https://t.co/36Mn8LxFwX with @Chris_Julliard )

(1) I recently wrote a paper exploring asset pricing in corporate bonds with Cesare Robotti and Philippe Mueller.

It has been published in the @J_Fin_Economics and was made the Editor’s Choice for November 2023.

The published article is available here: https://t.co/9JYtEQfqUr

@andrepaltry Spiegazione di contango e discussione su nat gas .. mancavano solo i futures sul succo di arancia ed era un tuffo nel passato a TOMA 2016 a uniud 😂

Thread on "In Search of the Origins of Financial Fluctuations" by @xgabaix and @rkoijen. One of the most exciting agendas in asset pricing. See video (https://t.co/2ZuSPWi4f3). They estimate $1b investment in market -> $10b increase in price. How? 1/

@b0rk@holtbt also gave a tutorial first on how to create container from scratch before introducing docker and it was really amazing like how this tweet demystify that container isn't that scary blackbox . https://t.co/Ox1m2sfOe7

My lunch breaks recently have been in the company of Yaser Abu Mostafa's "learning from data" lectures. What an amazing teacher. Ht @economeager

https://t.co/Ij6lKW02e2

Prima o poi doveva arrivare questo giorno. E’ stato un percorso lungo, ma ho preso la mia decisione. E mentre aspetto che mi chiamino, seduto nello spogliatoio, la mente corre a quando tutto è iniziato. A quel “soldo di cacio” che crebbe mangiando gnocchi, lasagne e salsicce”.