This is a *way* bigger deal than it seems...

Frontier AI companies will *never* own the frontier again

I kid you not... I've been waiting for someone to show this result for like 4 years... this is a huge deal.

The short reason: combinations of models will *always* outperform individual models

The long reason: this is the gateway to a million times more data... and huge leaps in compute efficiency.

The AI scaling laws always win.

More in article below 👇

So you can use the 5th/6th/7th best LLMs, getting 80-85% of the top guys' performance, but at an 85-95% discount in price?

You know what we call that? A commodity...

exactly what happened with LCD TVs, OLEDs, solar panels, electric cars, phones, etc

good luck with your AI IPOs!

Imagine you spent 40 years doing the boring, responsible thing.

You opened a 401k at 23. You contributed every paycheck. You ignored the noise. You bought the index because Bogle told you to, because Buffett told you to, because every honest piece of financial advice for 30 years told you the index was the safest, most diversified, most rules-based way to own America.

The whole point was the rules.

The rules said: a company must trade for 12 months before joining the S&P 500. The rules said: it must show four consecutive quarters of GAAP profitability. The rules existed because in 1999 the index quietly bought a lot of stocks at the top, and pensioners paid the bill.

After the dot-com crash, S&P tightened the rules. Nasdaq tightened the rules. FTSE Russell tightened the rules.

For 23 years, those rules held.

Then SpaceX filed for IPO.

And the rules changed.

The S&P 500 waived the profitability requirement. Nasdaq cut its trading-history window from 90 days to 15. FTSE Russell cut its to 5.

Bloomberg Intelligence estimates the major index funds will absorb between 19% and 24% of SpaceX's float within six months. That's over $30 trillion of passive 401k and retirement money, mechanically buying a single newly public company at IPO valuations, because the rules said they had to.

Except the rules used to say they didn't.

Here's the thought exercise:

If you spend 40 years building a system designed to protect ordinary savers from buying overpriced stocks, and then you waive the protections the moment a sufficiently large stock asks you to, what was the system actually protecting?

Most of investing is about understanding what's a rule and what's a guideline.

A rule binds the rule-maker.

A guideline binds the saver.

You're allowed to find out which is which only after the fact.

The AI numbers are starting to look very ugly.

Even under "best case" assumptions, FT's own data shows Microsoft AI ROI at -9%, Google at -15%, Meta at -28%, Oracle at -35%. Only Amazon barely comes out positive.

This is exactly why I keep comparing this to the dot-com era. Incredible technology does not automatically mean sustainable economics. The internet survived. Most internet companies didn't.

Right now hyperscalers are spending trillions hoping future demand catches up to present capex. That's not certainty. That's a leveraged bet.

The quiet bomb in today’s ONS release:

Over the past 5 years

Mortgage-interest payments: up 153%.

Stamp duty up 226%.

Interest on debt up 86%.

The cost of simply having obligations has exploded.

📌 ONS Household Costs Indices for UK household groups

NEW PODCAST: Why is UK electricity so expensive?

@HelenMiller_IFS, @levell_peter & @Dieter_Helm discuss Britain’s energy mix, the costs of renewables, net zero targets, and how policy should respond to energy price shocks.

🎧 Listen here: https://t.co/vHpPpIhCW7

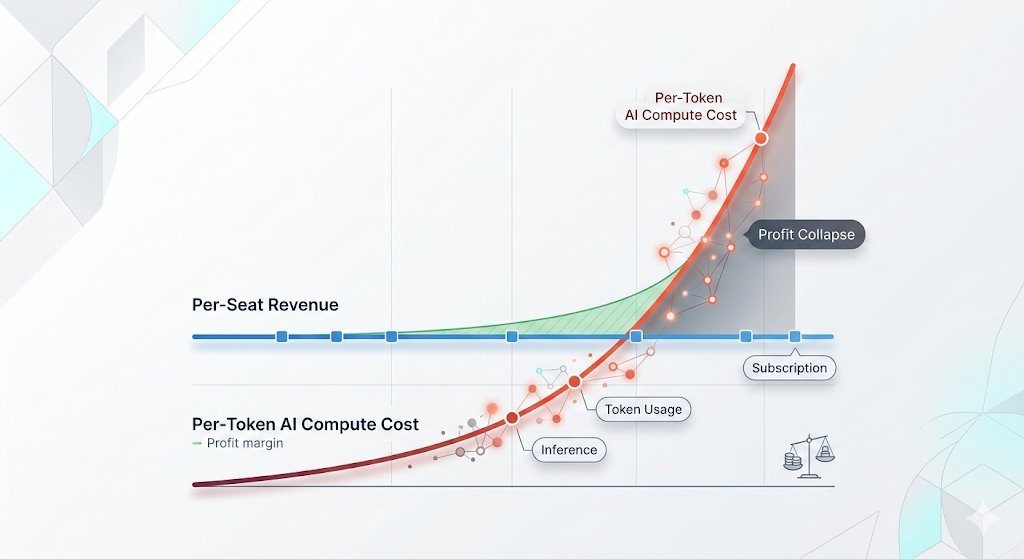

The AI bubble math doesn't add up.

Anthropic spends $3 to make $1 and that’s before you include any and all other costs like staff or electricity.

Microsoft dumped $300B in capex, made ~$18B in AI revenue. OpenAI and Anthropic alone make up 43-54% of Microsoft, Google, Amazon and Oracle's entire revenue backlogs.

Enterprises are burning through annual AI budgets in 4 months with zero measurable ROI.

This is the most expensive science experiment in history, funded by your SaaS subscriptions.

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

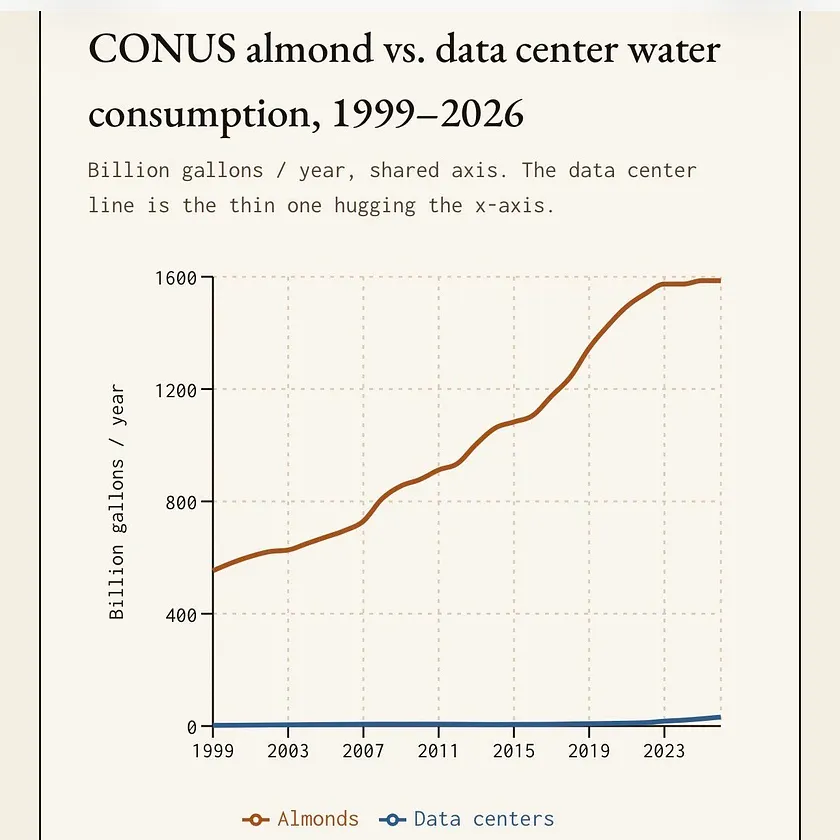

Water Use Estimated by Billions of Gallons💧

Lawns ~3,285

Almonds ~1,650

Golf Courses ~1,000

Data Center (Power) ~150

Data Center (Cooling) ~17

Bitcoin Mining ~0.000038

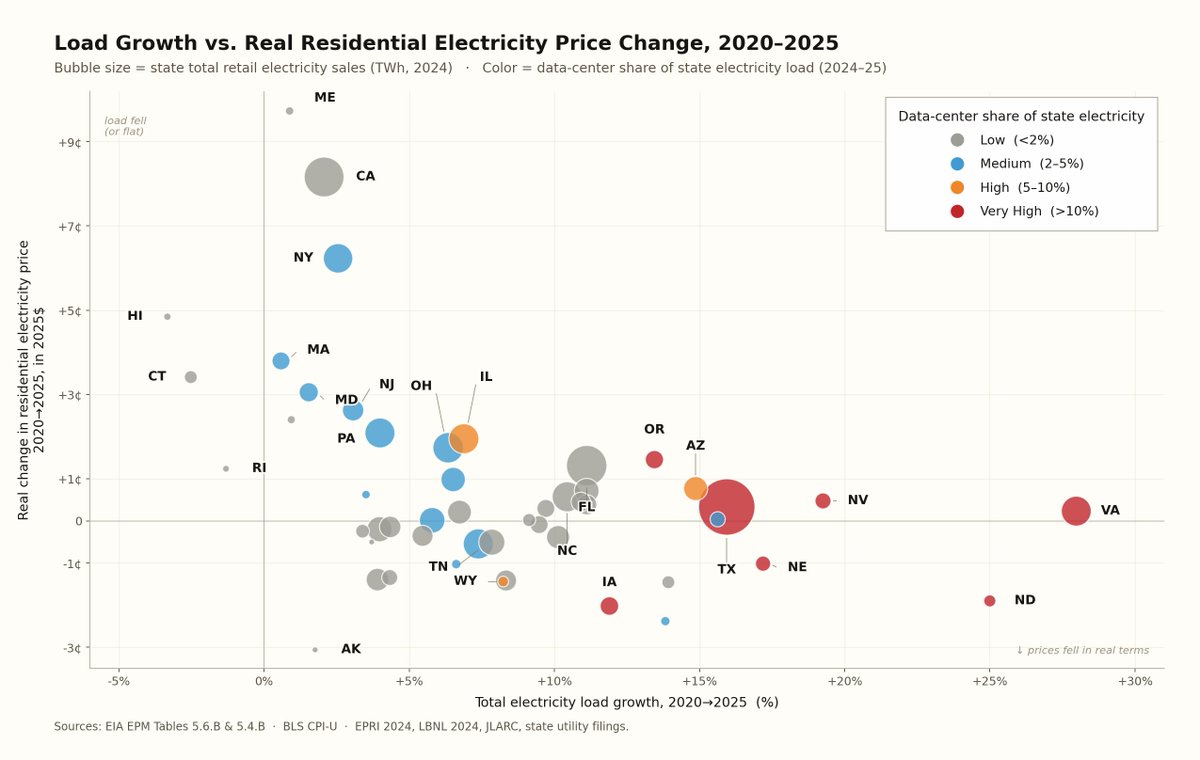

This is the single most important chart.

If AI were driving prices, you'd see a cluster top-right. You don't.

States with huge load growth (VA, TX, NV, ND, IA) sit at ~0c change in 5y. States with massive price hikes (CA, NY, MA, CT) have basically NO load growth.

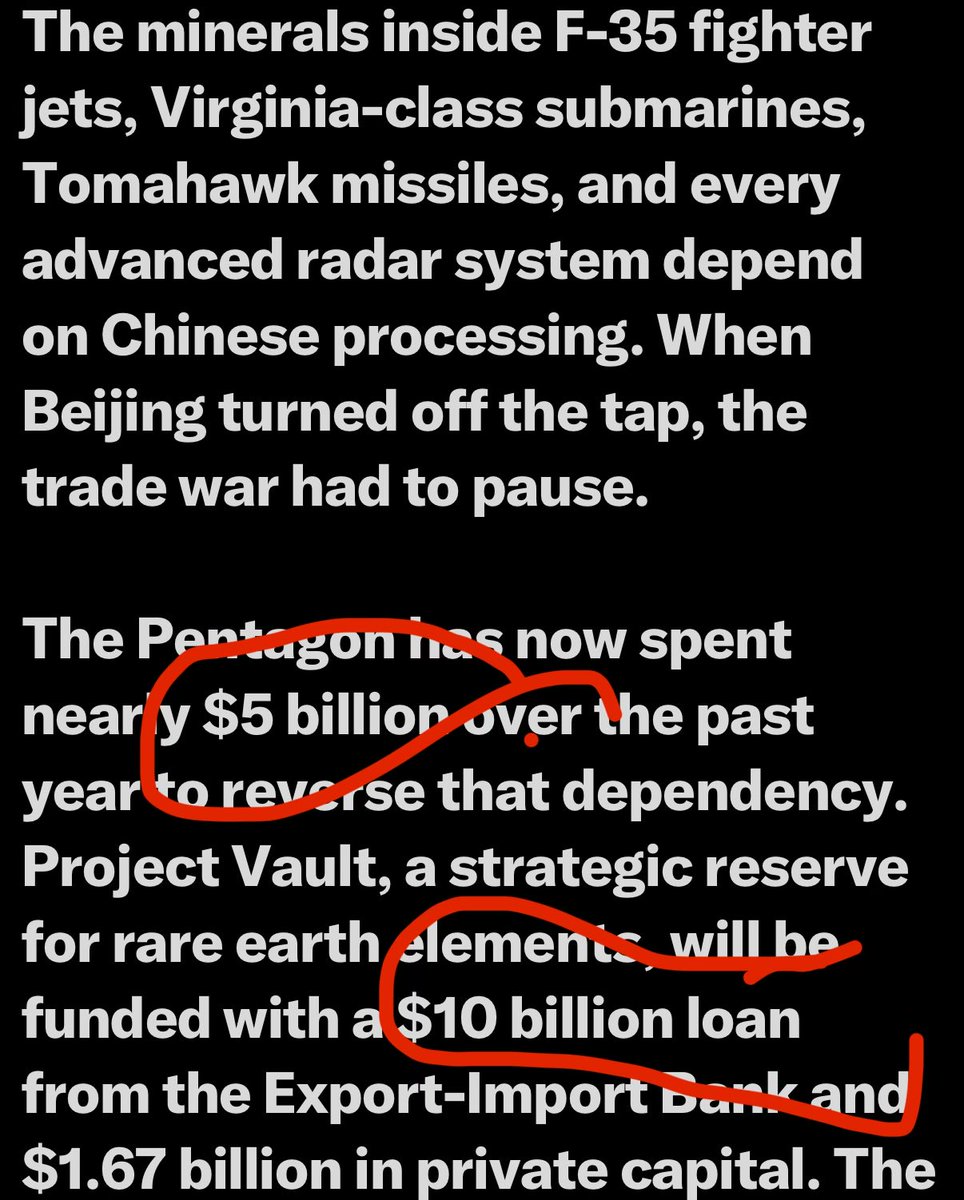

Please understand this, don’t just parrot it. The much lauded “Chinese control of rare earths” required a “whopping” $10B in US military purchase guarantees over 10yrs to begin unwinding. (A rounding error in Pentagon budget).

Markets are not the solution to everything. Sometimes we have to make choices.

Three bond markets on three continents are breaking at the same time.

US: The 30-year yield is at 5.085%. The 20-year at 5.092%. The 10-year at 4.538%. Every maturity rising together. The government is running a $2 trillion annual deficit and borrowing more every day to fund a war.

UK: Gilt yields just hit 5.13%, the highest since 2008. A leadership challenge to the Prime Minister, combined with global inflation fears and the same energy shock, is crushing British sovereign debt.

Japan: Wholesale inflation came in at 4.9%, nearly double the 3.0% forecast. Naphtha up 79.4%. The 30-year JGB yield hit 4.00%, a record for a country that spent three decades in deflation. The Bank of Japan is under pressure to hike rates in June.

The common thread: the Strait of Hormuz closure is injecting an energy shock into every major economy simultaneously. Oil spikes, wholesale inflation follows, bond markets reprice, and governments that borrowed trillions at near-zero rates discover what 5% actually costs.

Stocks are at all-time highs because AI earnings are real. Bond yields are at multi-decade highs because sovereign debt loads are also real. Both cannot be right. And historically, it is not the bond market that is wrong.